Proposed attestation changes: What CPAs should know

Part 1 of a three-part series explores the structure of the attestation standards and how the ASB proposal may change them.

Editor’s note: This is the first article in a three-part series on revisions to the attestation standards proposed by the AICPA Auditing Standards Board (ASB). You can access the February 2026 exposure draft and response template (February 2026 ED) and the March 2026 exposure draft and response template (March 2026 ED). Comments on the exposure drafts are requested from respondents by June 30.

Demand for new attestation services has increased, as companies continue to report an expanding array of nonfinancial information in areas such as sustainability, digital assets, and cybersecurity. Many stakeholders are seeking assurance on these nonfinancial subject matters.

In addition, recent federal and state regulatory actions, as well as standard-setting activities in select jurisdictions, have resulted in increased demand for attestation engagements on a broader range of topics.

According to the 2025 release of the Center for Audit Quality’s (CAQ) S&P 500 Sustainability Reporting and Assurance Analysis, 73% of the S&P 500 companies that reported sustainability information in 2023 obtained third-party assurance over at least part of that information. The CAQ is affiliated with the AICPA.

The ASB has also received feedback from the AICPA’s Assurance Services Executive Committee (ASEC), and other task forces and committees, on high-priority topics that warranted consideration for inclusion in the attestation standards. Standard setting was encouraged by ASEC and others to address these high-priority topics. (See Appendix A in the February 2026 ED for the list of high-priority topics and where they may have been addressed in the proposed Statement on Standards for Attestation Engagements (SSAE).)

Currently, practitioners often refer to other AICPA Professional Standards, such as Statements on Auditing Standards (SASs) and Statements on Standards for Accounting and Review Services (SSARSs), for guidance on how to address issues that arise during the attestation engagements for which relevant requirements and guidance are not included in the attestation standards themselves. But this workaround is not ideal and may result in inappropriate diversity in practice.

Though the attestation standards are meant to be self-contained, the expansion of subject matters and issuance of new SASs and SSARSs highlighted the need to consider enhancing or clarifying the baseline attestation standards.

What the ASB has done to address the evolving attestation landscape

In response, the ASB embarked on a comprehensive revision of certain AT-C sections of the attestation standards, as well as the development of new subject matter AT-C sections to provide requirements and guidance specific to engagements on sustainability information.

In doing so, the ASB sought to:

- Enhance the standards forassertion-based examination and review engagements to address those areas that had been identified as challenging in practice.

- Maintain transparency in the reports issued in accordance with the attestation standards.

On Feb. 26, 2026, the ASB issued an ED, proposed SSAE, Common Concepts, Examination Engagements, Review Engagements, and Engagements to Report on Sustainability Information. (See “Auditing Standards Board Proposes Changes to Attestation Standards,” JofA, Feb. 26, 2026.)

Subsequently, on March 25, 2026, the ASB issued related conforming amendments in an ED, proposed SSAE, Amendments to SSAE Nos. 18–19 and 21 to Reflect Proposed SSAE Common Concepts, Examination Engagements, Review Engagements, and Engagements to Report on Sustainability Information. Collectively, the EDs provide the proposed changes to the attestation standards.

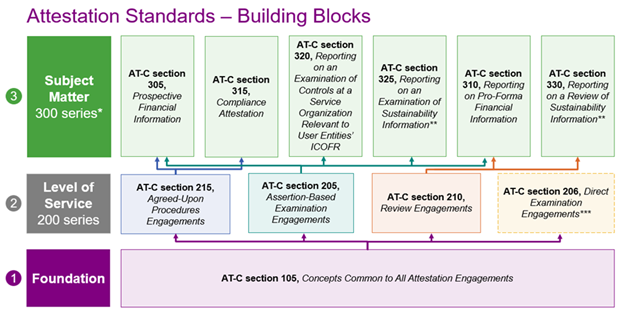

Structure of the attestation standards (the ‘building block approach’)

The attestation standards are structured using an approach wherein the AT-C sections are grouped in interrelated layers. This “building blocks approach,” in which the practitioner is required to apply two or more AT-C sections simultaneously when performing attestation engagements, depending on the level of service and the nature of the subject matter, is intended to be practical and flexible.

The AT-C sections in layers 1 and 2 are typically referred to as the baseline attestation standards (see the graphic, “Attestation Standards — Building Blocks”).

* The codification of the attestation standards includes a designated section for AT-C section 395, Management’s Discussion and Analysis. As the ASB is requesting feedback on potentially withdrawing this section, it was determined unnecessary to include this subject matter AT-C section in the graphic.

** Proposed subject matter attestation standard.

*** AT-C section 206 is not applicable to examination engagements related to subject matter for which other AT-C sections require the application of AT-C section 205. This includes all of the subject matter sections.

Source: AICPA.

Layer 1: The foundation

AT-C section 105 applies to all attestation engagements regardless of the service performed (i.e., examination, review, or agreed-upon procedures engagement).

Layer 2: The level of service (200 series)

The applicability of the AT-C section depends on the type of engagement being performed and, where applicable, the assurance intended to be obtained by the practitioner. The AT-C sections in the 200 series are drafted in a manner such that the principles-based requirements and the related application material are broadly relevant to all subject matters.

Note that AT-C section 206 does not apply to subject matter that requires the application of any of the AT-C sections in the 300 series.

Layer 3: The subject matter (300 series)

The subject matter-specific AT-C sections in the 300 series apply only when the section is relevant to the specific engagement circumstances. These sections include incremental requirements that build on, or are in addition to, the underlying requirements in AT-C section 105 or the 200 series.

For example, if a practitioner is engaged to report on an examination of sustainability information, the practitioner would apply AT-C sections 105, 205, and 325 (if issued as final) to the engagement being performed.

AT-C sections addressed by the February 2026 ED

The ED includes proposed revisions to the following AT-C sections:

- AT-C section 105, Concepts Common to All Attestation Engagements.

- AT-C section 205, Assertion-Based Examination Engagements.

- AT-C section 210, Review Engagements.

The ED also includes two new proposed subject matter sections:

- AT-C section 325, Reporting on an Examination of Sustainability Information.

- AT-C section 330, Reporting on a Review of Sustainability Information.

How the interconnectivity of the AT-C sections has been strengthened

The AT-C sections in the February 2026 ED include enhancements to the headings and section layouts. In addition, drafting conventions were adopted for the proposed new sustainability information AT-C sections in the 300 series that clearly indicate that, as part of performing the specified requirement in that other AT-C section, the practitioner is required to do more (as described in the 300 series).

The incremental practitioner action is intended to be specific and unique to the subject matter.

These improvements reinforce the interoperability of, and linkages between, the building blocks and provide a road map for the practitioner when applying multiple AT-C sections.

For example, when the same heading has been used in more than one AT-C section, it is easier for the practitioner to determine the interconnectivity of related requirements and guidance, including providing the practitioner with clarity as to which stage of the attestation cycle the performance requirements relate.

Amendments to other AT-C sections

The March 2026 ED includes proposed conforming amendments to the following AT-C sections:

- AT-C section 305, Prospective Financial Information.

- AT-C section 310, Reporting on Pro Forma Financial Information.

- AT-C section 315, Compliance Attestation.

- AT-C section 320, Reporting on an Examination of Controls at a Service Organization Relevant to User Entities’ Internal Control Over Financial Reporting.

- AT-C section 215, Agreed-Upon Procedures Engagements, as amended.

- AT-C section 206, Direct Examination Engagements, as amended.

Effective date

If issued as final, the proposed SSAEs will be effective for engagements beginning on or after June 15, 2029. Considering the “building blocks” concept, early implementation of a revised 200 series AT-C section would be permitted only if the practitioner also implements revised AT-C section 105. Early implementation of a revised or new 300 series AT-C section would be permitted only if the practitioner also early implements any other proposed AT-C sections that apply to the engagement.

How to participate in the comment letter process

The release of the EDs, and the request for respondents to participate in the comment letter process, is an invitation for stakeholders to provide their perspectives on whether the proposals continue to enable and support practitioners in performing high-quality attestation engagements effectively and efficiently, including whether:

- The revisions to the baseline attestation standards are appropriate and sufficiently robust to promote and drive consistency in practice.

- The new sustainability information AT-C sections are appropriate in the context of the U.S. jurisdiction.

Comments on the EDs are requested from respondents by June 30. Templates for comment responses have been posted for respondents to easily provide their feedback.

The series at a glance

The JofA is publishing three articles about the proposed enhancements to the attestation standards. These articles will cover:

• Part 1 (April 29): Structure of the attestation standards and proposed enhancements.

• Part 2 (May 7): Proposed revisions to examination and review engagements in the attestation standards.

• Part 3 (May 8): Proposed new sustainability information AT-C sections.

— Mike Glynn, CPA, CGMA, and Ahava Goldman, CPA, CGMA,are associate directors for the AICPA Audit and Attest Standards group. Sally Ann Bailey,CPA, Chartered Accountant (South Africa),serves as a consultant to the AICPA, working with technical staff on standard-setting activities. To comment on this article or to suggest an idea for another article, contact Jeff Drew at Jeff.Drew@aicpa-cima.com.