Proposed new sustainability information AT-C sections

In Part 3 of a three-part series, learn about the new subject matter-specific sections of the attestation standards for examination or review engagements on sustainability information.

Editor’s note: This is the last article in a three-part series on revisions to the attestation standards proposed by the AICPA Auditing Standards Board (ASB). You can access the February 2026 exposure draft and response template (February 2026 ED) and the March 2026 exposure draft and response template (March 2026 ED). Comments on the exposure drafts are requested from respondents by June 30.

The ASB has long played a prominent role in the United States with respect to issuing high-quality guidance related to sustainability matters. The AICPA guide Attestation Engagements on Sustainability Information (Including Greenhouse Gas Emissions Information and Climate-Related Financial Disclosures) (the sustainability guide), most recently updated in December 2022, is one of the primary resources for U.S. CPAs when performing attestation engagements to report on sustainability information. However, given the increasing focus in the U.S. and worldwide on environmental, social, and governance (ESG) matters, as well as the issuance in November 2024 by the International Auditing and Assurance Standards Board (IAASB) of the International Standard on Sustainability Assurance (ISSA) 5000, General Requirements for Sustainability Assurance Engagements, there has been an increasing demand from U.S. stakeholders for additional standards and guidance with respect to reporting on sustainability information.

To address this call to action, the ASB developed two new sustainability information AT-C sections:

- Proposed AT-C section 325, Reporting on an Examination of Sustainability Information.

- Proposed AT-C section 330, Reporting on a Review of Sustainability Information.

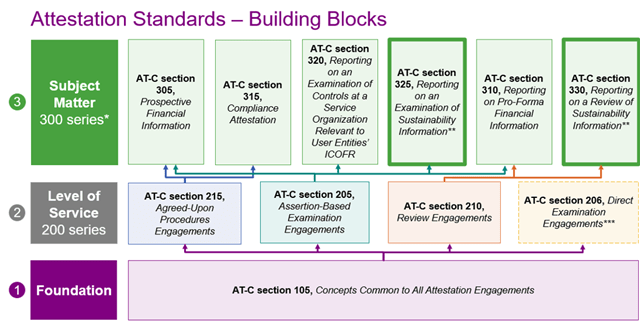

How the proposed new AT-C sections fit into the attestation standards is illustrated in the “Attestation Standards — Building Blocks” graphic below in bold green outline.

* The codification of the attestation standards includes a designated section for AT-C section 395, Management’s Discussion and Analysis. As the ASB is requesting feedback on potentially withdrawing this section, it was determined unnecessary to include this subject matter AT-C section in the graphic.

** Proposed subject matter attestation standard.

*** AT-C section 206 is not applicable to examination engagements related to subject matter for which other AT-C sections require the application of AT-C section 205. This includes all of the subject matter sections.

When developing the sustainability information AT-C sections, the ASB took into account the proposed revisions to AT-C sections 105, Concepts Common to All Attestation Engagements; 205, Assertion-Based Examination Engagements; and 210, Review Engagements, (the baseline attestation standards) and, using the building blocks approach, developed incremental requirements for inclusion in the new subject matter-specific AT-C sections. ISSA 5000 was used, where appropriate for the U.S. jurisdiction, as well as the AICPA sustainability guide, as the basis for developing the incremental requirements. This approach is consistent with the ASB’s strategic actions to develop high-quality standards in the public interest.

Linkages between the sustainability information AT-C sections and the proposed baseline attestation standards

In addition to headings being used consistently across the applicable AT-C sections, the sustainability information AT-C sections include requirements that:

- Build on related requirements in proposed AT-C section 105, 205, or 210, as applicable. In such circumstances, the phrase “in applying AT-C section [number]” is used, which indicates that, as part of performing the specified requirement in that other AT-C section, the practitioner is required to do something more.

- Are unique to proposed AT-C section 325 or 330.

Where application material is included in the sustainability information AT-C sections for which there is no related specified requirement in proposed AT-C section 325 or 330, the phrase “in accordance with AT-C section [number]” is used to reference the requirement in that other AT-C section, either in its entirety or in part, for purposes of providing a link. (A footnote referencing the relevant requirement in that other AT-C section is included.)

Significant matters addressed in the proposed sustainability information AT-C sections

The following selected matters are unique to an engagement to report on sustainability information:

Materiality

Proposed AT-C sections 205 and 210 require the practitioner to consider materiality for purposes of establishing the overall engagement strategy, determining the nature, timing, and extent of procedures, and determining whether the uncorrected misstatements are material when forming an opinion and conclusion, respectively, on the engagement.

To report on sustainability information in an examination or a review engagement, the practitioner considers materiality for qualitative disclosures and determines materiality for quantitative disclosures. This is an acknowledgement that, given the nature of qualitative disclosures, the practitioner may not, in all instances, be able to determine materiality.

Similarly, the practitioner is required to determine performance materiality for quantitative disclosures of sustainability information.

Criteria that assist the decision-making of the intended user may relate to:

- Either:

- The material impacts of ESG matters on the entity’s strategy, business model, and performance, which may be referred to as “financial materiality”; or

- The material impacts of the entity’s activities, products, and services on the environment, society, or the economy, which may be referred to as “impact materiality.”

- Double materiality, that is, both financial materiality and impact materiality.

If the criteria require the entity to apply financial materiality and impact materiality (that is “double materiality”) in preparing the sustainability information, the practitioner should take into account the double materiality concepts when establishing materiality for purposes of planning and performing the attestation engagement and when forming the conclusion.

Risk assessment procedures

The practitioner is required to design and perform risk assessment procedures sufficient to identify and assess risks of material misstatement, whether due to fraud or error:

- For an examination engagement, at the underlying assertion level for the sustainability disclosures.

- For a review engagement, at the sustainability disclosure level.

This distinction is intended to focus the practitioner’s work effort depending on the level of service being performed and to drive a more granular risk assessment in the case of an examination engagement.

Similarly, the procedures the practitioner performs to obtain an understanding of the components of the entity’s system of internal control relevant to the sustainability matters and the preparation of the sustainability information differ between an examination and a review engagement on sustainability information. The procedures performed are intended to be commensurate with the assurance being obtained, which is reasonable assurance (examination engagement) or limited assurance (review engagement), and are as follows:

- In an examination engagement, the practitioner is required to obtain an understanding through inquiry and other procedures of the components of the entity’s system of internal control which are — the control environment, the entity’s risk assessment process, the entity’s process for monitoring the system of internal control, and the information system and communication.

- In a review engagement, the practitioner’s work effort with respect to the entity’s system of internal control is less extensive and only requires the practitioner to obtain an understanding through inquiry.

The work performed to identify risks in a review engagement on sustainability information is intended to be more targeted (that is, at the sustainability disclosure level) and more extensive than a review performed in accordance with proposed AT-C section 210 only (which is applicable to all subject matters). For example, proposed AT-C section 330 requires the practitioner to obtain an understanding of the components of the entity’s system of internal control, whereas proposed AT-C section 210 requires the practitioner only to identify areas in which a material misstatement is likely to arise.

Responding to risks of material misstatement

In proposed AT-C sections 325 and 330, the practitioner is required to design and perform further procedures, which may include tests of controls or substantive procedures, when responding to the assessed risks of material misstatement. As defined in the attestation standards, substantive procedures extend to tests of details and analytical procedures.

The procedures to obtain limited assurance in accordance with proposed AT-C section 210 when responding to areas in which a material misstatement is likely to arise include inquiries and analytical procedures. But there is nothing precluding the practitioner from designing and performing additional procedures.

Therefore, when responding to risks of material misstatement in a review engagement on sustainability information, limited assurance may still be obtained by inquiries and analytical procedures only. But given the nature of the subject matter, further procedures such as tests of details are more likely to be performed.

Requirements and guidance related to further procedures that may be performed in a sustainability information engagement are included in proposed AT-C section 330.

Reporting

When engaged to report on sustainability information, the practitioner’s examination and review reports require a number of additional elements that are intended to provide transparency about the procedures performed. These incremental elements include:

- For an examination engagement, a statement that the nature, timing, and extent of the procedures selected depend on the practitioner’s judgment and include:

- The practitioner performing risk assessment procedures that are appropriate in the circumstances, including obtaining an understanding of internal control relevant to the examination to identify and assess the risks of material misstatement, whether due to fraud or error, at the underlying assertion level for the disclosures, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, no such opinion is expressed. If the examination report includes an opinion on internal control, the practitioner should omit “but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control.”

- The practitioner designing and performing procedures that are responsive to the assessed risks of material misstatement at the underlying assertion level for the disclosures.

- For a review engagement, a statement that a review involves performing procedures to obtain evidence about the sustainability information. The nature, timing, and extent of the procedures selected depend on the practitioner’s judgment and include:

- Performing risk assessment procedures that are appropriate in the circumstances, including obtaining an understanding of internal controls relevant to the review to identify and assess the risks of material misstatement, whether due to fraud or error, at the disclosure level, but not for the purpose of expressing a conclusion on the effectiveness of the internal control.

- Designing and performing procedures that are responsive to the assessed risks of material misstatement at the disclosure level.

Comparative information

Comparative information presented in sustainability information is an evolving and complex area. Criteria may be silent about whether comparative information should be presented, thereby driving voluntary presentation with the resulting inconsistency when such information is presented. Furthermore, frameworks may provide flexibility on the presentation of comparative information, including exemptions on first-time adoption of the criteria, and the extent of comparative information to present.

Unique facts and circumstances also may affect the practitioner’s responsibilities for the comparative information and how to address the comparative information in the practitioner’s report.

In responding to these challenges, the proposed sustainability information AT-C sections endeavor to establish a common understanding of what comprises comparative information by defining the term as follows:

Comparative information. Information for one or more prior periods presented for comparison to the current-period sustainability information. Comparative information may be presented as of multiple dates or cover multiple periods.

In addition, the proposed requirements addressing the practitioner’s responsibilities, the procedures performed as well as what should be included in the practitioner’s report regarding comparative information are principles-based to allow for flexibility for the wide variety of circumstances, while providing sufficient clarity to drive consistency in practice.

Other matters impacting the proposed sustainability information AT-C sections

For a more detailed explanation of other matters, such as the scope of the sustainability information AT-C sections or communications between the practitioner and a predecessor practitioner in connection with the acceptance of the attestation engagement, refer to the explanatory memorandum of the proposed Statement on Standards for Attestation Engagements (SSAE), Common Concepts, Examination Engagements, Review Engagements, and Engagements to Report on Sustainability Information, issued in February 2026 (see sections IV.F and IV.G in the explanatory memorandum).

The series at a glance

The JofA is publishing three articles about the proposed enhancements to the attestation standards. These articles will cover:

- Part 1: Structure of the attestation standards and proposed enhancements.

- Part 2: Proposed revisions to examination and review engagements in the attestation standards.

- Part 3: Proposed new sustainability information AT-C sections.

— Mike Glynn, CPA, CGMA, and Ahava Goldman, CPA, CGMA, are associate directors for the AICPA Audit & Attest Standards team. Sally Ann Bailey, CPA, Chartered Accountant (South Africa), serves as a consultant to the AICPA, working with technical staff on standard-setting activities. To comment on this article or to suggest an idea for another article, contact Jeff Drew at Jeff.Drew@aicpa-cima.com.