- feature

- PROFESSIONAL ISSUES

Global mobility: U.S. CPA credentials travel around the world

Please note: This item is from our archives and was published in 2013. It is provided for historical reference. The content may be out of date and links may no longer function.

Related

No Results

TOPICS

-

Uncategorized Article

Within the continental United States, CPAs are fairly mobile. No matter in which state they are based, they are generally able to temporarily practice across state lines without obtaining a reciprocal license if they have 150 hours of education, passed the CPA exam, and have at least one year of experience. The only remaining U.S. jurisdictions without an individual CPA mobility law are Hawaii, Guam, Puerto Rico, the Virgin Islands, and the Northern Mariana Islands. The rules for foreign countries are different, but U.S. CPAs interested in working abroad will find six nations open and hassle-free.

For U.S. CPAs, global mobility is largely determined by mutual recognition agreements (MRAs). MRAs are contracts between professional accounting organizations from countries that have signed the General Agreement on Trade in Services, a World Trade Organization treaty that took effect in 1995. To better understand why global mobility is gaining in importance and what MRAs can do for CPAs, the JofA talked to Jim Knafo, AICPA director–International Relations. From 1999 until 2012, Knafo helped negotiate existing U.S. MRAs as a volunteer member of the International Qualifications Appraisal Board (IQAB). The U.S. IQAB, whose members are appointed by the National Association of State Boards of Accountancy (NASBA) and the AICPA, reviews accounting qualifications in other countries, negotiates MRAs with foreign professional accounting organizations, and makes reciprocity recommendations to the AICPA, NASBA, and state boards of accountancy. The following are excerpts from the conversation with Knafo:

Why would U.S. CPAs explore licensure elsewhere?

Knafo: Global mobility is important for two reasons. The first is that the world is becoming a much smaller place, and our clients, even small ones, are turning to international markets more and more. We need global mobility in much the same way that we need interstate mobility: to continue to serve and grow with our clients. Similarly, more companies want to do business in the U.S. What better way to break the ice with a potential new client than to start the conversation by mentioning that you have an accounting designation from their home country? Right away, that gives you an edge over the next accountant who is pursuing the client.

The second reason is more personal. Global mobility gives you the opportunity to live and work abroad for a few years, broaden your professional expertise, and gain new perspectives without having to put your career progression on hold.

What does an MRA do for a CPA, and which countries have MRAs with the United States?

Knafo: The MRAs negotiated by the IQAB allow U.S. CPAs to access licensure in foreign countries through an accelerated route. An MRA is essentially a shortcut. It allows professionals who have already been tested and certified in their home country to move to another country without having to start over. They don’t have to meet additional education requirements or take other countries’ equivalent of the U.S. Uniform CPA Exam. The MRA allows professionals to have their existing credential, and all that went into earning it, recognized. Generally, the sole requirement to obtain the foreign license is to pass a short exam on local laws, tax, and regulations.

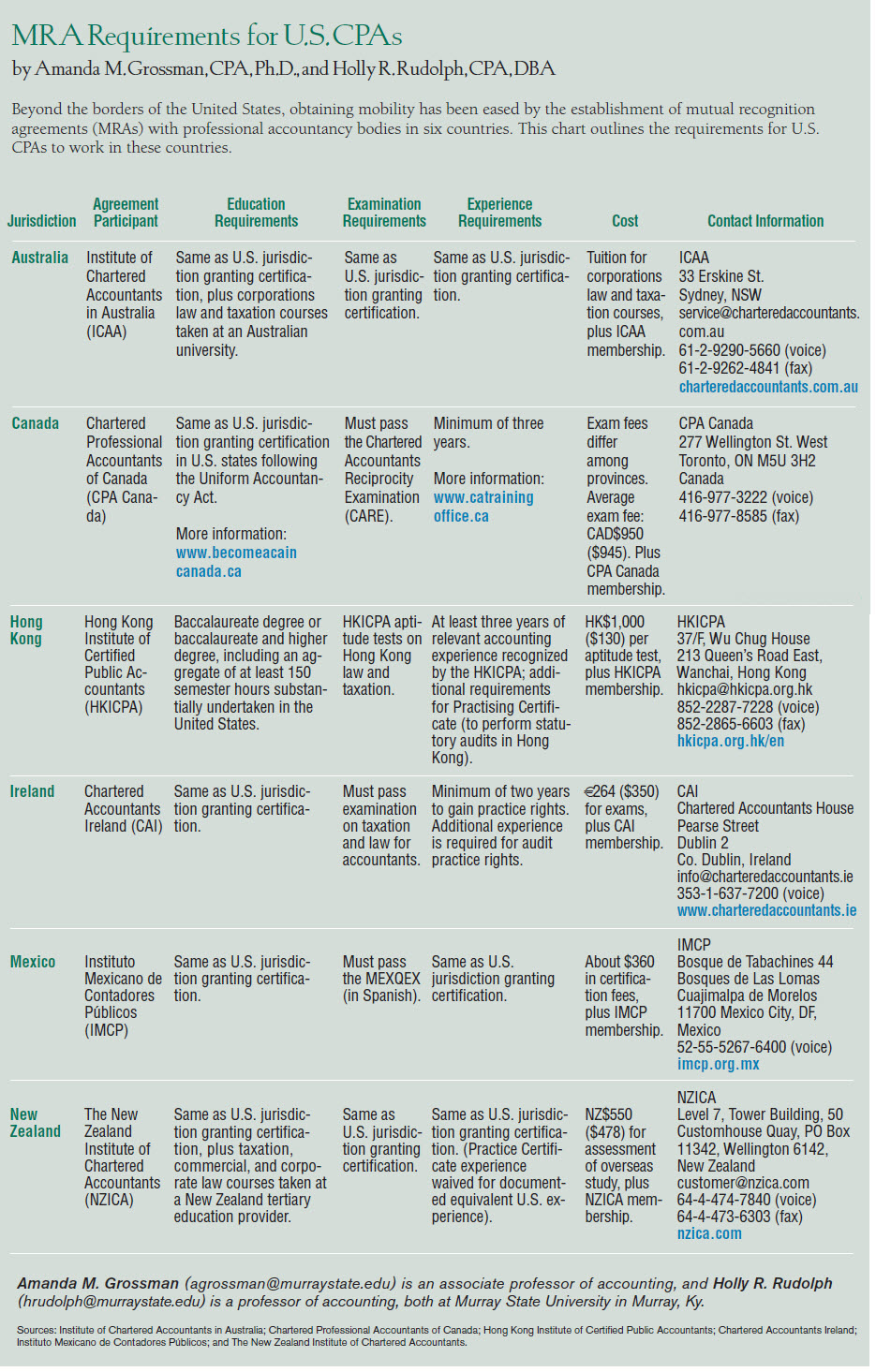

The National Association of State Boards of Accountancy and the AICPA currently have MRAs with professional accounting organizations, or PAOs, in Canada, Mexico, Australia, New Zealand, Ireland, and Hong Kong (see “MRA Requirements for U.S. CPAs”). With an MRA, individual U.S. CPAs do not have to be evaluated on a case-by-case basis, because, in essence, the U.S. CPA certification process has already been prescreened by the foreign PAO.

{kind=link}

What options do U.S. CPAs have in countries that do not have MRAs with the United States?

Knafo: In some non-MRA countries, a U.S. CPA seeking licensure may get lucky, because due to the outstanding reputation of the U.S. CPA certification and the AICPA around the world, some foreign PAOs may recognize and give credit for the CPA’s U.S. education and/or experience.

But usually U.S. CPAs will have to meet the same qualification requirements as local candidates without the MRA shortcut. This may mean additional education, local experience, or one or more examinations. Some countries even require residency or citizenship. To find out more, I suggest that U.S. CPAs interested in working in a non-MRA country visit the website of and contact the country’s PAO.

Do U.S. CPAs who are licensed elsewhere have a competitive advantage?

Knafo: Think of this question from the opposite perspective. If a foreign accountant came to the U.S., would she have an advantage if she became a U.S. CPA? Of course. Without a U.S. CPA would she be able to practice in the U.S.? Would her chances of getting a job improve if she obtained her U.S. CPA?

The same rationale holds true for a U.S. CPA who moves abroad, wants to attract foreign clients, or wants to retain clients who are expanding internationally.

Editor’s note: Click here to read “MRA Requirements for U.S. CPAs,” by Amanda M. Grossman, CPA, Ph.D., and Holly R. Rudolph, CPA, DBA. The chart is a quick guide to the requirements for U.S. CPAs to work in the six countries in which the United States has mutual recognition agreements.

Sabine Vollmer is a JofA senior editor. To comment on this article or to suggest an idea for another article, contact her at svollmer@aicpa.org or 919-402-2304.

AICPA RESOURCES

JofA articles

- “How to Do Business in India,” March 2013, page 26

- “Business Basics in Brazil,” Nov. 2011, page 34

- “Business Basics in China,” May 2011, page 42

Publication

U.S. Taxation of International Operations: Key Knowledge (#091102, paperback; and #091103PDF, on-demand online access)

CPE self-study

- International Taxation: To and From the United States (#731898)

- International Versus U.S. Accounting: What in the World Is the Difference? (#745941)

- IFRS Certificate Program (#159770)

Conference

Doing Business in Brazil, July 18–19, Orlando

For more information or to make a purchase or register, go to cpa2biz.com or call the Institute at 888-777-7077.