- feature

- FORENSIC ACCOUNTING

Applying Forensic Skepticism to Lost Profits Valuations

Use the correct tools to avoid overcompensating claimants.

Please note: This item is from our archives and was published in 2010. It is provided for historical reference. The content may be out of date and links may no longer function.

Related

CP53E notice tied to paper-check transition causes confusion

Fair value considerations for private credit providers and their investors

How to protect nonprofits from hidden fraud risks

Forensic accountants are frequently engaged to review insurance claims for business interruption or lost profits. Owners of privately held companies may inflate loss claims since they have control over the books and records. Business interruption (lost profits) insurance is intended to restore the claimants, not reward them with excess reimbursement. Generally, insurance policies consider the following methodology to quantify a loss: an insured is entitled to net income (loss) plus continuing expenses for the loss period. The objective of the forensic accountant is to prepare the calculation while concurrently searching for potential fraud. This article uses a hypothetical case study to highlight areas that require further examination in determining lost profits.

LOSS CALCULATION

Forensic accountants typically use one or more of the following methodologies to calculate business interruption losses: (1) the before-and-after method, (2) the comparable method (or yardstick method), (3) the “but for” method, or (4) the breach-of-contract method. The mechanics of each method require a special set of skills to carry out the computation. However, beyond the technical expertise, additional reflection in the form of forensic skepticism and consideration for the elements of the fraud triangle (pressure, opportunity and rationalization) are necessary to avoid overcompensating a lost profits claimant. An inquisitive mind may begin by addressing qualitative issues surrounding the particular case such as the current operating status of the business; the age of the owner; and whether the claimant is represented by a third party whose compensation is based upon the value of the recovery on the claim. An analysis that examines these issues may lead to a distinctly different conclusion than an analysis based merely on numbers.

For example, the age of the owner(s) may be a relevant motivating factor. If a business cannot be sold to a third party and the owners are approaching retirement age, a window of opportunity may present itself in the form of a lost profits claim. A claimant may also choose to be represented by a third party to present the loss to the insurance company. In such a case, these types of representatives are usually paid a percentage of the value of the recovery on the claim. The obvious incentive is to obtain the largest possible recovery. This does not mean that these representatives always submit inflated claims, but the forensic accountant must be mindful of the actor’s motives and consider their potential in the overall valuation of the loss.

CASE STUDY: BEST BROTHERS BANQUETS

Facts. Best Brothers Banquets Inc. (BBB) was established 25 years ago. The banquet hall, located on the banks of a river, has been in business at this location for almost three decades. Neither the corporation nor the individual shareholders owned the property that housed the banquet hall. BBB had a long-term lease with the property owner.

The family-owned corporation was owned equally by brothers Bob Best and Bert Best. Recently, the brothers decided to reduce their work hours since they were both in their late 50s and wanted more personal time. As a result, they hired a manager to run the daily operations.

The banquet hall needed some refurbishing. Its aesthetic shortcomings may have contributed to declining revenues in recent years. However, because of the community goodwill that BBB had built from its long history in the area and its strategic location, the business remained fairly profitable. In August, generally a slow month, a fire destroyed the banquet hall. The building was left untenable, causing the business to shut down. Due to the significant damage and loss of business, the Best brothers retained an attorney to represent BBB in its insurance claim. The attorney agreed to receive as compensation a percentage of the recovery from the insurance company.

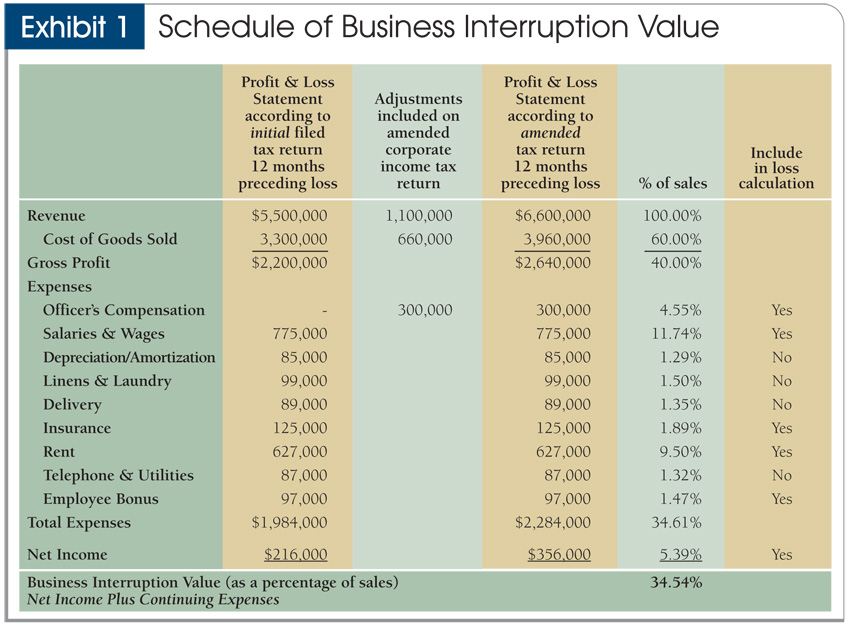

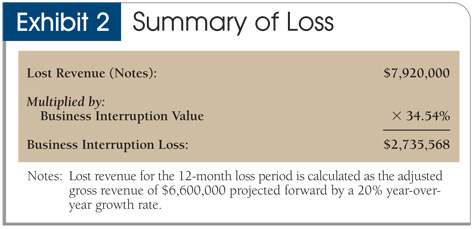

Using the before-and-after method of calculation, BBB submitted the 12-month loss claim shown in Exhibits 1 and 2.

Click here to view Exhibit 1: Schedule of Business Interruption Value

{kind=link}

Click here to view Exhibit 2:Summary of Loss

{kind=link}

ANALYSIS

Gross income adjustment. The claimant provided records showing the two preceding years of corporate income tax returns. The corporation has a year-end of Dec. 31. Since all records on the premises were destroyed in the fire and BBB recently retained a new accounting firm to prepare its corporate income tax returns, the limited records provided by the claimant were the only ones available. The previous accountant retired and provided the clients all of their records. Additionally, an amended corporate income tax return was submitted to the insurance company for the year immediately prior to the loss. The explanation on the amended tax return stated that in the initial filing an amount representing 20% of the gross income was inadvertently omitted due to the lack of communication during the transition of accounting firms. In addition, officers’ compensation was initially omitted. The amended return was dated in August of the loss year, subsequent to the business interruption date.

Application of forensic skepticism. An analysis of the amended corporate income tax return has revealed the following concerns:

- When removing the 20% omission of income, BBB had flat year-over-year growth in gross revenue.

- The net income increased as a percentage of sales, creating the potential for a larger recovery.

- The filing date was subsequent to the business interruption date.

Questions that may be asked to verify the authenticity of the amended corporate income returns include:

- Has this amended return been filed with the proper federal and state taxing authorities?

- Have the proper taxes been paid?

Determination. The only information subsequently provided were copies of checks that were not cashed by the taxing authorities for the increase in shareholder taxes as a result of the amended tax return. To determine if the amended corporate income tax return was actually filed with the IRS, the claimant was asked to provide a transcript of the tax return from the IRS; this request was ignored. Since it could not be corroborated, the additional income reflected on the amended corporate income tax return should not be considered in the final calculation of the loss claim.

OFFICERS’ COMPENSATION

Typically, officers’ compensation is an undisputed element of a lost profits claim; the officers are generally entitled to the profits associated with the business. Generally, the officers’ compensation is either paid to the owners in profits or compensation, therefore, an increase in one results in a decrease in the other. In the case of BBB, the officers were not on payroll prior to the loss date. This is most likely the result of a recent sales decline resulting in shrinking profitability and the inability to support the compensation historically paid to the officers. The owners also recently hired a manager to run the restaurant’s everyday operations, effectively reducing their operational responsibilities.

Application of forensic skepticism. Officers’ compensation was included in the business interruption value in an attempt to provide continuity in BBB’s historical income and expense behavior. Although the officers/owners are always entitled to net income in the business interruption value, without including the compensation for the officers, the net profit percentage would seem inordinately high in the year immediately preceding the loss. The additional effect of the amended corporate income tax return creates the potential for a recovery greater than the actual losses. This places BBB in a better position after the loss than prior to the loss. To validate the genuineness of this expense, BBB’s payroll tax returns and the accompanying tax payments should be requested.

Determination. Copies of the amended payroll tax returns were provided with a copy of the corresponding check to pay the additional payroll taxes. The IRS had not cashed the check. The fact the check did not clear the bank is suspicious. Again, a request should be made to verify that the payroll tax returns presented to support the claim are the same as ones filed with the IRS. It is important to always confirm that the tax returns presented for the claim are the tax returns on file with the taxing authorities.

Once more, the claimant did not comply with the request, therefore, the amended payroll returns were not considered in valuing the loss.

CONTINUING SALARIES AND WAGES (PAYROLL)

Continuing payroll for BBB included wages for the chef, waitresses, busboys and dishwashers. BBB employed these individuals for many years, and they were considered key. The payroll tax returns provided by the claimant corroborate salaries and wages that allegedly continued during the loss period.

Application of forensic skepticism. A request was made to interview all of the employees included as continuing on the BBB payroll. This request was denied, and the Best brothers offered to be interviewed as an alternative. During the interview, it was discovered that the payroll tax returns were not filed with the proper taxing authorities. The corresponding tax payments were also not made.

The pressing issue at this point is the legitimacy of the payroll. Since the employees were working at BBB for a long time, it would be plausible for them to be collecting unemployment benefits, effectively refuting the continuing expense claim. A statement of account was requested from the Department of Labor for the most recent period detailing unemployment benefits charged to BBB’s account. The report from the Department of Labor provides the specific names, dates and weekly unemployment benefits paid to BBB’s employees.

Determination. The Department of Labor report showed that every employee listed as continuing on the BBB payroll, except the chef, was also collecting unemployment benefits. Since a payroll service was preparing the company payroll reports before the loss, it was easy and relatively inexpensive to have a complete set of payroll records prepared during the loss period. As a result of the extra steps taken to scrutinize the employee expenses, the chef was the only employee included in the loss claim.

RENT

Rent was presented as a continuing expense included in the business interruption value. The fire utterly destroyed the building, leaving it uninhabitable. Even partial operation was not possible.

Application of forensic skepticism. BBB’s lease provided that regular rent would not have to be paid if the building became untenable. However, another clause required BBB to continue paying a stated portion of operating expenses even if the building was untenable.

Determination. It would seem plausible to conclude that if a fire renders a lessee’s building untenable, the obligation to pay rent would cease. A thorough reading of the lease determined that a portion of the rent does in fact continue. The continuing portion was included in the loss claim.

EMPLOYEE BONUSES

This expense was explained as an incentive program for employee customer service based upon surveys submitted by patrons. Again, this explanation appeared conceivable since service-oriented businesses strive for optimum customer satisfaction.

Application of forensic skepticism. An analysis of the general ledger account for employee bonuses commenced. The account in the general ledger appeared to have several entries payable to cash and dated during the loss period. This coincidence raised the question of why these payments were disbursed around the same time. BBB did not provide an explanation for this. The next step was to ask for a copy of the front and back of canceled checks.

Determination. Examination of the canceled checks revealed that they were deposited in the bank account of a vendor who supplied food, linens and other products to BBB. To further inspect the validity of the expense, invoices from the vendor were requested. It was discovered that these payments were for expenses prior to the loss, which are cost of goods sold—theoretically, a noncontinuing expense.

CONCLUSION

This article emphasizes the integration of forensic skepticism into the generally accepted methods of calculating lost profits in insurance-related matters. The case of BBB provides examples of the red flags that call for further examination. The resulting illustration brings to light how compelling these factors are in the calculation of the loss.

Methods of Loss Calculation

Forensic accountants typically use one or more of the following methodologies to calculate business interruption losses:

The before-and-after method. This considers profits across a spectrum of time. The period of profits before the loss is compared to the period of profits after the loss. The sales growth before the act is compared to the sales growth after the act. Profits are measured by comparing continuing expenses plus net income (or net loss) from the period affected by the alleged damaging acts with either the pre-damage profits and/or the post-damage effect on profits to calculate the lost profits. Since this method usually does not require a lot of data and may be applied with one or two years of sales growth data, it is an attractive choice for short-term losses.

The comparable company method. This method identifies similar companies or industries that are comparable to the company claiming the loss. The forensic accountant uses this information to project the claimants’ profits by referring to the performance of comparable companies or industries. This method may be used when there is no historical information available for a company.

The “but for” method. This method is based upon a financial model that uses assumptions about income and expenses. The estimated loss of income is the difference between estimated profits and actual profits “but for” the actions of a defendant to a civil claim. Typical techniques used in the “but for” method are time series forecasting methods such as exponential smoothing and autoregressive integrated moving average models. A classic linear regression analysis model may also be used.

The breach-of-contract method. This method is used when a contract is infringed that contains explicit requirements for the calculation of liquidated and other damages in the event of a breach of contract. The analysis provided by the forensic accountant will follow the contract terms.

EXECUTIVE SUMMARY

Forensic accountants are frequently engaged to review business interruption (lost profits) damages for insurance claims. Although it isn’t always the case, owners of privately held companies may have the opportunity to inflate loss claims.

To help avoid overcompensating a lost profits claimant, forensic accountants should prepare the lost profits calculation while using forensic skepticism to search for potential fraud.

One or more of the following methodologies are typically used for calculating business interruption losses: (1) the before-and-after method, (2) the comparable method (or yardstick method), (3) the “but for” method, and (4) the breach-of-contract method.

As part of the process, certain qualitative issues surrounding the case should also be considered, such as the current operating status of the business and whether the claimant is represented by a third party whose compensation is contingent upon the value of the recovery on the claim. An analysis that examines these issues may lead to a distinctly different conclusion than one based on numbers alone.

James A. DiGabriele (jim@dmcpa.com) is an accounting professor at Montclair State University.

To comment on this article or to suggest an idea for another article, contact Loanna Overcash, senior editor, at lovercash@aicpa.org or 919-402-4462.

AICPA RESOURCES

JofA articles

- “Detecting Circular Cash Flow,” Dec. 09, page 26

- “Selecting the Right Investigative Resource,” Dec. 09, page 40

Use journalofaccountancy.com to find past articles. In the search box, click “Open Advanced Search” and then search by title.

Publications

- Forensic Accounting—Fraud Investigations: FVS (Formerly BVFLS) Practice Aid 07-1 (#055305)

- Practice Aid 06-4: Calculating Lost Profits (#055303PDF, available for download only)

CPE self-study

Auditing for Internal Fraud (#730282)

For more information or to place an order, go to cpa2biz.com or call the Institute at 888-777-7077.

On-Site Training

Forensics and Financial Fraud: Real-World Issues & Answers (#FFF)

To access courses, go to aicpalearning.org and click on “On-Site Training” and search by “Acronym Index.” If you need assistance, please contact a training representative at 800-634-6780 (option 1).

FVS Section and CFF credential

Membership in the Forensic and Valuation Services (FVS) Section provides access to numerous specialized resources in the forensic and valuation services discipline areas, including practice guides, and exclusive member discounts for products and events. Visit the FVS Center at aicpa.org/FVS. Members with a specialization in forensic accounting may be interested in applying for the Certified in Financial Forensics (CFF) credential. Information about the CFF credential program is available at aicpa.org/CFF. Practice Aid 06-4: Calculating Lost Profits is available free to FVS Section members on the FVS Center’s Practice Aids and Special Reports page.