- feature

- TECHNOLOGY

How to develop and publish a mobile app

Compelling idea and solid plan are key to placing product in an app marketplace.

Please note: This item is from our archives and was published in 2013. It is provided for historical reference. The content may be out of date and links may no longer function.

Related

ENGAGE takeaways: 7 principles to improve CPA firm profitability

What it takes for a CFO to lead operations and tech

Rise2040: A human-led profession built on trust

When Susan Bruno set out to launch a mobile application to help women gain control of their finances, and Leonard Wright decided to develop an app to enhance his client interactions, neither wealth manager could foresee the dizzying array of detours and dead-ends they would encounter on the road to the app marketplace.

Bruno, CPA/PFS, managing partner of Connecticut-based Beacon Wealth Consulting LLC and co-founder of DivaCFO LLC, was forced twice to find a new vendor to write the code for her app, DivaDocs. Wright, CPA/PFS, a wealth management adviser in San Diego and co-host of a weekly radio show on financial planning, saw Apple reject his app multiple times. Both financial planners lost deposits when the developers they hired to build their apps either closed up shop or simply disappeared.

How can CPAs interested in launching a mobile app avoid the types of problems that plagued Bruno and Wright? What are the best practices in mobile app development? This article lays out a series of steps CPAs can follow as they seek safe passage through the mobile app minefield.

FILL A NEED

CPAs should not pursue the creation of a mobile application without a clear and compelling reason to do so. The road to submitting an app to Apple’s App Store or one of the myriad Android app stores is riddled with potholes that can knock the project off course or kill it, costing CPAs significant time and money.

“Don’t build an app just to have an app,” said Ben Schell, a website and mobile app developer and owner of Blue Pane Labs. “You’re going to end up with something that nobody really wants to use.”

To avoid that, CPAs should be able to answer “yes” to the following questions:

- Would the application address an unmet need in the marketplace?

- Would delivery to mobile devices enhance the value of the content or functionality the application would provide?

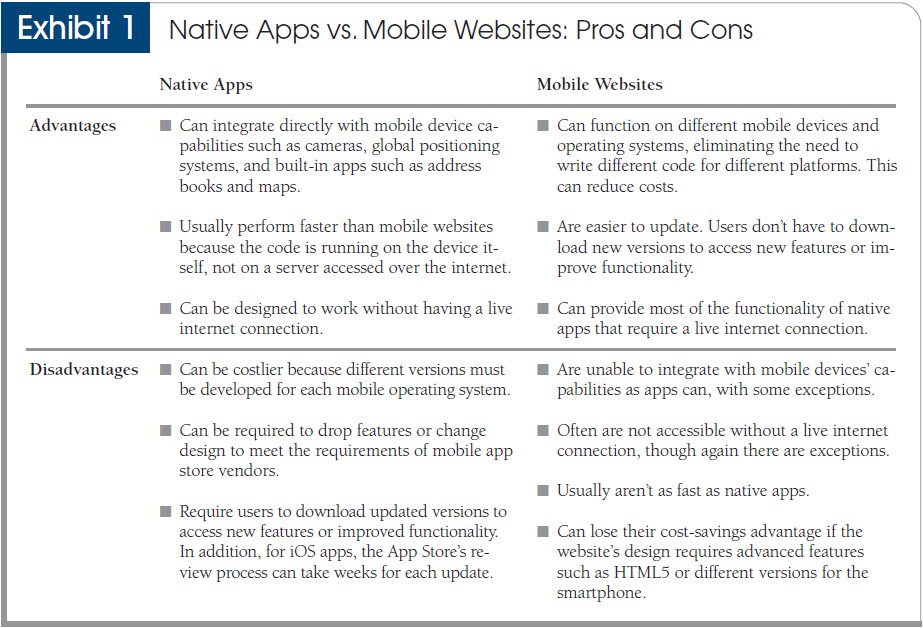

If those questions are answered in the affirmative, the next step is to determine whether the same functionality could be delivered as well or better through a mobile website. That decision requires an understanding of the differences between mobile apps and mobile websites:

- A mobile app is a software application designed to run on the “native” operating system of a mobile device. Native apps are not interchangeable, said Michael Ham, vice president of operations at CPA2Biz, the AICPA’s for-profit technology subsidiary and provider of technology development to the Institute. A native app designed to work on Apple’s iOS will not work on Android and vice versa.

- A mobile website is a website optimized for mobile devices. The content is reformatted—and often streamlined—to provide a better experience on mobile devices than the full website does. Mobile websites may also feature enhancements for touchscreen navigation. A single mobile website will work on a broad range of mobile browsers and devices.

This article focuses on the development process for native apps. For an expanded comparison of native apps and mobile websites, see Exhibit 1.

{kind=link}

For CPAs, native mobile apps should do at least one of the following, according to Ham:

- Expand the firm’s product or service offerings using the built-in capabilities of smartphones, such as cameras, global positioning systems (GPS), etc.

- Enhance the firm’s brand.

- Initiate interactions with clients that reflect the changes in communication methods being used at the client level. In other words, if clients are texting and emailing via mobile devices, their CPAs need to engage them in the same manner.

Bruno suggests that CPAs ask themselves this question: “Can I leverage my expertise and create a new virtual business from what I already know?” In Bruno’s case, she knew which vital personal and financial documents her wealth management clients have to gather when they work with her. She then applied that knowledge to design DivaDocs as a “scavenger hunt” that helps women (and men) track down those documents in a “fun way.”

Mobile apps create all kinds of possibilities for CPAs to inform, assist, and interact with clients (see Exhibit 2), but CPAs should resist the temptation to include too many features in a mobile app, especially their first one, said Ham, who believes that an app needs to do only one or two things well to merit consideration for development.

“Instead of having one app that does 50 things, it’s better to have 50 different apps,” said Ham, who led CPA2Biz’s development of the JofA’s iPad app and the CPA Exam Aid app for iOS and Android smartphones.

Mobile apps should not replicate the website of the CPA or the CPA’s organization, Schell said. Instead, apps should provide new content or functionality that offers value to the target-user market.

DETERMINE THE APP’S LOOK AND USER INTERACTIONS

Once it has been determined what the app will do, decisions must be made on what the app will look like and how it will work. Of particular importance is the appearance and functionality of the user interfaces (UIs). A UI refers to a meshing point where the user interacts with an application. UI elements include the design of menus and icons, the functionality of touchscreens, and the ease of navigation to the application’s various features.

For the visual elements, a professional graphic designer with experience designing mobile apps is a good option if the CPA’s organization does not have such capabilities in-house. Also, if the CPA pursuing the app hasn’t yet engaged someone with IT knowledge to help with the development process, this would be the time to do so. The right consultant can provide the expertise and experience needed to properly analyze apps. Some of the performance factors with apps are so subtle that it often takes a trained technical eye to spot flaws, Ham said (see Exhibit 3).

An IT consultant also can assist with the toughest and riskiest part of the process—the vetting and selection of a vendor to write the code for the app.

PROCEED WITH CAUTION

CPAs who opt to hire a contractor to build their app must venture into the world of mobile-app vendor vetting and selection, a largely lawless land that Bruno and Wright both labeled the “Wild West.”

The analogy is appropriate. There’s no official certification to distinguish the good developers from the bad developers.

“Anyone can say they are a mobile app developer,” Ham said.

And anyone can take a deposit, usually 50% of the overall cost, and then disappear with the money. That happened to both Wright and Bruno, whose bad experiences illuminate some of the dangers lurking in Dodge City (see sidebar, “Two CPAs and App Development: Lessons Learned”).

“Vendors can say anything,” Bruno said. “They overpromise and under-deliver.”

Steps CPAs can take to protect themselves when selecting a mobile app developer, or a mobile website developer, include:

- Obtain a list of apps or mobile websites developed by the vendor. Test those apps and gauge their performance on your mobile devices and the types of mobile devices you want to be able to run your app.

- Contact customers of the vendor to see what their experience was like. What went well? What could have gone better? Would they work with the vendor again?

- Request to see full technical specs for the app or mobile site that show in detail what the site would look like, how it would work, and whether the code used would allow for changes to function and design based on feedback in testing. If the vendor won’t provide this information, do not sign anything with the vendor. But don’t balk when the vendor says the tech specs will come with a cost. “It’s like an architectural blueprint and worth every penny,” Bruno said.

- Make sure the contract spells out in detail what the developer will produce, what the deadlines will be, and what consequences are attached to vendor failure to live up to the contract.

- Don’t rush into a contract. You need to negotiate terms from a position of strength. Don’t scramble to put together an app just to meet an artificial deadline.

- Negotiate not only the final price, but also what you will pay up front. While 50% is a common deposit for mobile app development, it is by no means the only option.

- Talk to as many developers as possible. This is where your consultant can help with initial interviews and screening. Your goal should be to create as much competition as possible to develop your site.

SET A BUDGET

The cost of building an app can range from a few thousand dollars to well into the six figures. Bruno, for example, invested about $100,000 to bring her app to market—a price tag that included not only the app developer and graphic artists for design, but also paying a full-time project manager to oversee the DivaDocs app and the DivaCFO blog and website. Other costs included engaging experts to provide media training and set up TV and radio interviews, and hiring attorneys to set up an LLC for the DivaCFO concept and to protect intellectual property. Wright, in contrast, spent between $3,000 and $4,000 for his app.

CPAs need to align their resources and goals for the app with how much the design and development will cost. To do that, CPAs should consider the main cost drivers in launching a mobile app:

- How much of the design and coding is customized. The more customization, the higher the price. The use of existing templates and coding can reduce costs but also places limits on the functionality and features that can be included in the app.

- The quantity and complexity of the features.

- The complexity of the functionality.

- The number of additions and changes made during the development process. This can range from new features to redesigned user interfaces. “It’s kind of like building a house,” Bruno said. “… The [final cost] is going to be 50% more.”

- The number of versions that must be produced. Tablets and smartphones require different specifications, as do different operating systems. If a CPA decides to build an app for the iPhone, it will cost “X” amount of money based on the other factors listed above. A decision to design apps customized for the iPad as well as the iPhone could double the cost, Ham said. The price for developing the app for the Android as well as Apple’s iOS could be double the price of building the app for just one operating system. “There could be up to four different versions you have to create,” Ham said. That could cost four times as much as building just one app, though Ham cautions that costs depend on scope and that it’s difficult to predict how much a developer’s final bill would be.

PICK THE BEST DEVICE(S) FOR AN APP

While the cost factor should carry a lot of weight in the decision on device and operating system for an app, there are other factors to consider:

- There are significant differences in the size and purpose of smartphones and tablets. Smartphones, for example, are ideal for the delivery of content that can be quickly consumed, while tablets are superior for reading long-form material.

- User smartphones almost always have an internet-access plan with a telecommunications carrier. Many tablet users can connect to the internet only via a Wi-Fi connection.

- Smartphones are far more widespread than tablets and more convenient to carry.

- Apps designed for Apple’s iOS will have a consistent user experience on each of Apple’s platforms because the company restricts the way consumers can use their iPhones and iPads. Android apps, in contrast, could be used in countless ways, and not just because there are hundreds of Android smartphones and tablets. If you put two people using the same app on identical Samsung Galaxy S III smartphones beside each other, the apps could look totally different, as could the way each person uses the app, Ham said. “[Users] can customize everything on Android,” he said. “You can change how it works.” That flexibility complicates the process of designing and coding apps for the Android.

Note: At the time this article was written, Android and iOS were the only operating systems with a significant presence in both the smartphone and tablet markets. Microsoft was attempting to catch up with Windows 8, but app development procedures for the platform were not well-established.

SELECT THE RIGHT STORES

Perhaps nowhere is the difference between developing mobile apps for iOS and Android more pronounced than in the process of accessing a distribution channel to get the app to its intended users.

Apple requires all apps for the iPhone, iPad, and iPod Touch to be distributed exclusively through its App Store. Google, in contrast, not only offers Android apps through its Google Play store, but also allows third-party stores to offer Android apps.

The result is two diametrically opposed app store experiences. Apple controls everything in its App Store. CPAs and others who would like to distribute through the App Store must first register as an Apple developer (even if the person filing the application isn’t the actual developer) and pay the associated annual fee, which is about $100, Ham said. The app must then be submitted to Apple, which thoroughly vets every app to make sure it meets the company’s standards.

“Apple will make sure the app works on all platforms it’s built for,” Ham said.

In addition, Apple will measure the app against its current acceptable-policies list. The review process takes one to two weeks due to the high volume of submissions to the App Store. Rejections are common and can come for many reasons.

“If you build an app strictly selling stuff to your clients outside of the Apple Store or iTunes, Apple will reject such apps,” Ham said.

Apple does not charge for making apps available in the App Store, but for apps that users must buy, Apple generally takes between 30% and 35% of the proceeds from each sale. In the case of DivaDocs, which sells for $4.99, Apple pockets $1.50 from each transaction, Bruno said.

Apple’s strict controls do produce a couple of advantages for consumers. First, there have been no reports of malicious software, or malware, being found on any apps distributed through the App Store. Second, the App Store and iTunes enjoy high name recognition and a strong reputation for quality.

It’s much quicker and easier to get an app into the Google Play store. Wright’s app appeared within 24 hours of submission, he said. The CPA Exam Aid app showed up almost instantly, according to Ham.

The process won’t necessarily be as easy with the hundreds of third-party Android marketplaces, which include those of Amazon, AT&T, Sprint, and Verizon, among other large players. “Each third-party marketplace has its own set of rules,” Ham said. “Amazon will reject anything that smells of eBooks.”

Third-party marketplaces also vary in focus. Some, such as Google Play, operate like a shopping mall, with something for everyone. Others, though, might focus on a niche.

Perhaps the biggest downside for users of the Android apps marketplace system is the risk of downloading malware. The proliferation of Android devices and third-party app markets has made the Android the top target of hackers writing malware for mobile devices.

“On Google Play, the insurance that you have is the user base themselves,” Ham said. “Malware might fool the first 10 or 100 people, but as soon as someone figures it out, the app is almost instantly pulled off the marketplace. Google will pull apps and revoke licenses. Still, it does lend itself to more risk than Apple.”

ON THE QA

Before sending an app to a store, a CPA should put it through a thorough quality assurance (QA) process. All features and functions of the app should be tested, as should all operating system-specific versions of the app.

QA testing is especially important because an app can’t be updated on the fly as websites can. As a result, if there is a major problem with an app, all corrections must be distributed via a new version of the app. Users who don’t download the new version won’t have access to the corrected code. In addition, the update process can take a great deal of time, especially at the App Store, where it can take weeks to get an update approved for distribution.

Despite the distribution hurdles, the update process should not be ignored. CPAs should not fall into the trap of paying to develop an app and then paying no attention to it after it is released to the market. A content app needs a steady supply of fresh content, for example. Otherwise, it will look neglected and outdated—not exactly a good image to convey to clients on their mobile devices.

CONCLUSION

Mobile apps offer CPAs powerful new ways to engage clients and empower employees on the devices they prefer to use. From the timely delivery of targeted content or instant access to financial tools and advice, mobile apps can provide information and interactive features that help individuals and businesses make better decisions with their money. Providing actionable intelligence clients can use aligns with the CPA’s core purpose of “making sense of a changing and complex world.” Still, CPAs should enter into mobile app development only if there is a compelling reason to do so and they have a clear understanding of the work involved and the risks inherent in the app development process.

Two CPAs and App Development: Lessons Learned

Susan Bruno and Leonard Wright had dramatically different visions for their mobile apps but ran into similar problems during the development process. Following are their stories and the lessons they learned about building and launching mobile apps.

The Wright Stuff

Wright’s goal for his app was straightforward: communicate with his clients in a manner more welcoming and engaging than email.

The idea came to him during dinner with a client. During the discussion that evening, which focused on how Wright communicated with his clients and also on the communication methods he preferred to use on his smartphone, Wright realized that while he deleted more than half of the emails he received, he always took notice of the content delivered by apps he had downloaded.

“If I have an app, I have an app for a reason, and that reason is that I’m interested in whatever that app delivers to me,” he said.

After that dinner, Wright paid particular attention to how his clients interacted with their mobile devices. He noticed that in meetings and at meals, his clients often left their smartphones on the table. When the device made a sound indicating a message had come in, the clients usually would take a quick look at their screen. When Wright asked them what they had glanced at, they often told him that they were checking on alerts to content delivered to their phones by various apps. The clients would not open the message and access the full content during their meetings with Wright, but they would take note of what was delivered and check it more thoroughly after the meeting.

Those client conversations convinced Wright that the best way to interact with his clients was by developing an app that clients would download. Wright could then deliver financial information and other content of interest to his clients.

Wright sketched out the concept for his idea in 10 minutes on a napkin; then he began the process of bringing his app from concept to reality. He selected a veteran business executive-turned-mobile app developer in Kansas City, Mo., who was highly recommended by one of Wright’s clients. The developer worked with Wright on the app, making changes at Wright’s request and adding features. It appeared that Wright had found the perfect person to develop his app. That is, until that person, and Wright’s deposit, disappeared.

“[He] never returned phone calls, never returned emails,” Wright said. “He was just gone.”

Forced to start from scratch, Wright found a Nevadan, Lisa Wark, who had taught herself how to write code for mobile apps. She was able to re-create his app for the iOS and Android operating systems for smartphones.

Next came the task of submitting the app to the Google Play and Apple iTunes app stores. Submission to the Google Play store went smoothly. The mobile application was up and available for download within 24 hours.

It took three months to achieve the same result with Wright’s iPhone app. Apple rejected the app three times for a variety of reasons. Apple would not allow it to have YouTube videos, so those had to be removed. Apple also objected to some of the design elements, all the way down to the colors of some of the text.

“Apple wants everything to have the same look and feel,” Wright said.

Despite the setbacks and delays in the app development process, Wright believes apps are the future of CPA-client communications and that CPAs, especially those who do personal financial planning, can leverage the technology to create a competitive advantage.

“The key here is accessibility to what it is you want to deliver on everybody else’s time schedule,” he said.

The Story of a DivaCFO

DivaDocs is part of Bruno’s DivaCFO concept, which includes a website and blog. Bruno set up DivaCFO LLC to own the rights to DivaCFO’s assets, including DivaDocs, and to protect the owners’ personal assets. DivaDocs represents a roll of the dice that Bruno recommends CPAs take on only if they have another strong source of income.

Bruno also advises CPAs against signing any agreements with app vendors that don’t agree to provide full technical specifications and wire framing to show how the app would look and detail how it would work. In addition, CPAs should consider only vendors that can produce dynamic code, a type of programming language that allows for rapid modifications to functionality and design.

These are lessons learned the hard way. The first vendor Bruno selected did not provide tech specs and could write only in static code, which could not accommodate changes in functionality during the development process. That was unacceptable to Bruno, who anticipated having to make changes to her app, which helps users find and organize financial documents by playing a game that’s a mix of a scavenger hunt and the social app Foursquare. Bruno anticipated that testing during the development process would reveal the need for changes to the app’s functionality (which proved to be true), and she was willing to pay for those changes. What she was unwilling to do was start over from scratch, which would have been required for her first vendor to change functionality after coding began.

Bruno learned about the tech specs and the difference between static and dynamic coding from an IT consultant she hired while still working with the first vendor. She then pulled out of the $35,000 project for which she had paid the industry-standard 50% upfront in the form of a nonrefundable deposit.

“It was a good learning experience,” she said.

Bruno was fortunate that her first vendor chose to give her a full refund. She would not be so fortunate with the second vendor, Appiction.com, an Austin, Texas-based company that boasted 55 employees and a strong track record of app development with clients including IBM, Samsung, and the state of Texas. Bruno’s IT consultant vetted the company and confirmed it had the technical knowledge to handle her project. After meeting with a 12-person project team at the vendor’s offices, Bruno was given a $50,000 quote to develop the app. Bruno paid $35,000 upfront because the vendor told her that paying more than half would move her project up in the development schedule, and she wanted the app delivered in time for the 2012 tax season.

That didn’t happen. Within a few weeks, Appiction.com was out of business and Bruno was out $35,000. The company shut down in October 2011 and later filed for Chapter 7 bankruptcy liquidation.

“We’ll never see that money again,” Bruno said.

Bruno found yet another vendor, Colleen Tully, at a two-person shop in Colorado, and arranged a deal in which Tully agreed to build the app in exchange for a 15% stake in DivaCFO LLC. Tully produced the iPhone app, which Apple accepted on its first submission after a two-week vetting period. The app became available on July 12, 2012, for $4.99.

Michael Ham, vice president, technology, CPA2Biz, discusses how mobile apps can help firms attract and retain clients:

EXECUTIVE SUMMARY

Mobile applications can offer CPAs new ways to engage clients and colleagues on their smartphones and tablets. Opportunities exist in the areas of content delivery and enhanced, interactive communications.

Do not invest time and money into developing a mobile app unless there is a clear and compelling reason. Apps should provide a new product, service, or form of interaction with clients in a manner that is significantly enhanced by delivery through a mobile device. Don’t build an app just to build an app.

Once a strong app idea is established, decide whether to build a mobile-optimized website or a “native app.” Mobile websites are hosted on the internet and are designed to work on multiple mobile devices and operating systems. Native apps are designed to be downloaded to a device and work exclusively on that platform. For example, an iPhone app running on Apple’s iOS won’t work on an Android smartphone or tablet.

CPAs who aren’t website experts should consider hiring a consultant who can advise on app design, vendor vetting, device selection, and app store submissions. Look for experience with app development when choosing a consultant.

Choose which devices and operating systems will run the app. Keep in mind that the costs will rise with each version of the app that is created.

Once the design and functionality of an app is mapped out, the next step is to find someone to write the actual code. This is the most vexing part of the process. Without an official body to sanction app developers, it’s difficult to tell the good vendors from the bad ones.

The costs of building an app can range from a few thousand dollars to well into the six figures. Budget accordingly.

Make sure to do thorough quality assurance testing on your app before submitting it to an app store. The release of an app that doesn’t work right will hurt your brand and could lead to costly revisions.

The Apple App Store puts app submissions through a thorough review process that can take weeks and often results in a rejection. Understanding the App Store’s rules and developing the app to comply with App Store policy is the best approach to break through Apple’s red tape.

Jeff Drew is a JofA senior editor. To comment on this article or to suggest an idea for another article, contact him at jdrew@aicpa.org or 919-402-4056.

AICPA RESOURCES

JofA articles

- “Windows 8: Jump or Wait?” Nov. 2012, page 40

- “Managing Cybersecurity Risks,” Aug. 2012, page 44

- “Technology and CPAs: Visions of the Future,” June 2012, page 110

- “125 Technology Quick Tips,” June 2012, page 130

CPE self-study

IT: Risks and Controls in Traditional and Emerging Environments [ITRC] (#733520)

Conference

Practitioners Symposium and Tech+ Conference in partnership with the Association for Accounting Marketing Summit, June 10–12, Las Vegas

For more information or to make a purchase or register, go to cpa2biz.com or call the Institute at 888-777-7077.

Private Companies Practice Section and Succession Planning Resource Center

The Private Companies Practice Section (PCPS) is a voluntary firm membership section for CPAs that provides member firms with targeted practice management tools and resources, including the Succession Planning Resource Center, as well as a strong, collective voice within the CPA profession. Visit the PCPS Firm Practice Center at aicpa.org/PCPS.

Information Management and Technology Assurance (IMTA) Section and CITP credential

In an effort to better recognize and support the breadth of its members’ professional duties and responsibilities, the AICPA has changed the name of the Information Technology Section to the Information Management and Technology Assurance (IMTA) Section. The IMTA division serves members of the IMTA Membership Section, CPAs who hold the Certified Information Technology Professional (CITP) credential, other AICPA members, and accounting professionals who want to maximize information technology to provide information management and/or technology assurance services to meet their clients’ or organization’s operational, compliance, and assurance needs. To learn about the IMTA division, visit aicpa.org/IMTA.