How to handle increased enforcement of unclaimed property notices

Companies can respond to states’ changing enforcement of unclaimed property notices by applying these best practices.

Unclaimed property has long been an important source of nontax revenue for states. One estimate suggests states hold tens of billions in their unclaimed property coffers, and states continue to increase enforcement of unclaimed property compliance, using ever-changing enforcement mechanisms. Accounting, legal, tax, and compliance professionals — whether as a company employee or on a client’s behalf — should be aware of unclaimed property notices, as they can expose a company to risk if not handled properly.

States have typically adopted a version of the Uniform Unclaimed Property Act from 1981, 1995, or 2016. Each version provides states the statutory authority to examine a company’s books and records to verify abandoned property compliance. To this end, each state may employ its own methodology to verify compliance.

Among the state methodologies, the industry is seeing new and increased unclaimed property notice trends:

- California Voluntary Compliance Program (VCP) reminder.

- Delaware verified reports.

- State self–audits or self–reviews.

- Penalty and interest assessments.

There are clear risks for noncompliance and notable benefits of compliance. Evaluating each trend using sample notices along with additional background information and best practices on appropriately responding will increase awareness for properly handling notices within these trends. (See “How to Handle State Unclaimed Property Notices,” JofA, March 2, 2023, for additional state notice information and see the sidebar “Unclaimed Property as Revenue?” for a quick explanation of how states account for unclaimed property.)

RISKS AND BENEFITS FOR COMPANIES

For companies, the risks of noncompliance can include unclaimed property audits, penalty and interest assessments on identified past-due unclaimed property, reputational risk, and estimations for periods where records cannot be fully researched.

Two well-known court cases in the industry illustrate the risks involved. In Temple-Inland, Inc. v. Cook, No. 14-654-GMS (D.C. Del. 2016), estimations substantially affected the company’s unclaimed property risk. For periods lacking records, the state relied upon estimation methodologies that extrapolated from a single $147.30 payroll check, resulting in an initial audit assessment of over $2 million.

In Dine Brands Glob., Inc. v. Eubanks, No. 165391, 2025 WL 898837 (Mich. 3/24/25), the plaintiffs disagreed with the period under review due to the passage of time since the multistate audit began. Unclaimed property review periods commonly extend beyond 10 transaction years, which leaves companies vulnerable to risk compared to shorter record-retention requirements set by other governing bodies, like the SEC and the IRS.

Filing unclaimed property reports regularly, however, can have several benefits, including:

- Minimizing audit risk.

- Avoiding penalties and interest.

- Helping maintain clean, accurate financials.

- Decreasing personnel time reconciling and accounting for stale balances.

- Improving customer, vendor, employee, etc. experience and trust.

- Protecting brand reputation.

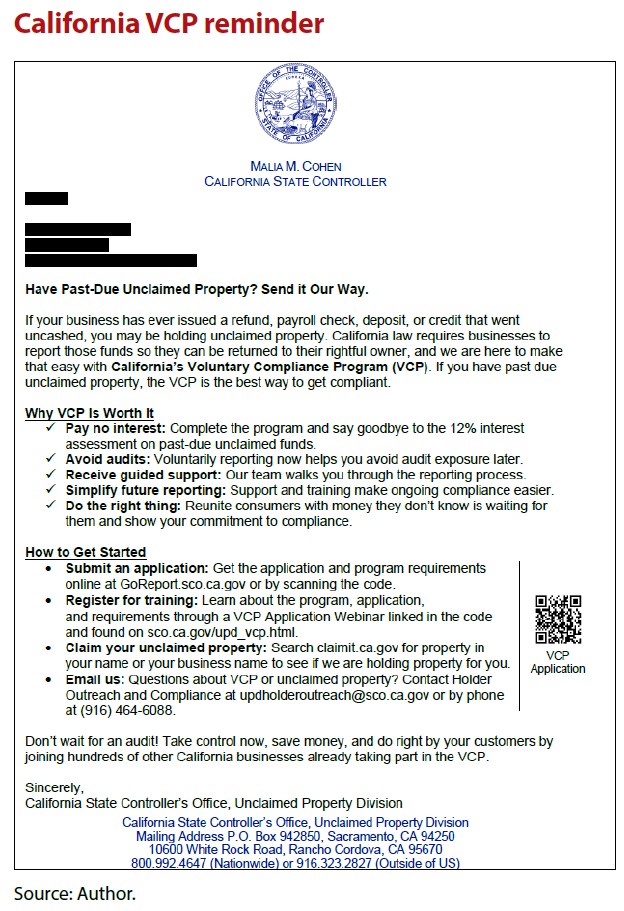

CALIFORNIA VOLUNTARY COMPLIANCE REMINDER

California launched the VCP in 2023 as a more company-friendly enforcement approach. The program has several benefits for companies that seek to handle unclaimed property compliance proactively, including a waiver of the 12% annual interest assessment and avoidance of penalties. The program also offers training for holders to learn about California’s unique dual-reporting process.

To support the launch of the relatively new program, the California State Controller’s Office (CA SCO) mailed out VCP reminders in late 2025. (See “California VCP Reminder.”) As part of an outreach and education campaign, initial mailings were sent to about 4,000 companies, with follow-up letters sent in February 2026. Future mailings will also be sent to new groups of holders throughout 2026.

“Unclaimed property compliance is important and can be challenging and costly sometimes. We understand that,” said Gary Qualset, CPA, CA SCO’s project director, Unclaimed Property Division. “To ease the burden for holders, we have created the VCP in California to help holders get into compliance, avoid a potentially large interest assessment, and facilitate the return of more money to the rightful owners.”

DELAWARE VERIFIED REPORTS

Delaware’s third-largest source of revenue is unclaimed property receipts. As such, the state is regularly enforcing unclaimed property compliance via several statutory mechanisms. These mechanisms vary, as two departments handle unclaimed property: the Secretary of State and the Department of Finance. Delaware sends three common notices to companies:

- Voluntary disclosure invitations — sent by the Secretary of State.

- Verified report notices — sent by the Department of Finance.

- Audit letters — sent by the Department of Finance.

The verified report process serves several purposes: to have companies attest to the completeness of a previously filed report; to confirm a company’s negative report (which is not required in Delaware) — that there was, in fact, no property to report; and to determine whether the company has existing unclaimed property compliance policies and procedures. (See “Delaware Verified Report Notice.”)

The Delaware Department of Finance requires companies to provide the following information within 30 days of receipt of the notice:

- A complete and notarized verified report form for the specified report year.

- A list of legal entities that were included in the verified report.

- A response as to whether the company has established unclaimed property policies and procedures along with a copy if they exist.

The state sends out these requests several times per year. Note that third-party unclaimed property audit firms assist Delaware in managing the verified report process, and companies should expect to receive a request once every three to four years.

It is crucial that a company respond within 30 days. Although companies have a full year to complete the verified report process, the state’s Enforcement page notes the state “may approve incremental extensions up to 180 days from the date of the Notice” and that information should be submitted “as soon as possible to allow for review and completion.” A response within the 30-day time frame will typically result in an extension from the reviewer if more time is necessary.

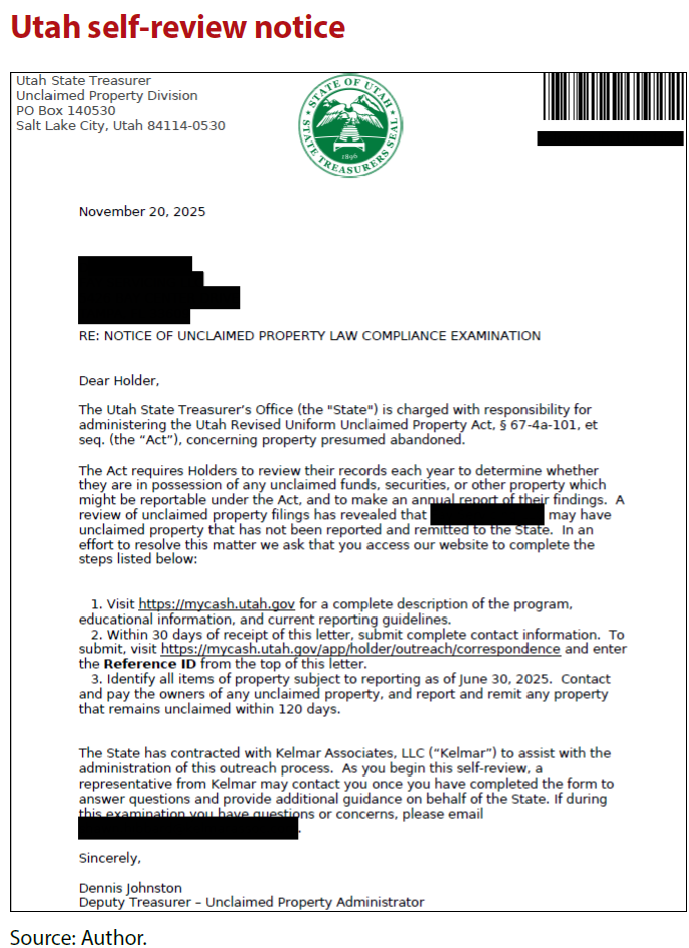

STATE SELF-AUDITS AND SELF-REVIEWS

Most states have amnesty programs that give companies an option to mitigate unclaimed property noncompliance. This compliance-friendly approach appears to be influencing the way states are electing to verify a company’s compliance with unclaimed property laws. Rather than conducting a full examination, many states are sending notices that instruct the company to perform a “self-audit,” “compliance review,” or “self-review.” While some states directly conduct these reviews (e.g., New York and North Carolina), many reviews are guided by one of a state’s third-party unclaimed property auditors, primarily Kelmar Associates LLC and Kroll Government Solutions LLC. More than 20 states now use these types of reviews. (See the example, “Utah Self-Review Notice.”)

Kelmar and Kroll perform a plethora of government solution services for states and jurisdictions. Kroll claims to assist 47 jurisdictions with their unclaimed property examination solutions. Kelmar, which services 50 jurisdictions with unclaimed property solutions, advertises two key unclaimed property solutions.

Kroll’s services for states as they pertain to unclaimed property include advanced technology, legal expertise, and forensic skills. These services assist in providing compliance and recovery solutions. Additionally, Kroll promotes that it leverages its data processing and analysis capabilities “to assist state agencies to bring thousands of small to medium-sized businesses into compliance with unclaimed property laws.”

The Kelmar Abandoned Property System (KAPS), among other things, assists states in managing unclaimed property reports and receipts received from companies. To date, 42 states are enrolled in KAPS, including Utah. Kelmar also developed the State Targeted Assisted Compliance System (STACS) “for unclaimed property programs to identify noncompliant holders, perform holder outreach, deliver education, and manage other voluntary compliance initiatives.”

Any responses provided by a company in such a review should not be taken lightly, as the response can potentially lead to a full examination (audit).

In reviewing the example notice, companies should note the 30-day response deadline for completing the first step of the process. Once this step is complete, Kelmar then provides a questionnaire and scoping matrix to be completed within 120 days of receipt of the original notice.

The Kelmar scoping exercise requests that entity information be supplied to exhibit the company’s intention for review. This, in turn, is likely to provide the state and Kelmar with detailed information that may not have been apparent through the annual reporting process (e.g., subsidiary information for holders that consolidate filings). Additionally, the questionnaire includes guidance that the holder should review disbursement accounts (e.g., accounts payable or payroll) and receivable functions (e.g., overpayments or unidentified remittances), along with all other property categories that may generate unclaimed property (e.g., checking/savings accounts for financial institutions or gift card programs for retailers) for the last 10 report years, though the number of years for review may differ by state. In unclaimed property, the last 10 report years typically equate to the last 13 to 15 transaction years. Most companies find it challenging to perform such a comprehensive review within the 120 days provided.

Accountants should be especially considerate of how they respond. Providing the aforementioned entity and property type information without thoroughly understanding the potential downstream effects may subject the company to additional risk such as future audits or inquiries on entities or property types not explicitly included in the responses. Also, companies should seek extensions, where needed, to ensure any assertions made can be properly vetted and reviewed.

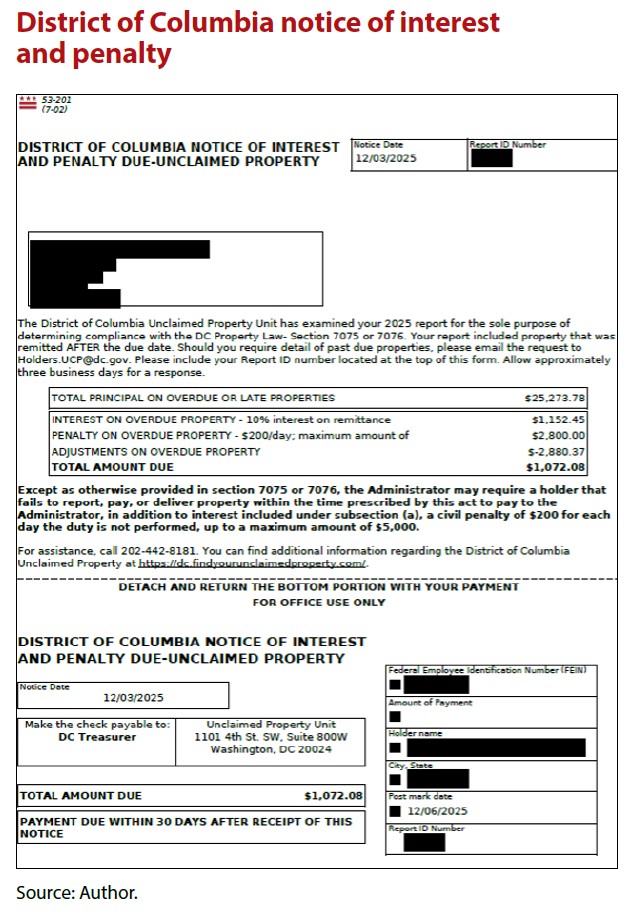

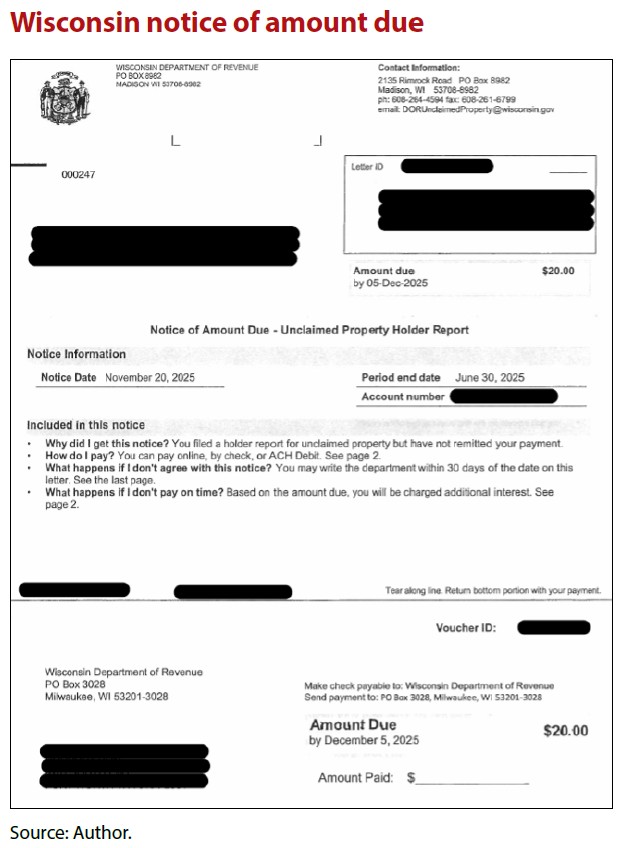

PENALTY AND INTEREST ASSESSMENTS

All states have the statutory authority to assess penalties and interest. Typically, these assessments occur when property is reported or remitted late by a holder. Historically, only a handful of states have regularly assessed penalties and interest (e.g., California and Texas), but in recent years, the number of states sending assessments has grown (e.g., the District of Columbia and Maryland). This, too, provides an example of how states can more easily enforce their statutes, especially when they are readily able to do so through the use of third-party software, such as Kelmar’s KAPS/STACS systems.

When reviewing an assessment, consider:

- The amount of the assessment.

- The corresponding state statute.

- The due date to pay the assessment.

- Any noted capabilities to seek mitigation of the assessment or receive further information from the state on the assessment.

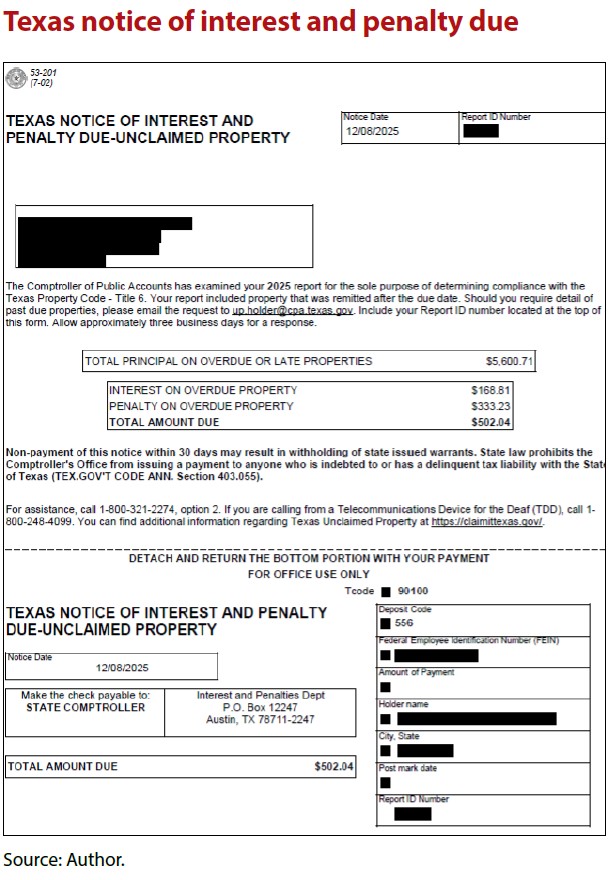

The following notices provide examples of penalty and interest assessments received from the District of Columbia, Wisconsin, and Texas, respectively. (See, “District of Columbia Notice of Interest and Penalty,” “Wisconsin Notice of Amount Due,” and “Texas Notice of Interest and Penalty Due.”)

Note the similarities between the District of Columbia and Texas assessments. Both jurisdictions use Kelmar’s KAPS software, which quickly generates assessments for any late-reported unclaimed property.

MAINTAIN COMPLIANCE

Companies with comprehensive unclaimed property compliance programs minimize their liabilities and lower their audit risk. Regularly performing risk assessments to locate missed or underreported property assists in early detection and remediation efforts. Companies may also perform off-cycle reports for missed property types or inherited unclaimed property risk from a merger or acquisition. Lastly, companies should have robust policies and procedures to help identify, track, and document their unclaimed property efforts.

To obtain more information on state reporting requirements or to search for unclaimed property, visit the National Association of Unclaimed Property Administrators’ website.

Note: MarketSphere Consulting LLC specializes in unclaimed property compliance and management. MarketSphere is not an accounting firm or a law firm, and the information herein is not intended to be, and shall not be, construed as accounting or legal advice.

Unclaimed property as revenue?

You may wonder what makes it possible for states to recognize unclaimed property as revenue when they retain the obligation to return funds to the rightful owners. Under GASB’s framework for nonexchange transactions, governments may recognize inflows of resources when they receive value without providing equal value in return, provided the government has a legally enforceable claim to the resources. Escheat statutes generally establish such a claim once dormancy and due-diligence requirements are met.

For governmental fund reporting, once unclaimed property meets the criteria of being measurable and available, it qualifies for revenue recognition within the appropriate reporting period. For proprietary fund reporting and at the governmentwide level, revenue recognition is based on accrual principles rather than the availability criterion. Although governments may be required to return funds if owners later come forward, GASB does not view this continuing obligation as precluding initial recognition. Accordingly, escheated property may be recognized as an asset when the government’s statutory claim is established. The related inflow of resources is recognized as revenue in the appropriate reporting period in accordance with the applicable basis of accounting. While the property remains subject to possible reclamation, the government reports a liability for estimated future claims based on historical experience and current trends rather than deferring recognition.

LEARNING RESOURCES

State and Local Governments — Audit and Accounting Guide

This authoritative guide offers complete coverage of state and local government audit and accounting considerations critical for both preparers and auditors.

PUBLICATION

Fundamentals of Governmental Accounting and Reporting: Fund Accounting and Financial Statements

Fund accounting and reporting intricacies are decoded for accounting professionals and auditors who work with state and local governments.

CPE SELF-STUDY

CPE SELF-STUDY

2026 State and Local Government Audit Planning Considerations

Learn key information and considerations to inform the planning of your 2026 state and local government financial statement audits.

July 16, 11 a.m. ET

WEBCAST

Corporate Finance & Accounting community

Make new contacts and join interesting discussions at the Engage365 Corporate Finance & Accounting community, a dedicated space to connect with experts, peers, and thought leaders as you navigate the complexities of the modern business world.

COMMUNITY

For more information or to make a purchase, go to aicpa-cima.com/cpe-learning or call 888-777-7077.

MEMBER RESOURCES

Article

“How to Handle State Unclaimed Property Notices,” JofA, March 2, 2023

Websites

State & Local Tax (SALT) (topic hub)