- feature

- PRACTICE MANAGEMENT

Tackling the top issues

Growth returns to forefront as firms try different strategies to handle concerns.

Please note: This item is from our archives and was published in 2013. It is provided for historical reference. The content may be out of date and links may no longer function.

Related

ENGAGE takeaways: 7 principles to improve CPA firm profitability

What it takes for a CFO to lead operations and tech

Rise2040: A human-led profession built on trust

For many, if not most, accounting firms, the quest to survive the Great Recession and its aftermath has ended. The focus now is on growth.

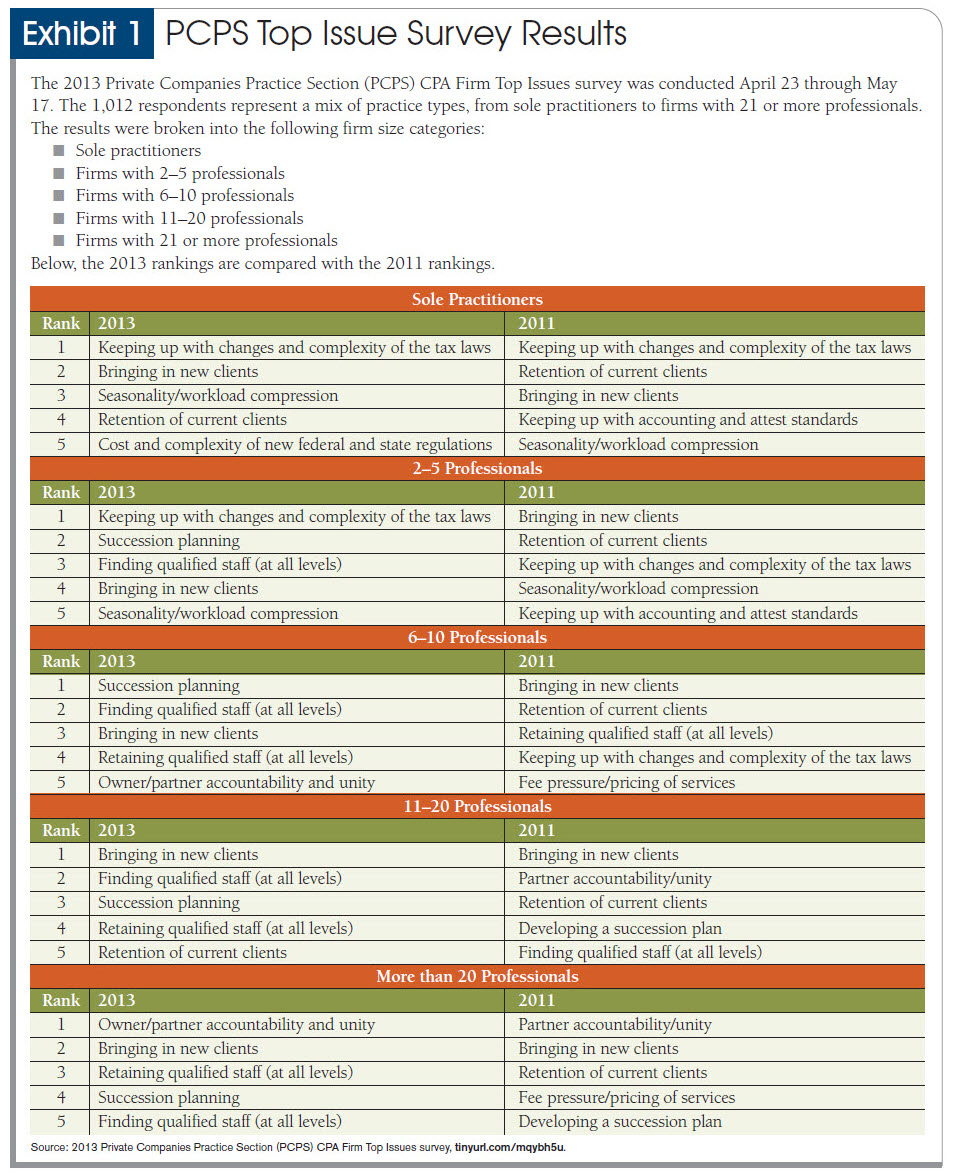

That’s one of the overarching themes derived from the 2013 Private Companies Practice Section (PCPS) CPA Firm Top Issues survey, which found that accounting firms of all sizes are strongly pursuing new clients while also turning their attention back to finding and retaining qualified staff.

From 1997 through 2007, staff recruitment and retention topped the list of issues for almost all firm sizes tracked by the biennial PCPS Top Issues survey. That changed with the 2009 poll, which found firms focused on trying to retain clients amid the Great Recession. The scene shifted a bit with the 2011 survey, when the search for new clients emerged as a major priority along with client retention. This year, however, client retention ranked among the top five issues in only two of the five size categories (see Exhibit 1).

{kind=link}

“When the economy was in free fall, firm leaders largely focused on stabilizing their client base,” said Mark Koziel, CPA, CGMA, the AICPA’s vice president–Firm Services & Global Alliances. “Now we’re seeing firms being able to catch their breath and engage in more planning for future growth.”

Bringing in new clients was the only issue to rank among the top five in all five size categories. Finding qualified staff and succession planning ranked among the top five in four of the five categories.

The increased emphasis on attracting and keeping quality staff indicates that accounting firms are growing and that competition for talent is heating up. A surge in the number of accounting graduates should help in this area (see “Supply and Demand for Accounting Talent at Record Levels,” page 30), as could increased emphasis on promoting women CPAs (see “Women’s Initiatives: A Strategic Advantage,” page 34). The growing focus on succession planning, which appeared among the top five issues in only the two largest size categories in 2011, indicates that more firms realize that the inevitable transfer of ownership from Baby Boomer partners will become a reality (see “How to Select a Successor,” page 40).

The list of top five issues for each firm-size category can be found in Exhibit 1.

TOP ISSUES: SUCCESS STRATEGIES

How are CPAs and their firms dealing with the top issues? What strategies and initiatives have proved successful? Following is a look at how some firms are handling three of the top issues identified by the PCPS survey: client acquisition, partner accountability, and workload compression.

Bringing in New Clients

Green Hasson Janks is a 12-partner, 100-employee firm based in Los Angeles. HBE Becker Meyer Love is a six-partner, 40-employee firm in Lincoln, Neb. At first glance, the two firms appear to have about as much in common as Hollywood and the heartland. But a closer look reveals a similar approach to gaining new clients.

Green Hasson Janks and HBE Becker Meyer Love have both built their practices on core niches and have built their books of business through focused marketing efforts. Both firms have partners or staff dedicated to marketing, and both firms count services for not-for-profit entities among their core niche offerings.

At Green Hasson Janks, Kari Schott has been director of marketing for 3½ years. During that time, the firm has built a concentration in three niches—entertainment, not-for-profit, and food and beverage. The firm also has implemented an emphasis on business and referral development that starts with the partners.

Managing partner Leon Janks has empowered Schott to be the driving force behind the program, though she is not a CPA and has a marketing, not accounting, background. Schott plays a key role in helping the partners develop annual business development plans. She then acts as a coach, meeting with each partner quarterly to help assess how each plan is progressing and what steps should be taken to move the plan forward.

“We talk about prospective referral sources, what type of content they want to develop over the course of the year,” Schott said. “The plan is a living document.”

Janks wants his partners and staff to live and breathe business development in everything they do. The firm has set up an incentive program for staff in which staff members are rewarded for bringing in new business. One point of emphasis is cross-selling. If a tax partner or staff CPA can bring in an audit client, it helps the firm as a whole.

The firm emphasizes the importance of partners getting out into the field to meet with prospective clients. Partners recently ventured outside their primary service area of Southern California to attend a food conference in Chicago, where they contacted potential clients and began building relationships that have resulted in opportunities to bid for business locally. “We would not have traveled outside of our market two years ago,” Janks said. “But it’s clear to me that we need to create relationships in a nonselling environment.”

The approach paid off. The firm has generated a 50% increase in bids for business over the past two years, Schott said.

Halfway across the country from Los Angeles, HBE Becker Meyer Love also has built business by beefing up its marketing efforts. The firm has a partner in charge of business development and also hired a marketing coordinator. Marketing pipeline meetings are held, with an emphasis on building relationships and generating referrals from other professionals, particularly attorneys. The approach has helped grow the firm’s three main niches—not-for-profits, construction, and manufacturing—as well as the firm’s developing business lines including doctors’ and dentists’ offices and business process outsourcing.

“We encourage our staff to be involved with not-for-profits, and we use some of that in our marketing material,” said Lanelle Herink, CPA, the firm’s business development partner. “We list everything they do. It shows our commitment to the firm.”

Serving on the boards of not-for-profit organizations also improves staff and partner skills, said managing partner Scott Becker, CPA. Experience dealing with nonprofit issues in a management capacity makes CPAs better at auditing nonprofits as part of their day job, Becker said.

Partners and staff are organized into niche teams within the firm, and there is an emphasis on involving staff in business development. Partners list all client visits on a calendar accessible by all partners and staff. CPAs at the staff level who want to join a partner on a client visit can simply sign up through the calendar, subject to partner approval. That allows staff to pursue areas of interest and helps with staff retention by getting them involved in face-to-face business development and current client meetings.

“We’re good at our partners’ transitioning clients down to staff,” Herink said. “It’s a good mix.”

Owner/Partner Accountability and Unity

A dozen years ago, Seattle-based Peterson Sullivan was at a crossroads. The firm was successful but limited by its governance structure. There was no managing partner and no executive committee. The firm’s five partners each had a vote on all partnership matters including partner compensation. It was a viable system, but one stretched to its full capacity. To grow, the firm needed to make some changes.

Four years ago, Arizona-based Henry & Horne was not so much one firm as it was three. The practice’s Scottsdale, Tempe, and Casa Grande offices operated as separate profit centers. Each office had its own managing partner and kept the profits it generated. Individual partner compensation was determined by a complicated formula. The firm was an $18 million giant, but one in need of an awakening.

Peterson Sullivan and Henry & Horne took similar paths to move to a higher level of growth and success. Both firms addressed two of the key factors in partner accountability and unity—the firm’s governance structure and partner compensation.

At Peterson Sullivan, the firm formed an executive committee while growing from five partners to eight partners, said Chris Russell, CPA, managing partner and executive committee member. Firm leadership recognized a need to base partnership compensation on factors beyond what was assessed on a spreadsheet. Over time, the executive committee determined partner compensation and then formed a compensation committee to handle the task. The firm then set up and evolved the governance structure in use today. Partners meet with the partner in charge of their department and in a collaborative process agree to specific goals. The goals vary from partner to partner, based on individual expertise and skills. Partners meet with their department head for a midyear meeting to assess progress, then in a review meeting at the end of the year. The firm’s compensation committee bases partner pay on the information gathered at the meeting and on the partner’s performance during the year.

The changes have paid off. The firm over the past 12 years has more than tripled in size, to 17 partners and about $25 million in annual fees. A key to the firm’s growth has been the steady evolution of the compensation and governance structure and, most importantly, of partner buy-in to that structure, Russell said.

“It wasn’t an overnight thing,” Russell said. “Every year, we fine-tune it.”

Peterson Sullivan encourages partners to make “stretch” goals that align with the firm’s overall strategic plan. “It’s not necessarily about whether you attain the goal,” Russell said. “It’s about how much progress you’ve made.”

Henry & Horne began progressing from a loose collection of three offices to one firm by eliminating the managing partner position at the individual offices and naming Chuck Inderieden, CPA, and Chuck Goodmiller, CPA, as co-managing partners for the entire firm. Henry & Horne ripped down the walls separating the firm’s three offices. “We don’t even track what Scottsdale does vs. Tempe and Casa Grande,” Inderieden said.

In addition, Henry & Horne moved away from partner compensation based on a formula to a governance system in which the managing partners work with a compensation committee to determine partner pay. In a system similar to Peterson Sullivan’s, Henry & Horne partners co-create their goals with management and work to align those goals with the firm’s overall strategy.

“Our approach is not that every partner should be the same,” Goodmiller said. “One partner may be highly talented with business development but not as technically strong. When we do have complementary talents, we should use them.”

How do Peterson Sullivan and Henry & Horne persuade their partner groups to go along with their accountability and governance systems? Leaders at both firms emphasize the importance of building trust with the partners—a process that takes time and consistency. Peterson Sullivan’s system provides explanations to partners on compensation decisions. Henry & Horne emphasizes the importance of dealing with difficult situations early, before they grow bigger.

“It’s much easier to fix something when it starts,” said Goodmiller, whose firm has grown from an $18 million operation four years ago to a $21 million practice today.

Tax Law Complexity

As a sole practitioner, Casey Lynch, CPA, understands the struggle of trying to keep pace with continually changing and complex tax laws. The problem is perspective and a lack of personal and professional interaction. “We have so much information, but there’s a difference between information and knowledge,” said Lynch, the Durango, Colo.-based owner of Casey D. Lynch CPA LLC.

At larger firms, CPAs can discuss the implications and applications of tax laws with one another. That’s not possible for sole practitioners, but Lynch has found an able substitute through the social media website LinkedIn. He is an active participant in a number of LinkedIn groups organized through the AICPA.

“You have access to so many CPAs,” Lynch said. “I like the AICPA group because I have a certain level of expectation of the participants.”

Lynch also likes the fact that there are groups dedicated to specific topics. To wit: If he has a tax question, he can post it in the Tax Practitioners group, which has a wider array of CPAs than the Sole Practitioners group. Or if he has a question about work flow, he might take that question to a group discussing work flow issues.

The ability to interact with fellow CPAs in a number of different areas helps Lynch deal with tax laws that continue to become more complicated. “It’s been an amazing help to my practice,” he said.

Seasonality/Workload Compression

Tabitha Jones, CPA/PFS, is a tax manager with Daniel C. Henning & Associates, a two-partner, 10-employee firm in Sandy Springs, Ga., a suburb north of Atlanta. Her firm works exclusively on tax issues. There is no audit work. The bulk of the firm’s work comes during the busy season, and the firm employs a combination of strategies to mitigate the impact of seasonality and workload compression.

“One of our biggest focuses is training,” Jones said. “We spend the whole month of January training to make sure everyone is proficient in the use of the software.”

Daniel C. Henning & Associates hired third-party CPE providers to put employees—from administrative staff to partners—through 20 hours of training each week in January. The training aims to make sure everyone is on the same page on how to use the software and how to handle a variety of situations. The training has two areas of focus. Technical training addresses new tax laws, updates to laws, etc. The second component covers the software training and all of the firm’s procedures for handling tax work. The month of preparation culminates with a full-day tax season meeting.

The training program has been in place for five years, said Jones, who has seen a “really huge improvement” with efficiencies. “The stress level is much better, just knowing what to expect, not having as many surprises,” she said. “A lot of the training process is about leveraging technology. Now, everyone has a clearly defined direction with everything they touch.”

Jones’s firm uses project management software to track each project by deadline and person working on each task. The firm organizes its efforts during the height of tax season by holding daily work-in-progress meetings at 7 a.m. These triage sessions, as Jones calls them, help the firm make the most of its 11-hour shifts during the height of the tax crunch.

Daniel C. Henning & Associates’s training and triage approach has helped the firm better handle the time pressures of busy season, Jones said. This year was the most difficult tax season Jones has experienced because of the late changes made by Congress, but the firm’s employees averaged no more than 65 hours a week during the height of the tax rush, from March 1 through April 15, she said. That compares with an average of 70 hours per week before the training program began five years ago.

“With the training in place, we have a much smoother tax season,” she said.

EXECUTIVE SUMMARY

Growth-related concerns are top of mind for accounting firms surveyed in the 2013 Private Companies Practice Section (PCPS) CPA Firm Top Issues survey. Adding new clients was the only issue listed among the top five for each of the five size categories.

Firms have turned their attention back to attracting and retaining qualified staff. This indicates that the competition for talent is heating up.

Succession planning ranked among the top issues for all but the smallest firms. Firms recognize the need to prepare for the future.

Other top concerns include partner accountability, the complexity of tax laws, and the compression of workload during tax season.

Marketing personnel and niche services play key roles in firms’ business development efforts.

Firms seeking partner accountability have found success with compensation committees, shared goal setting between managers and partners, and regular meetings to gauge progress.

Extensive training on processes and technology can help improve efficiency and ease the workload burden during busy season.

Jeff Drew is a JofA senior editor. To comment on this article or to suggest an idea for another article, contact him at jdrew@aicpa.org or 919-402-4056.

AICPA RESOURCES

JofA articles

- “Supply and Demand for Accounting Talent at Record Levels,” Sept. 2013, page 30

- “Women’s Initiatives: A Strategic Advantage,” Sept. 2013, page 34

- “How to Select a Successor,” Sept. 2013, page 40

- “The Long Goodbye,” Aug. 2013, page 36

- “Mergers Emerge as Dominant Trend,” July 2013, page 52

Conference

Practitioners Symposium and Tech+ Conference, June 9–11, Las Vegas

For more information or to make a purchase or register, go to cpa2biz.com or call the Institute at 888-777-7077.

Website

The PCPS Top Issues Survey commentary

Private Companies Practice Section and Succession Planning Resource Center

The Private Companies Practice Section (PCPS) is a voluntary firm membership section for CPAs that provides member firms with targeted practice management tools and resources, including the Succession Planning Resource Center, as well as a strong, collective voice within the CPA profession. Visit the PCPS Firm Practice Center at aicpa.org/PCPS and the Succession Planning Resource Center at tinyurl.com/oak3l4e.