Ways to de-risk concentrated stock portfolios

Learn how investors can manage concentrated stock risk with minimal tax impact — and why CPAs should know the options.

U.S. investors hold roughly $1 trillion in concentrated portfolios that each consist of a small number of stocks, or even a single stock, acquired through various channels, including inheritance, compensation, and successful ventures. Holding a significant portion of one’s wealth in a concentrated portfolio is much riskier than owning a diversified portfolio, but investors averse to paying tax on capital gains may be hesitant to sell.

There are remedies, however. Investors can choose from several risk-reduction strategies that mitigate the downside risk in a concentrated portfolio with minimal tax cost. These solutions, such as tax-loss harvesting, involve tax and investment considerations and trade-offs. Integrating both tax and investment considerations into the process of tax-efficient risk reduction may lead to improved after-tax outcomes.

SINGLE STOCKS ARE RISKIER THAN DIVERSIFIED BENCHMARKS

Long-term investors in broadly diversified U.S. equity portfolios have enjoyed enviable returns for decades. This can be seen in the Russell 3000 Index, a capitalization-weighted benchmark that measures the performance of the largest publicly held companies in the United States. A starting position of $100,000 in the Russell 3000 Index on Jan. 1, 1987, translated to approximately $5.2 million at the end of 2023.

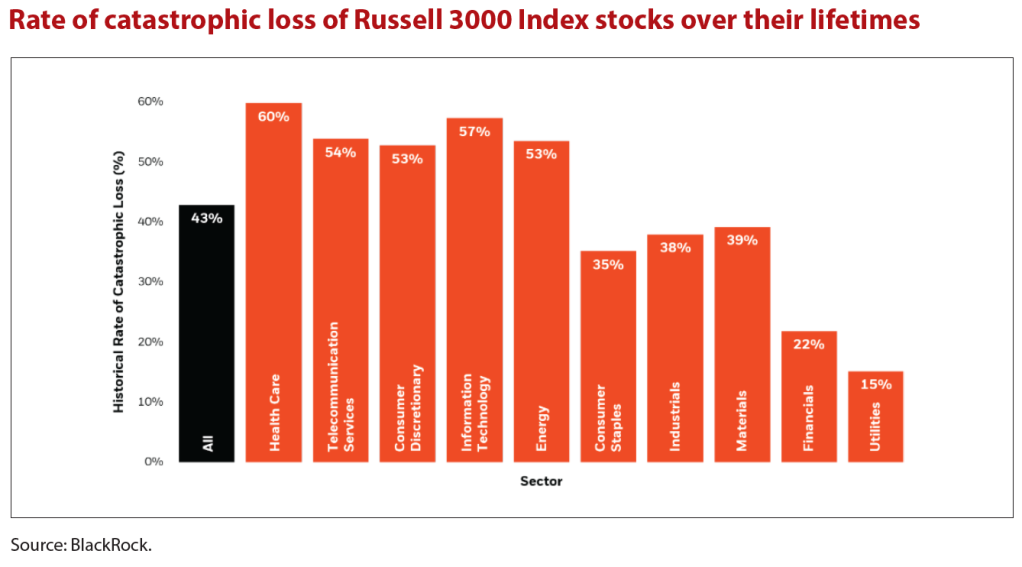

However, this remarkable fortune was not evenly shared by index constituents; there was a wide distribution of outcomes for single stocks. Between 1987 and 2023, two-thirds of stocks underperformed the Russell 3000 Index over their lifetimes, and 43% underwent a catastrophic loss, meaning they experienced a decline of 50% or more from their peak and did not recover. (See the chart “Rate of Catastrophic Loss of Russell 3000 Index Stocks Over Their Lifetimes,” below.)

U.S. market growth has historically been driven by a few exceptional performers. However, the winners’ identities varied from period to period. Winners did not necessarily continue to win.

To illustrate, BlackRock researchers noted, on each of a series of analysis dates, the 25 stocks in the Russell 3000 Index that had the highest returns over the prior decade. By construction, these stocks massively outperformed the index in the 10 years leading up to the analysis date, but how did they perform in the subsequent decade? An average over all the securities on all the analysis dates shows underperformance. (See the chart “Average Performance of High-Returning Stocks in the Decade Following Their Success,” below.)

These empirical facts may motivate some investors holding concentrated, appreciated portfolios to consider downside risk reduction.

METHODS FOR TAX-MANAGED RISK REDUCTION

Once a client decides to reduce their risk in a concentrated portfolio, what strategy or strategies should be considered to maximize after-tax wealth and achieve other goals?

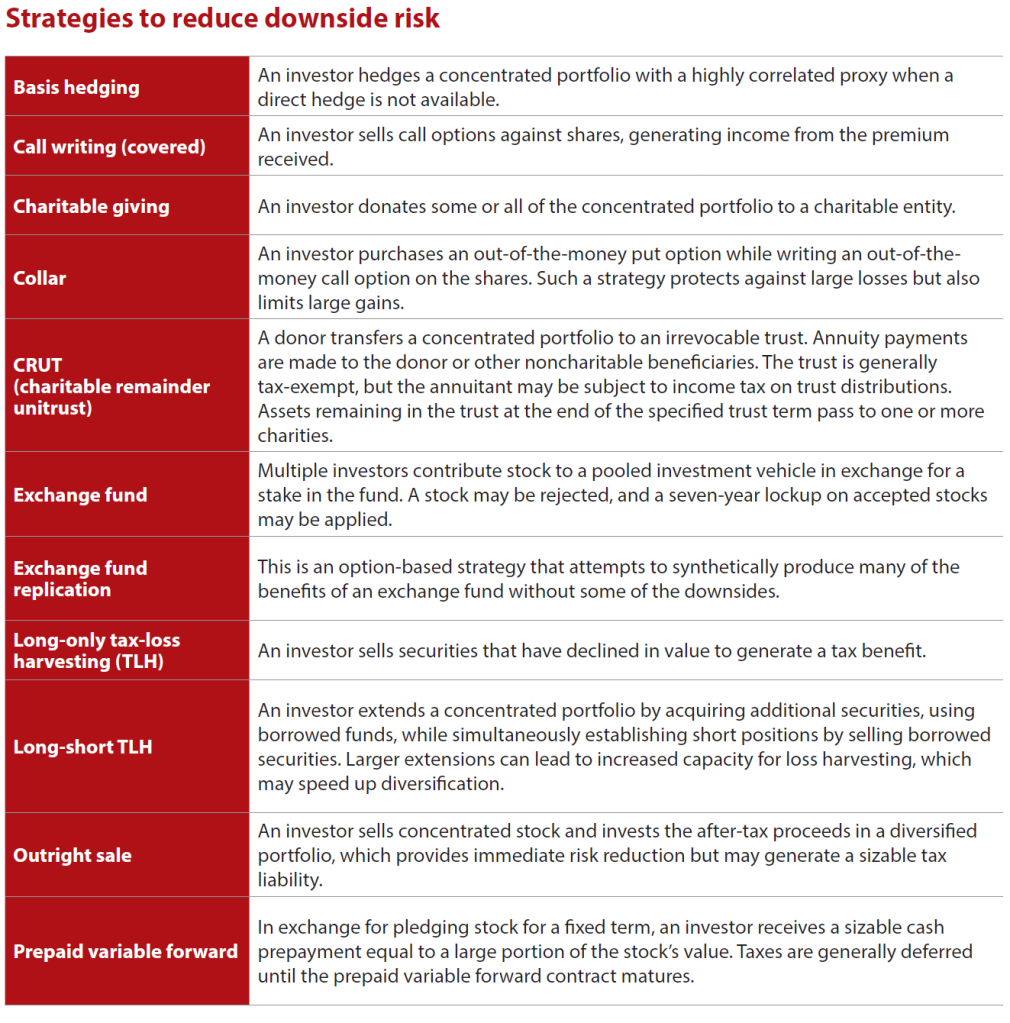

A client may choose to divest, hedge, or diversify a concentrated portfolio, with varying degrees of tax efficiency. (See the chart “Strategies to Reduce Downside Risk,” below.)

CRUTs

Tax and financial advisers have used some of these risk-mitigation strategies for many years. Several examples reflect philanthropic intent, including charitable remainder unitrusts (CRUTs) and outright charitable donations. CRUTs are frequently used to tax-efficiently diversify a concentrated portfolio.

Here’s how they work: A donor transfers highly appreciated, concentrated property to the trust. The donor may receive an upfront charitable deduction. The trustee can liquidate the concentrated property and reinvest the proceeds. Annuity payments are made to one or more noncharitable beneficiaries, providing a stream of income.

The trust is a tax-exempt entity, and capital gains realized by the trust are generally not taxable to the noncharitable beneficiaries until they are distributed out of the trust. The trust is irrevocable, and at the end of its term, any remaining assets pass to one or more charities.

Other investors with concentrated wealth and charitable utility may desire to immediately support causes that are important to them while reducing their overall tax burden and lowering the concentration risk in their portfolio. Investors who donate long-term appreciated securities to one or more charities may realize several important tax benefits:

- The donor may receive a charitable income tax deduction.

- The donor may avoid capital gains taxation on the unrealized appreciation.

- Wealthy investors who donate to charity may lower their taxable estates.

Such tax savings could be used to further divest from the concentrated portfolio tax-neutrally.

Tax-loss harvesting

Several other risk-mitigation solutions involve tax-loss harvesting, a commonly used investment strategy that strives to procure a tax benefit by selling securities that have decreased in value and delaying or avoiding selling securities that have increased in value. Harvested losses may be used to offset other sources of capital gains and limited quantities of ordinary income.

Loss harvesting enables investors to capitalize on market volatility to boost overall after-tax returns and achieve other desirable investment objectives, such as tax-efficient reduction of a concentrated portfolio.

Opportunities to harvest losses in a diversified equity, long-only portfolio may be abundant early in the strategy’s life. However, as lower-basis tax lots become more prevalent, and the portfolio appreciates over time, opportunities to harvest losses may diminish. Contributing fresh cash to the portfolio elevates the overall cost basis and may enable additional opportunities to harvest losses. Relaxing the long-only constraints and adding long and short extensions to create a tax-managed long/short portfolio may be another way to rejuvenate loss-harvesting opportunities.

Tax-neutral diversification with a long/short strategy

While tax and financial professionals may be acquainted with many traditional risk-reduction strategies, some may be less familiar with loss harvesting in a long/short portfolio — an innovative approach that enables tax-neutral diversification of concentrated portfolios without incurring immediate capital gains taxes.

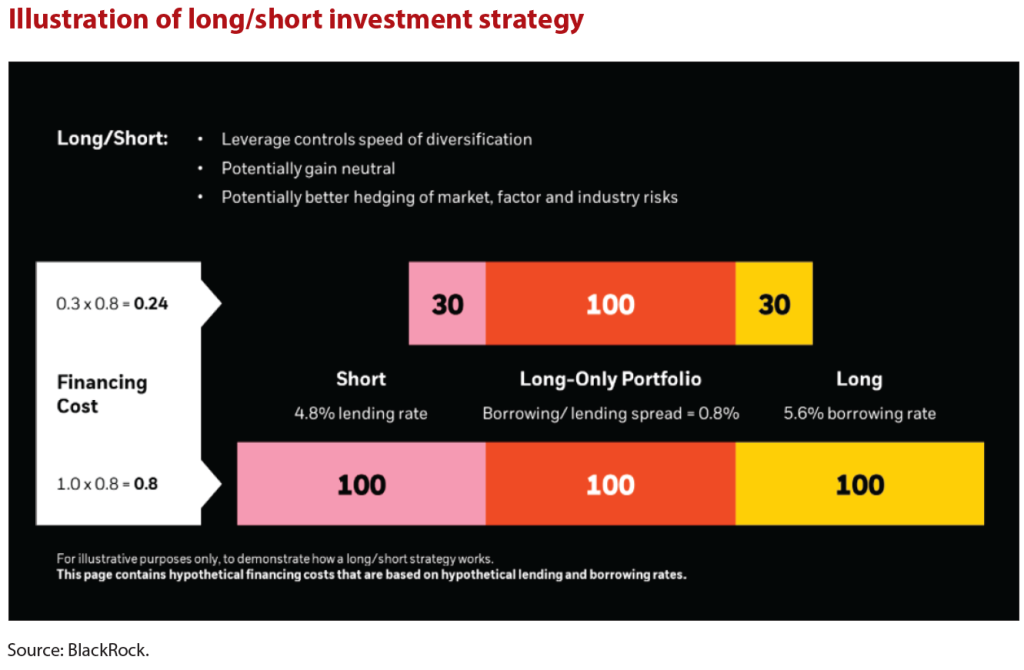

Under this strategy, an investor extends a concentrated portfolio by acquiring additional securities using borrowed funds while simultaneously establishing short positions by selling borrowed securities. The long and short extensions are expressed as percentages, typically equal in magnitude, of the concentrated position’s value. These extensions are carefully constructed so that the returns of the long/short portfolio track the returns of a broad market index as closely as possible.

A long/short strategy is quantified by its gross exposure, which is the sum of the dollar values of the concentrated position and the positions in the long and short extensions as a percentage of the dollar value of the concentrated position. For instance, in a long/short portfolio in which extensions are each 30% of the concentrated portfolio, gross exposure is 160. That long/short portfolio is denoted as LS130/30. Similarly, in a portfolio where the dollar values of the long and short extensions are each 100% of the concentrated portfolio’s dollar value, gross exposure is 300. That long/short portfolio is denoted as LS200/100. Greater gross exposure is associated with greater loss-harvesting capacity and hence more rapid diversification.

Because the sizing of a long/short diversification strategy is also associated with greater financing costs and risk, the trade-off between an investor’s desired speed of diversification and tolerance of financing costs and risk determines the sizing.

Investors enhance the concentrated position by purchasing additional securities for a long extension with borrowed funds and creating a short extension by selling borrowed securities. Long and short securities are chosen to minimize risk to a diversified benchmark. Net financing costs are the difference between the borrowing rate for the long extension and the lending rate on funds from the short sale, scaled by the size of the extensions. (See the chart “Illustration of Long/Short Investment Strategy,” below.)

The proceeds from tax-neutral liquidation of concentrated positions are reinvested in the long/short portfolio, resulting in a new set of securities with high-cost bases, with potential for future loss harvesting and possible further acceleration of diversification. The portfolio manager can begin to unwind portfolio leverage once the target weights are achieved.

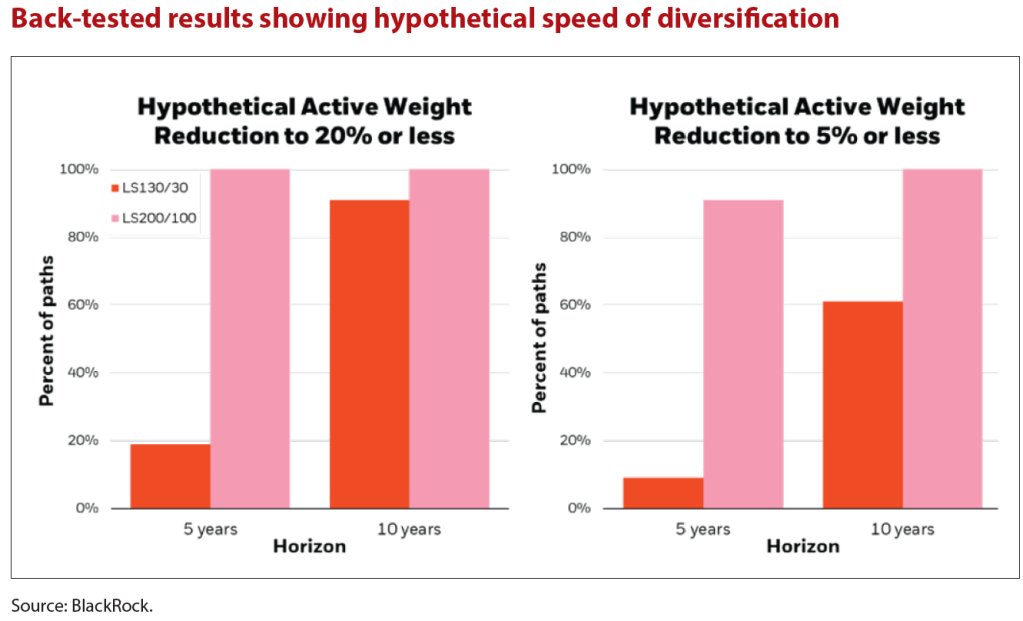

BlackRock researchers conducted an empirical study involving back-testing of hypothetical concentrated portfolios to examine the potential speed of diversification for the LS130/30 and LS200/100. The study involved running these strategies over 380 hypothetical, 10-year scenarios beginning Dec. 31, 1995, and ending Dec. 31, 2023, with different stocks and historical time periods. The study provided a broad view of the portfolios’ possible diversification speeds. The researchers measured the success of these strategies using active weight, which is the difference between the weights of a concentrated position in a portfolio and in a benchmark. Long/short diversification strategies reduce the active weight of a concentrated position until it is acceptably close to zero. For the more rapidly diversifying LS200/100 strategy, the concentration of any single stock was reduced to 5% of portfolio weight by the fifth year in 346 out of the 380 (91%) scenarios analyzed. Higher leverage led to a more reliable reduction in active weight. (See the table “Back-Tested Results Showing Hypothetical Speed of Diversification,” below.)

While the speed of diversification is an important factor for investors seeking to reduce the risk of concentrated holdings, it is not the sole consideration. Tax and financial professionals may evaluate additional elements when developing strategies to mitigate downside risk for their clients.

CHOOSING A CONCENTRATED STOCK RISK-MITIGATION STRATEGY

Selecting an appropriate concentrated portfolio management strategy requires a thorough evaluation of the investor’s profile. (See the table “Client Profile,” below, for a taxonomy of some factors that a tax or financial professional may take account of on their clients’ behalf.)

The relative importance and prioritization of these factors may vary by investor, so incorporating an investor’s goals, profile, and preferences is critical when formulating a de-risking strategy.

Consider, for example, a hypothetical investor who is concerned that an appreciated Apple stock holding may underperform the broader market. This position accounts for three-quarters of their net worth, leading the investor to prioritize capital preservation and avoidance of capital gains tax. An adviser might evaluate potential solutions such as participation in an exchange fund, establishing a CRUT, or investing in a long/short tax-managed strategy.

Upon discovering that the only exchange fund willing to accept Apple stock would not provide as much diversification as the other potential solutions, the investor narrows the decision to a CRUT — which immediately addresses downside risk — or a rapidly diversifying long/short tax-managed strategy. Their tax and financial advisers outline the respective advantages and disadvantages of these approaches.

A second investor is a sophisticated financial professional who anticipates the possibility of growth in their stock relative to the market. A slowly diversifying loss-harvesting strategy and a collar on half the position are both appealing. To finalize the decision, the investor asks their adviser about the collar’s tax implications and how to calibrate the loss-harvesting strategy so that the weight of the concentrated position is expected to be cut in half in five years.

Sometimes, a combination of strategies may enhance the overall outcome. For example, a CRUT can be a powerful solution on its own, but in some situations, it may be beneficially paired with an external loss-harvesting strategy. The latter may offset capital gains distributed by the CRUT and extend its tax-deferral horizon.

Each downside risk-mitigation strategy has benefits and drawbacks, rendering it powerful in some circumstances and less than ideal in others. Tax and financial professionals can frequently assist by modeling different scenarios and assumptions when trying to decide which strategy or strategies to use.

As always, an investor’s profile is an essential driver of the strategy choice. As tax and financial planning professionals’ ability to customize strategies that reduce downside risk expands, the maxim “know your client” becomes more important than ever.

About the authors

Lincoln Fleming, CPA/PFS, CFP, is a director and after-tax wealth strategist with BlackRock, a New York City-based multinational investment company. Lisa Goldberg is a managing director and senior advisor at SMA Solutions with BlackRock and professor of the practice of economics at the University of California at Berkeley. To comment on this article or to suggest an idea for another article, contact Jeff Drew at

Jeff.Drew@aicpa-cima.com.

LEARNING RESOURCES

Old Problems, New Solutions: Techniques for Solving Concentrated Stock Positions

Explore the challenges, complexities, and client behaviors related to concentrated stock positions. Review historical stock performance for insights and examine tax-efficient mitigation strategies. (This resource is exclusive to PFP Section members.)

WEBCAST (archived, no CPE)

This eight-course program covers steps in the investment planning life cycle, including a discussion of planning for and funding higher education.

CPE SELF-STUDY

Investment Planning Certificate

The Investment Planning Certificate Program bundle includes the Investment Planning online CPE learning and the Investment Planning Exam.

CPE SELF-STUDY

Advanced personal financial planning is one of the tracks you can follow as the biggest event in the accounting profession celebrates its 10th anniversary at the ARIA in Las Vegas. Don’t miss it!

June 8–11

CONFERENCE

The Personal Financial Planning (PFP) Section is an add-on membership section within the AICPA that provides an unparalleled package of resources designed specifically to support and promote CPA financial planners and their client relationships. For more information, click on the PFP Section membership headline above.

SECTION

For more information or to make a purchase, go to aicpa-cima.com/cpe-learning or call 888-777-7077.

MEMBER RESOURCES

Article

“How OBBBA Alters Charitable Deduction Strategies for 2025 and 2026,” JofA/PFP Digest, Oct. 31, 2025

Podcast episode

“JofA Branded Podcast: Investment Management at the Intersection of Tax and Wealth Services,” JofA, Dec. 2, 2025

Website