- feature

- FINANCIAL REPORTING

Three common currency-adjustment pitfalls

How to correctly account for foreign-currency translations

Please note: This item is from our archives and was published in 2012. It is provided for historical reference. The content may be out of date and links may no longer function.

Related

GASB proposes guidance on infrastructure assets

FASAB announces new chair, new board structure

SEC accepting Professional Accounting Fellow applications

Although the rules on accounting for foreign-currency translations have not changed in many years, mistakes in this area persist. Such mistakes can result in misstatements in financial reporting, hurting the bottom line, creating false understandings of business results, and exposing companies to possible regulatory scrutiny.

A key factor raising the stakes in foreign-currency reporting is the fact that U.S. companies are increasingly looking offshore for growth. U.S. exports are growing at a healthy pace, as a slumping dollar makes goods from the U.S. less expensive overseas. With the increase in foreign transactions comes a parallel increase in foreign-currency reporting, and since many companies do business in multiple countries, the complexity of such reporting is on the rise.

The risk of accounting errors in foreign-currency transactions has been compounded by significant volatility in the value of the U.S. dollar compared with some other currencies, especially in the past 18 months. And this volatility will likely continue, given recent headlines, such as the spike in the yen’s value following Japan’s devastating earthquake last March, the rise of China’s yuan to a new high versus the U.S. dollar last summer, and runaway inflation in developing countries such as Venezuela.

THREE COMMON MISTAKES

As U.S. companies expand their presence in global markets, it is more important than ever to understand and address the most common pitfalls associated with working with foreign currencies. This article examines three frequent mistakes that accountants make regarding the reporting of foreign currencies. Avoiding these pitfalls can make a big difference to companies’ financial statements.

Mistake 1: Hiding foreign-currency gains and losses in other comprehensive income (OCI) instead of recognizing them in net income. The first common mistake is difficult to detect without knowing how the accounting system consolidates subsidiaries. This mistake occurs when a company misclassifies a foreign-currency gain or loss in OCI instead of net income. Such a misclassification sounds benign, but it misstates net income and hides the gain or loss in an account that is normally presented as part of the statement of changes in equity.

This mistake can arise when a company has an intercompany account (for example, a parent’s intercompany receivable from a subsidiary) recorded on the books of companies with different functional currencies. The issue boils down to how to account for an intercompany balance when each of the parties has the balance recorded in different currencies (for example, the parent company records the balance in U.S. dollars, while the subsidiary records the balance in euros).

To illustrate, assume that on Jan. 1, 2011, Parent Company A lends $10 million to its subsidiary in Germany, and the loan is payable in U.S. dollars. On that date, Parent Company A records a $10 million receivable on its balance sheet, and the subsidiary records €6,961,000 on its balance sheet. Assuming the German subsidiary used the exchange rate of $1 = €0.6961 in its journal entry, the intercompany balance should be eliminated when the euro balance is translated to U.S. dollars, as shown in Exhibit 1.

Now assume that no other entries are recorded to this account, but that on March 31, 2011, Parent Company A must report its financial statements. The prevailing exchange rate on that date is $1 = €0.7433.

Solely because of the change in the exchange rate, the company’s intercompany accounts (prior to any currency translation adjustments) no longer balance, as shown in Exhibit 2.

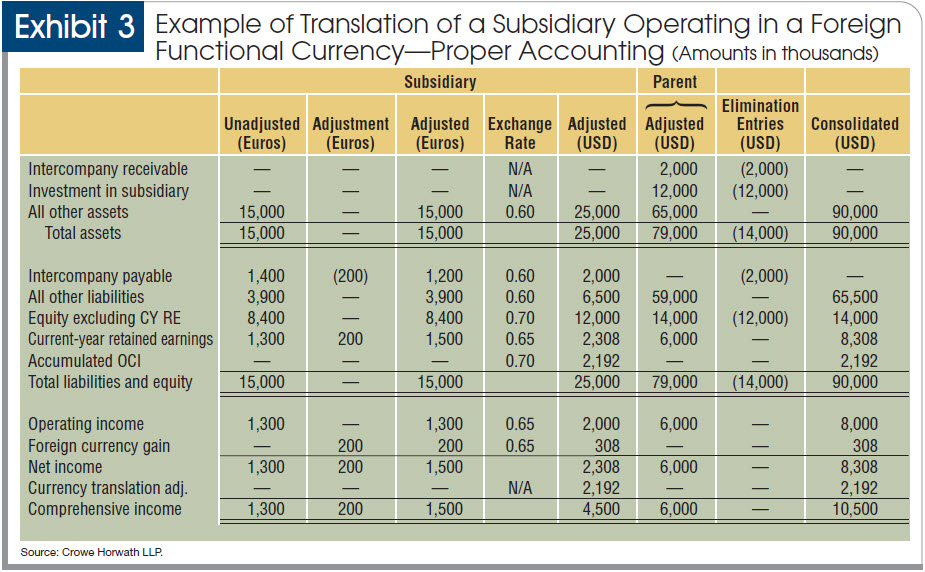

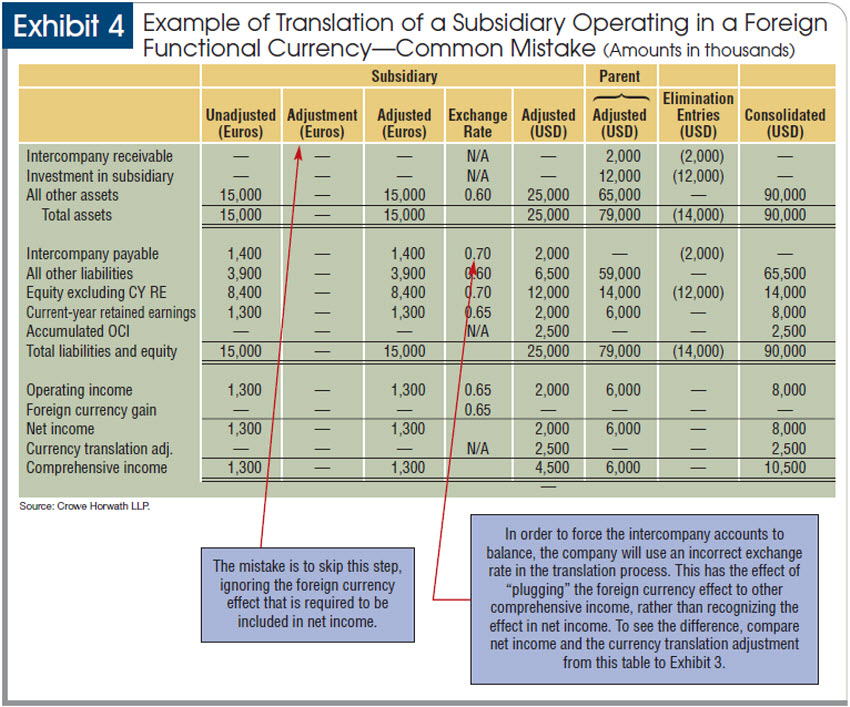

Therefore, the German subsidiary must adjust its liability to Parent Company A from €6,961,000 to €7,433,000. The subsidiary will credit its liability for €472,000. The question is how the German subsidiary should record the offsetting debit to this transaction. The common mistake is to record the debit side of this transaction as part of the currency translation that is included in OCI. Generally, the debit side of this transaction should be included in net income rather than only as a component of OCI.

There is one exception to the general rule, however. Foreign-currency gains and losses on intercompany accounts that are essentially permanent are excluded from the determination of net income and instead are recorded as OCI. In essence, if the intercompany account is essentially a permanent investment in the subsidiary, the gain or loss on that account should be excluded from net income. Unless the intercompany account meets this narrow exception, foreign-currency gains and losses on intercompany accounts should be included in determining net income.

Normal intercompany accounts will generate a gain or loss that is ordinarily reflected on the books of the subsidiary operating in a functional currency other than the reporting currency of the parent company. This gain or loss will not be eliminated in consolidation. This point seems counterintuitive and could be at the root of many errors in this area.

Exhibit 3 shows an example of the translation of a subsidiary operating in a foreign functional currency under the proper accounting, while Exhibit 4 shows an example of the common mistake. In these examples, a parent company lent $2 million to a subsidiary whose functional currency is the euro. The subsidiary recorded the amount on its books at the rate in effect at that time—$1 = €0.7000. At the next reporting period, the applicable exchange rate was $1 = €0.6000. As you compare Exhibit 3 to Exhibit 4, notice how subtle the error can appear.

{kind=link}

{kind=link}

Mistake 2: Preparing the consolidated statement of cash flows based on amounts reported in the consolidated balance sheets. The second common mistake is misstating the statement of cash flows by allocating changes in cash flows from the effects of foreign-currency rates among individual cash flow line items. U.S. GAAP requires that the statement of cash flows present changes in cash flows at the rate in effect on the date the cash flows took place, although the rules permit use of the average rate in effect during the period if it reasonably approximates the timing of cash flows.

The issue is that many preparers present the statement of cash flows under the indirect method. When preparing the statement of cash flows for a consolidated company that deals in more than one functional currency, it is simple to prepare a statement of cash flows based on the consolidated balance sheets of the current and prior periods—simple, but not correct. The consolidated balance sheets have been prepared using the exchange rates in effect on each balance sheet date; cash flows, however, should be translated into the reporting currency using the average exchange rate in effect during the period. The differences between those rates can be significant.

Even if the difference between exchange rates is relatively small, the error is often obvious on the face of a company’s financial statements because either the statement of cash flows will omit the line item used to account for the effects of foreign currencies on cash flows or changes in cash flows will, on their face, correspond to changes in amounts reported on the consolidated balance sheets.

The right way to prepare a consolidated statement of cash flows requires a bit of work. The statement should be prepared using cash flow activity at the functional currency level that has been translated to the reporting currency using the average exchange rate in effect for the period. For example, a parent company reporting financial statements in U.S. dollars that has subsidiaries using the euro and the yen should prepare three statements of cash flows—U.S. dollar, euro and yen. The statements prepared in euros and yen for each of the subsidiaries would be translated into U.S. dollars using the average exchange rate in effect, and all three would be combined, considering elimination entries, to create the consolidated statement of cash flows.

(Click here to download Exhibits 5 and 6, illustrations of the correct and incorrect ways to prepare a consolidated statement of cash flows.)

Mistake 3: Failing to recognize the need to modify accounting for foreign-currency translations in highly inflationary environments. Companies may fail to recognize that they are operating in an economy that has become highly inflationary, and hence do not appropriately modify their accounting for foreign-currency translations. Essentially, they continue to recognize currency translation adjustments in OCI and continue to translate all assets and liabilities at current translation rates.

However, under U.S. GAAP, the financial statements of the foreign entity operating in a highly inflationary environment are required to be remeasured as if the functional currency were the reporting currency, which generally results in translation adjustments’ being reported in earnings currently and requires that different procedures be used to translate nonmonetary assets and liabilities.

An example of this is Venezuela, which reached highly inflationary status for U.S. GAAP purposes effective Nov. 30, 2009. On that date, a U.S. company with a Venezuelan subsidiary would cease using bolivars as the functional currency of the Venezuelan subsidiary. The subsidiary would remeasure assets and liabilities into U.S. dollars as of Nov. 30, 2009, and those amounts would become the accounting basis of assets and liabilities for the Venezuelan subsidiary. Going forward, the subsidiary should measure monetary assets and liabilities at current (that is, balance sheet) exchange rates and recognize a gain or loss on that translation in net income. This diverges significantly from the rules prior to the application of highly inflationary accounting where such gains and losses would be recognized only in OCI.

THREE WAYS TO MITIGATE THE RISK OF MISSTATEMENT

Companies can reduce the risk of misapplying the accounting rules for foreign-currency translations and, in turn, misstating the financial statements, by taking these three steps:

Step 1: Adopt understandable accounting policies. U.S. companies operating in foreign countries should develop and adhere to a strong companywide policy on the translation of intercompany accounts. In other words, a company should have clear guidelines that lower-level accounting personnel can follow easily. A well-documented policy would educate personnel on appropriate accounting for foreign-currency transactions and would embed the necessary periodic translation adjustments into the company’s normal month-end close procedures.

Step 2: Scrutinize the system. Global companies also should ensure that each accounting system used to perform consolidation procedures handles the processes in compliance with U.S. GAAP. Ideally, the system will allow users to see a clear trail of foreign-currency translations that can be tracked back from the financial statements. Companies that use a “black box” system, where financial statements come from subsidiaries in a foreign currency and the system spits out the consolidated financial statements, might have more difficulty detecting foreign-currency errors. These companies should be able to look behind the accounting system’s “curtain” to understand how accounts are translated and consolidated.

Step 3: Implementing adequate internal controls. Global companies also should implement internal controls designed to analyze and detect misstatements in foreign-currency gains and losses. These controls should analyze accounts included in net income and the translation account included in OCI. The controls also should monitor the company’s activities for significant or unusual foreign-currency transactions.

IFRS VS. U.S. GAAP

The three mistakes discussed here can occur regardless of whether a company applies IFRS or U.S. GAAP. However, it’s worth noting how differences in the rules between IFRS and U.S. GAAP could affect the mix of functional currencies used by global companies.

The substantive differences between IFRS and U.S. GAAP come into play only in highly inflationary environments or when selecting or changing a company’s functional currency. Once an entity is determined to be operating in a highly inflationary environment, IFRS and U.S. GAAP diverge significantly. IFRS uses an approach that restates historical amounts (potentially including the prior-year comparative amounts) into their current value, using end-of-period rates. U.S. GAAP, on the other hand, dictates that the entity adopt the reporting currency as its functional currency.

Upon selecting a functional currency, IFRS identifies primary and secondary factors to consider. U.S. GAAP also lists factors for consideration in selection but assigns equal weight to them. When a company changes its functional currency, IFRS always accounts for the change prospectively. U.S. GAAP, however, in certain circumstances requires retrospective application of the change.

IFRS and U.S. GAAP also use different nomenclature for foreign-currency matters. For example, IFRS refers to “presentation currency,” but U.S. GAAP uses “reporting currency.” However, other than the differences noted above, the two bases of accounting are equal, and accordingly, the mistakes described here could occur whether a company applies IFRS or U.S. GAAP.

Click here to download detailed examples of Mistake 2.

EXECUTIVE SUMMARY

Foreign currency is playing a bigger role in financial reporting as U.S. companies increasingly look to foreign markets for growth.

Companies participating in foreign markets should be aware of three common mistakes in accounting for foreign currency. They are hiding foreign- currency gains and losses in other comprehensive income rather than recognizing them in net income; preparing the consolidated statement of cash flows based on amounts reported in the consolidated balance sheets; and failing to recognize the need to modify accounting for foreign-currency translations in highly inflationary environments.

Companies can reduce their risk for misapplying the accounting rules for foreign-currency translations in three main ways: adopting understandable accounting policies; using appropriate models; and implementing adequate internal controls.

Companies need to stay on top of foreign-currency-translation accounting. With the level of foreign activity increasing, it’s easy to make costly mistakes on financial statements.

Scott L. Spencer (scott.spencer@crowehorwath.com) is a partner, and Glenn E. Richards (glenn.richards@crowehorwath.com) is a senior manager with Crowe Horwath LLP, both in the Oak Brook, Ill., office.

To comment on this article or to suggest an idea for another article, contact Kim Nilsen, executive editor, at knilsen@aicpa.org or 919-402-4048.

AICPA RESOURCES

JofA articles

- “Currency Translation Adjustments,” July 2008, page 42

- “Found in Translation,” Feb. 2007, page 38

Publication

- IFRS Accounting Trends & Techniques (#0099110, paperback; #WIF-XX, online subscription)

CPE self-study

- IFRS: Foreign Currency (IAS 21) (#159744)

- International Versus U.S. Accounting: What in the World is the Difference? (#153284)

For more information or to place an order, go to cpa2biz.com or call the Institute at 888-777-7077.

Website

IFRS Resources, ifrs.com

More from the JofA: