- feature

- MANAGEMENT ACCOUNTING

A strategic approach to IT budgeting

How organizations can align technology spending with their overall mission and goals

Please note: This item is from our archives and was published in 2012. It is provided for historical reference. The content may be out of date and links may no longer function.

Related

A new top 5 firm: Grant Thornton acquiring fellow top 10 firm CBIZ

As AI use in cybersecurity rises, so do the risks

Are finance leaders moving too fast on agentic AI?

Organizations of all types struggle with information technology (IT) budgeting. This often happens because the IT team doesn’t understand the budgeting process and the finance team doesn’t understand IT. CPAs, whether in public practice, business and industry, the not-for-profit sector or government, can remedy this disconnect by changing their organization’s approach to IT budgeting from merely an annual “make it fit” exercise into a meaningful planning and ongoing management process.

This shift requires more than just throwing numbers onto a spreadsheet. It demands that an organization’s leaders work together to define IT’s role in achieving the organization’s objectives—transforming IT from a cost center into an investment.

GOOD IT BUDGETING IS LIKE GOOD FINANCIAL PLANNING

If you look at IT spending as an investment in your organization’s future, you may see that effective IT budgeting has much in common with personal financial planning. To give appropriate savings and investment guidance, personal financial planners first must understand their clients’ short- and long-term goals. The same holds true for CPAs working on an IT budget. Only after gaining an understanding of the organization’s short- and long-term goals can CPAs help ensure that the organization is aligning its IT strategy with its business strategy, resulting in the right IT investment decisions.

Personal financial planners must consider each client’s short- and long-term constraints—for example, is the client’s ability to save or invest limited by current earnings, deduction limitations or even current life-stage expenses (for example, school costs for children)? A similar concern with constraints applies to IT budgeting. What is the organization’s cash flow? How will IT spending impact the organization’s overall capital and operating budgets? Are any major projects occurring that might impact the IT infrastructure? Remember to consider both the financial and nonfinancial implications of IT-related initiatives.

Good financial planning considers the human element of each client’s life. What is the client’s current lifestyle, and what is the client’s expected lifestyle upon retirement? Is the client willing to make changes in his or her current lifestyle to provide for a different lifestyle upon retirement?

The human element also is one of the key, and most often overlooked, aspects of IT initiatives. Is the organization making other changes that might impact its employees’ ability to absorb a new computer system or other IT investment? How would an IT initiative affect employees’ work lives?

Good personal financial planners help clients look at various investment options and savings strategies to determine what makes the most sense based on each client’s life stage, risk tolerance and savings ability. Financial planners discuss multiple investment and savings scenarios with clients to determine what best meets their short- and long-term needs. From this process comes the final financial plan.

CPAs should develop their organization’s IT budget in much the same way. They should use multiple versions of the IT budget to analyze technology options and their associated financing strategies. They should look at each IT initiative as an investment option, the timing and execution of which affects the overall IT budget. They should consider different timing or initiative phasing to identify how different execution scenarios might impact the organization’s IT budget and cash flow.

ALIGNING THE IT BUDGET WITH THE ORGANIZATION’S STRATEGY

Once a client’s individual investment and savings options have been selected, good financial planners look at the plan as a whole to determine whether it will achieve the client’s financial goals. The IT budget works the same way. Once IT initiatives have been evaluated and incorporated into the budget, organizations should take a step back from the details and look at the big picture.

Each organization should answer the following questions: Do the selected IT initiatives align with and support the organization’s strategic objectives? Should any initiatives that weren’t selected for the budget be reconsidered? Would any of the organization’s strategic initiatives make one of the selected IT initiatives obsolete?

The next step is to validate IT’s role in the organization. The IT budget often is treated as just one big mass (see sidebar “IT Budgets: Expenditure Types and Categories,” near bottom of page). However, it really has three distinct components. Information technology research firm Gartner refers to these components as Run, Grow and Transform.

1. Run budget items keep the organization operating. Examples of Run budget items include mission-critical server replacements, key software upgrades and personnel costs associated with administering and maintaining the IT infrastructure on a day-to-day basis.

Organizations that have to trim IT budgets should avoid cutting Run initiatives. Such cuts would introduce operational risk. If an organization already is going through a tough stretch, the last thing it needs is a server, application or network failure.

2. Grow budget items help the organization introduce new capabilities or improve existing ones. Grow initiatives could include the implementation of new software that makes operations more efficient, the purchase of a new firewall that provides additional protection from cyber threats or an upgrade of the organization’s website that improves interactivity with customers.

Grow budget items should tie directly to the organization’s strategic initiatives. Grow initiatives usually are not as mission critical as Run initiatives and often have some time flexibility, which means that they are good candidates for starting early when additional cash is available, or for deferral if cash is tight.

3. Transform budget items are research- and-development-type activities. These initiatives might seek to identify, for example, the right technologies for new organizational capabilities; fundamental changes to business processes; or a new product or service offering. Examples of Transform initiatives include proof of concepts, prototypes and small-scale testing of new systems or business applications.

When finances are tight, transform initiatives often are the first to be cut or deferred—unless they are associated with key strategic initiatives that the organization views as essential to its continued operation. Even if the organization doesn’t deem certain Transform initiatives immediately essential, care should be taken when considering cutting or deferring them. That’s because Transform initiatives often are key to the organization’s long-term health. Failure to provide adequate resources to Transform initiatives can stunt an organization’s future success. By looking at the percentages of the Run, Grow and Transform components of an IT budget, CPAs can analyze the role that IT plays in the organization (see sidebar “Run-Grow-Transform IT Investment Analysis”). A Run-Grow-Transform analysis can determine whether the IT budget properly reflects IT’s designated role in achieving the organization’s mission. Additionally, by classifying initiatives into each of these categories, CPAs can help guide adjustments to the timing of IT spending in response to changes in the organization’s cash position throughout the year.

Run-Grow-Transform IT Investment Analysis

By analyzing the Run-Grow-Transform components of an organization’s IT budget, CPAs can help to ensure a balanced IT investment. Just as a diversified financial portfolio is good for long-term financial health, a diversified IT budget portfolio is important for ensuring the long-term viability of an organization.

In Exhibit 1, Entity A (a late technology adopter) is an organization where IT does not play a critical role. About 80% of the IT budget is used for “keeping the lights on,” and only 20% is spent helping to grow the organization. Conversely, Entity B (mainstream adopter) and Entity C (early adopter) spend only 50% to 60% of their IT budget on Run items and devote a hefty 30% to growing their IT capabilities. The key difference between these two organizations is that Entity C devotes twice as much of its IT spending to Transform initiatives as Entity B does. While this might not seem like much, spending more than your competition to figure out how to leverage technology can provide a huge competitive advantage.

How important is IT to your organization? If it is critical or very important, your IT spending analysis should look like those of Entity B or C. Be wary if your breakdown looks like Entity A’s. In today’s world, if your organization isn’t transforming and keeping current with technology, you might be left in the proverbial silicon dust.

ASSESSING THE FINANCIAL IMPACTS OF THE IT BUDGET

CPAs also can help determine whether the IT budget makes financial sense. In making that determination, the following considerations are key: (1) impact on financial key performance indicators (KPIs); (2) impact on financial statements; and (3) impact on cash flow. Because IT budgets often have large capital- and operating-expenditure components, the final IT budget needs to be incorporated into the organization’s overall budget to determine whether the timing or financing options for IT initiatives could have any unintended consequences.

Each organization uses different financial KPIs to gauge its performance. Loan covenants, leasing agreements, contracts and grants, and other arrangements also may have certain financial requirements or metrics that should be considered when developing the IT budget. Sometimes, adjustments to the timing of initiatives or different financing arrangements for the initiatives can help to ensure that an organization meets both its compliance requirements and internal KPI measurements.

Finally, and most importantly for smaller organizations and not-for-profits, CPAs must consider the impact on cash flow. IT initiatives often have large upfront expenditures for purchase and implementation. Organizations can manage the impact of these initiatives on their cash flow by, again, adjusting the timing of the initiatives (or purchases within the initiative) or by obtaining different financing arrangements.

One way to manage cash flow is to use a reserve approach to IT budgeting. Similar to the way reserve requirements are computed for a homeowners’ association, an organization can plan to set aside cash each year to ensure that it has the funds necessary to execute future IT initiatives. This process also helps reduce the risk that an unexpected technology failure and early replacement would have a negative impact on the organization’s cash flow.

Again, a long-term outlook is advisable. CPAs should assess the IT budget’s financial impact not only for the current or upcoming year, but also for future periods that IT initiatives might affect. Too often, organizations “balance the budget” for the current year, only to run into unintended consequences in a future period. Remember, a good IT budget balances both short-term and long-term financial implications. The sidebar “A Multiyear Run-Grow-Transform and Reserve Analysis” illustrates how reserve budgeting works.

A Multiyear Run-Grow-Transform and Reserve Analysis

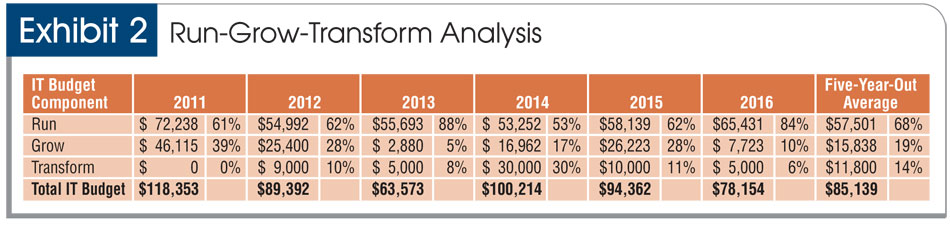

Exhibit 2 shows how a small organization may have different Run-Grow-Transform profiles as it goes through different stages in its development.

{kind=link}

In 2011, the organization “modernized” its IT infrastructure, spending a substantial amount to replace and update its servers and workstations. Over the next two years, it plans to scale back its IT spending to build up reserves for major upgrades in 2014 and 2015. In 2016, the organization plans to start building reserves for the next major upgrade/replacement cycle.

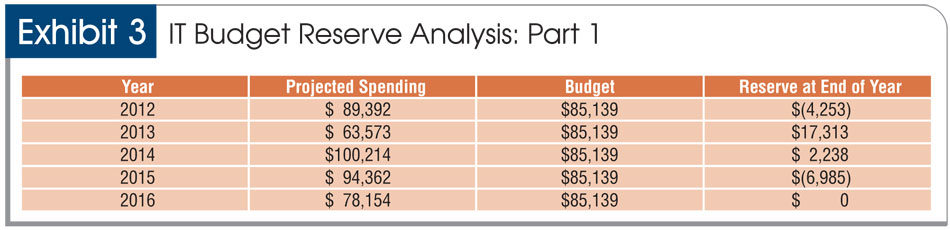

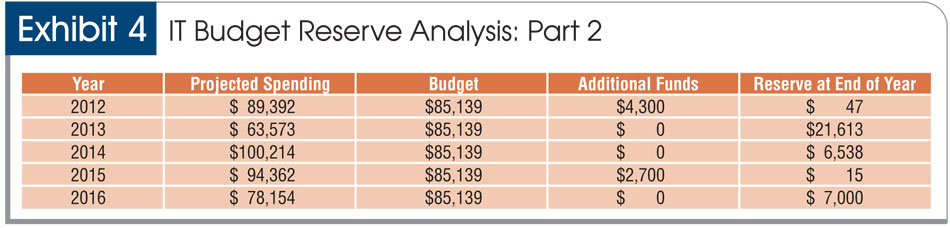

The same small organization can use a reserve analysis to smooth out the impact of IT spending on its budget and manage cash flow. The average annual spending ($85,139) identified in Exhibit 2 is used as the IT budget amount for 2012–2016. This results in reserve-amount deficiencies in 2012 and 2015, as shown in Exhibit 3. That means the organization must plan to supplement its IT budget with about $4,300 in 2012 and $2,700 in 2015 to balance its budget and spending, as shown in Exhibit 4.

{kind=link}

{kind=link}

Once the additional funding amounts are plugged in, the projected IT spending is fully covered for the out-years with only minimal additional contributions of cash. Such contributions often are much easier to manage than large fluctuations in cash, especially for small businesses and not-for-profits. When the projected spending is less than the budgeted amount, the difference for that year goes into a “reserve” that accumulates over time to balance out cash needs in years with significantly larger projected spending. The organization can plan to “hold back” in years prior to large spending years to accumulate more cash reserves, as seen in Exhibit 4 when 2013 is compared with 2014 and 2015. Please note that this reserve analysis is purely a budgeting and cash management technique and is not valid for financial statement purposes.

CONCLUSION

When CPAs employ a strategic approach for IT budgeting, they create a planning and decision-making tool that can help maximize the benefits of IT investments. A good IT budget not only gives the organization the ability to manage its IT costs in both the short and long term, but it also provides the agility needed to adjust IT spending in response to changes in the business environment. In the final analysis, a good IT budget provides a competitive advantage because it helps organizations better execute in achieving their missions. CPAs should play a critical role in helping their organizations gain this competitive edge.

Click here to view a video clip of Donny Shimamoto, CPA/CITP, discussing the strategic approach to IT budgeting.

IT Budgets: Expenditure Types and Categories

Sometimes, IT budgets are treated as one big blob. To support better decision making and planning, the IT budget should identify expenditures by type and category.

In addition to the standard personnel and nonpersonnel expenditures associated with other functions, the IT budget should identify the following IT-specific expenditures:

- Hardware. This encompasses equipment and other fixed assets, installation costs, maintenance contracts, warranties, etc. This is any expenditure that results in ownership of a physical asset or is associated with the continued use and maintenance of such an asset.

- Software. This includes software licenses and support contracts, usually with a set price for a fixed term.

- Subscriptions. These could be associated with hardware, software, training, cloud computing and managed-service providers. Subscriptions can have a fixed or variable price and a fixed or variable term.

- Services. In this group are advisers, consultants, service providers, auditors and legal counsel. This item covers direct and indirect cost of services needed to support IT operations and initiatives.

IT budgets also should address the three main categories of IT spending:

- Capital. These expenditures need to be considered as part of the organization’s capital budget; usually, this means that the spending will need to be capitalized. These expenditures include purchases of hardware and large software licenses, significant repairs, parts replacements and major software upgrades.

- Operating. These expenditures are related to operations and usually include subscriptions, maintenance and support for hardware and software.

- Project. Usually, project expenditures are tied to a discrete effort. These may or may not need to be capitalized and may be required or discretionary. Project expenditures often are a flexible part of the IT budget; they usually can be accelerated or pushed back depending on cash flow or other events.

Identifying the categories of expenditures helps to break the IT budget blob into identifiable components that can be used to support organizational planning and cost management.

Not-For-Profits Face Grant Decision

Not-for-profit organizations have an additional variable to consider when looking at IT initiatives: grant opportunities.

Many grants fund one-time capital expenditures but not ongoing operational expenditures. Not-for-profit organizations also must consider funding sources and grant opportunities when structuring IT budgets to ensure that proper funding is provided for both the capital and operating portions of all projects.

Often, not-for-profits jump to take advantage of a grant opportunity but forget to assess the impact on their operational budget. CPAs working with a not-for-profit should insist that this step is taken to ensure that the not-for-profit can absorb the ongoing expenditures in its operations funding.

EXECUTIVE SUMMARY

Organizations of all types often struggle with IT budgeting because the finance team doesn’t understand IT and the IT team doesn’t understand budgeting. One way for both sides to better conceptualize the process is to look at IT spending as an investment in the organization’s future.

A good IT budgeting process has much in common with good personal financial planning. Both processes establish short- and long-term goals, take into account spending and other constraints, consider the “human” impact and analyze several strategies to determine the approach that aligns best with mission and risk tolerance.

While often viewed as one big mass, an IT budget comprises many components—such as capital, operating and project categories—and types of spending—such as hardware, software, subscriptions and services.

A good way to analyze the IT budget is to conduct a Run- Grow-Transform analysis. “Run” budget items “keep the lights on”; “Grow” spending aims to increase the organization’s IT proficiency; and “Transform” projects refer to R&D-type projects such as proof of concepts or prototypes.

CPAs can determine whether the IT budget makes financial sense by assessing its impact on three areas: financial key performance indicators (KPIs), financial statements and cash flow.

The reserve approach to IT budgeting helps organizations manage cash flow. The technique is similar to the system used by many homeowners’ associations. The strategy is especially useful for smaller entities and not-for-profits, which have less cash on hand for large technology expenditures.

Donny Shimamoto (donny@intraprisetechknowlogies.com) is managing director of IntrapriseTechKnowlogies in Honolulu.

To comment on this article or to suggest an idea for another article, contact Jeff Drew, senior editor, at jdrew@aicpa.org or 919-402-4056.

AICPA RESOURCES

JofA articles

- “Technology 2012 Preview: Part 1,” Nov. 2011, page 46, and “Technology 2012 Preview: Part 2,” Dec. 2011, page 30

- “Planning for Uncertainty: New Approach to Forecasting Guides Companies in Unpredictable Economy,” Oct. 2011, page 32

- “Scenario Planning: Navigating Through Today’s Uncertain World,” March 2011, page 22

JofA video

Conferences

- CFO Conference, May 17–18, New Orleans

- Practitioners Symposium and TECH+ Conference in partnership with the Association for Accounting Marketing Summit, June 11–13, Las Vegas

For more information or to register, go to cpa2biz.com or call the Institute at 888-777-7077.

Website

Quantum of Paperless (PDF download, available only to Private Companies Practice Section members)

IT Division and CITP credential

The AICPA Information Technology (IT) Division serves members of the IT Membership Section (ITMS), CPAs who hold the Certified Information Technology Professional (CITP) credential, other AICPA members, and others who want to maximize information technology to provide risk, fraud, internal control, audit, and/or information management services within their firms or for their employers. The division aims to support members and credential holders who leverage technology to provide assurance or business insight about financial-related information (direct and indirect financial data, processes or reporting) to support their clients and/or employers. To learn about the IT Division, visit aicpa.org/infotech.

More from the JofA: