Fair value considerations for private credit providers and their investors

The private credit market, which has grown rapidly in recent years, has increasingly come under the spotlight. Rarely a day goes by without a news story on the topic tackling issues around the quality of underlying loans, valuation quality, and transparency.

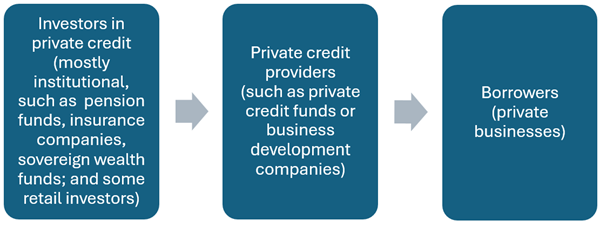

Staff at the Federal Reserve Board of Governors in an article in FEDS Notes define private credit as “debt-like, non-publicly traded instruments provided by non-bank entities, such as private credit funds or business development companies (BDCs), to fund private businesses. Private credit is typically extended to middle-market firms with annual revenues between $10 million and $1 billion but has grown rapidly in recent years to fund larger companies that were traditionally funded by leveraged loans.” The following illustration provides a simplified diagram of participants in the private credit market:

Participants in the private credit market

Private credit providers typically offer their investors the opportunity to invest in pooled investment vehicles that apply FASB ASC 946, Financial Services — Investment Companies, which requires measuring their investments at fair value in accordance with FASB ASC 820, Fair Value Measurement.

Estimating fair value requires significant judgment in normal circumstances. However, in the current environment characterized by market volatility and uncertain outlook, applying judgment in determining fair value is even more challenging.

This article discusses certain FASB ASC 820 considerations that are particularly relevant to private credit providers and their investors and is intended to assist readers with applying FASB ASC 820 guidance.

Considerations for private credit providers

Fair value is defined in FASB ASC 820 as “[t]he price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.” Estimating fair value of investments in loans involves considering contractual terms, the borrower’s financial performance, and market participants’ expectations regarding cash flows and market yield, given the instrument’s risk and current market conditions.

Because investments in loans are less liquid and have limited observable market data, preparers often use Level 3 inputs when determining fair value of their investments.

A reporting entity might first consider the other market participants to whom it could sell the asset. In accordance with FASB ASC 820-10-35-9, “[a] reporting entity shall measure the fair value of an asset or a liability using the assumptions that market participants would use in pricing the asset or liability, assuming that market participants act in their economic best interest.” Based on guidance in FASB ASC 820-10-35-53, in the absence of relevant observable inputs, a reporting entity uses “unobservable inputs [that] shall reflect the assumptions that market participants would use when pricing the asset or liability, including assumptions about risk.”

When an entity uses its own data to develop unobservable inputs, it should adjust those inputs to reflect market participant assumptions, including assumptions about credit risk. Specifically, FASB ASC 820-10-35-54A provides, that “[a] reporting entity shall develop unobservable inputs using the best information available in the circumstances, which might include the reporting entity’s own data. In developing unobservable inputs, a reporting entity may begin with its own data, but it shall adjust those data if reasonably available information indicates that other market participants would use different data or there is something particular to the reporting entity that is not available to other market participants (…). A reporting entity need not undertake exhaustive efforts to obtain information about market participant assumptions. However, a reporting entity shall take into account all information about market participant assumptions that is reasonably available…”

Therefore, when measuring the fair value of their investments in loans, private credit providers should take into account the effect of a borrower’s credit risk (credit standing) and any other factors that might influence the likelihood that the obligation will or will not be fulfilled. For instance, if the credit risk associated with a loan increases, that change should be incorporated into the fair value measurement to compensate market participants for that increased risk.

Furthermore, when using a valuation technique that requires unobservable inputs, it is important to calibrate these inputs to an observed transaction, providing an initial set of assumptions that are consistent with the transaction price when the transaction price represents fair value.

Calibration is important, as it helps ensure that the valuation technique will not produce artificial gains or losses in subsequent measurement periods. FASB ASC 820-10-35-24C states the following regarding calibration: “If the transaction price is fair value at initial recognition and a valuation technique that uses unobservable inputs will be used to measure fair value in subsequent periods, the valuation technique shall be calibrated so that at initial recognition the result of the valuation technique equals the transaction price. Calibration ensures that the valuation technique reflects current market conditions, and it helps a reporting entity to determine whether an adjustment to the valuation technique is necessary (for example, there might be a characteristic of the asset or liability that is not captured by the valuation technique). After initial recognition, when measuring fair value using a valuation technique or techniques that use unobservable inputs, a reporting entity shall ensure that those valuation techniques reflect observable market data (for example, the price for a similar asset or liability) at the measurement date.”

In addition, private credit providers that provide investment company interests under the Investment Company Act of 1940 (the Act) should comply with the requirements of SEC Rule 2a-5 of the Act on good-faith determinations of fair value. This rule addresses valuation practices and the board of directors’ role with respect to the fair value of the investments of a registered investment company or BDC (fund). It provides requirements for determining fair value in good faith for purposes of the Act. This determination involves assessing and managing material risks associated with fair value determinations; selecting, applying, and testing fair value methodologies; and overseeing and evaluating any pricing services and valuation specialists used. The rule permits a fund’s board of directors to designate certain parties (e.g., the fund’s investment adviser or officers of an internally managed fund) to perform the fair value determinations, who then carry out these functions for some or all of the fund’s investments. This designation is subject to board oversight and certain reporting and other requirements designed to facilitate the board’s ability effectively to oversee this party’s fair value determinations.

Considerations for investors in private credit funds and BDCs

As indicated earlier, private credit providers typically offer their investors the opportunity to invest in pooled investment vehicles such as private funds, public funds (such as closed-end interval or tender offer funds), and BDCs (individually referred to as a “fund” and collectively “funds”). Private credit providers typically account for these funds as investment companies under FASB ASC 946 measuring the funds’ investments at fair value in accordance with FASB ASC 820.

Investors often value their investments in the funds under FASB ASC 820 using net asset value (NAV) as a practical expedient. The practical expedient permits the use of the investor’s allocable portion of the investment vehicle’s NAV if all of the following conditions are met:

- The investment does not have a readily determinable fair value (as per FASB ASC 820-10-15-4(a)).

- The investment is in an investment company within the scope of FASB ASC 946 or is an investment in a real estate fund for which it is industry practice to measure investment assets at fair value on a recurring basis and to issue financial statements that are consistent with the measurement principles in FASB ASC 946 (as per FASB ASC 820-10-15-4(b)).

- The NAV is calculated in a manner consistent with the measurement principles of FASB ASC 946 (that is, all or substantially all underlying investments are reported at fair value) as of the measurement date (as per FASB ASC 820-10-35-59).

The NAV practical expedient is available to investors in any fund not traded on a public exchange (e.g., investors in private credit funds and nontraded (private) BDCs) that meet these criteria. If a fund interest is actively traded on a securities exchange, it has a readily determinable fair value, which would preclude its investors from using the NAV practical expedient. Fair value of such funds should be determined using the readily determinable fair value.

Therefore, the NAV practical expedient is not available to investors in publicly traded BDCs or other public traded funds; investors in those vehicles would typically use observable market prices to estimate fair value of their investments.

Also, consistent with the guidance in FASB ASC 820-10-35-62, NAV should not be used to estimate fair value, if a decision has been made to sell a fund interest and the proceeds are expected to differ from NAV.

FASB ASC 820-10-35-60 notes that if the NAV obtained from the investee is not as of the reporting entity’s measurement date or is not calculated in a manner consistent with the measurement principles of FASB ASC 946, the reporting entity should consider whether an adjustment to the most recent NAV is necessary. The objective of any adjustment is to estimate an NAV for the investment that is calculated in a manner consistent with the measurement principles of FASB ASC 946 as of the reporting entity’s measurement date.

From a practical perspective, reported NAV is rarely available contemporaneously with the preparer’s measurement date. Therefore, adjustments to last-reported NAV for market movements, underlying investment performance, cash flows, and other significant impacts on fair value may be required.

An investor may use reported NAV provided by the investee as a practical expedient to estimate their investment’s fair value, if their allocable share of NAV is calculated in a manner consistent with the measurement principles of FASB ASC 946 as of the investor’s measurement date. However, the investor’s management is responsible for the valuation assertions in its financial statements and, thus, has a responsibility to determine if the underlying investment vehicle has calculated NAV at the measurement date consistent with the measurement principles of FASB ASC 946.

AICPA Technical Q&A Sections 2220.18–.28 provide further guidance on the NAV practical expedient (all Q&A sections can be found in Technical Questions and Answers). They are intended to assist reporting entities when implementing the provisions of FASB ASC 820 to estimate the fair value of their investments in certain entities that calculate NAV. Q&A Sections 2220.18–.28 apply to investments that are required to be measured and reported at fair value and are within the scope of paragraphs 4–5 of FASB ASC 820-10-15.

If an investor chooses not to or is not able to use the NAV practical expedient, they need to estimate fair value using other approaches. Approaches commonly used include a market approach using secondary market transactions or bids from qualified buyers and an income approach using a discounted-cash-flow method or other applicable model that captures prepayment features (e.g., a Black-Derman-Toy model). Q&A Section 2220.27, “Determining Fair Value of Investments When the Practical Expedient Is Not Used or Is Not Available,” also suggests factors to consider when estimating fair value in those circumstances. This Q&A discusses various features of investments (including gates, redemptions from an investee fund, and so on) and their impact on fair value.

Other resources

When determining fair value, entities should use FASB ASC 820 as a primary resource as well as consider other relevant resources. For example, private credit providers and their investors may find it helpful to refer to Valuation of Portfolio Company Investments of Venture Capital and Private Equity Funds and Other Investment Companies — Accounting and Valuation Guide.

This guide provides guidance and illustrations regarding the accounting for and valuation of portfolio company investments of venture capital funds, private-equity funds, and other investment companies. The following sections may be of particular relevance for private credit:

- Chapter 2, “Fair Value and Related Concepts.”

- Chapter 4, “Determining the Unit of Account and the Assumed Transaction for Measuring the Fair Value of Investments” (especially paragraphs 4.17–.24, 4.38, 4.49–.52).

- Chapter 6, “Valuation of Debt Instruments.”

- Chapter 10, “Calibration.”

- Chapter 11, “Backtesting.”

- “Private Fund Interests” section in Chapter 13 (paragraphs 13.88–.100).

- Appendix A, “Valuation Process and Documentation Considerations.”

- Appendix C, Case Study 14 — “Business Development Company With Various Debt Investments.”

— Yelena Mishkevich, CPA, CGMA, is senior manager–Accounting Standards at the AICPA. To comment on this article or to suggest an idea for another article, contact Jeff Drew, JofA editor-in-chief, at Jeff.Drew@aicpa-cima.com.