- feature

- PRACTICE MANAGEMENT

A wealth of opportunity

CPAs can expand their practice by helping clients assemble and monitor financial management teams.

Please note: This item is from our archives and was published in 2012. It is provided for historical reference. The content may be out of date and links may no longer function.

Related

Differentiating agentic and generative AI — and more with a Tech Q&A author

How to ease taxes on inherited IRAs

How AI is transforming the audit — and what it means for CPAs

Much has been written in recent years about wealth management services that call for practitioners, including CPAs, to have personal financial planning certification and to come under investment-adviser or other regulations. Much less attention has been paid to PFP services that don’t require specialization or additional licensing.

One of these services is helping clients assemble and oversee wealth management teams. In addition to CPAs, these teams consist of attorneys, investment advisers, pension actuaries, insurance experts and others. CPAs also can offer important accounting and tax services to wealth management teams. For tax practitioners, the ability to provide these PFP-related services is one of many market differentiators between CPAs and registered tax return preparers (a designation recently created under IRS regulations). For other CPAs who don’t have a credential such as the AICPA’s Personal Financial Specialist (PFS), PFP-related services present an opportunity to add a profitable practice area, though additional education might be necessary.

THE VALUE PROPOSITION

While some clients know how to choose and monitor a wealth management team fitting their needs, most do not have the expertise or time to adequately vet the array of professionals needed. CPAs are well positioned to help clients pick the right advisers and, perhaps more important, to avoid the wrong ones. That’s because CPAs possess a number of attributes essential to this role:

- Strong, often multigenerational trusted client relationships.

- Related intimate knowledge of the client’s financial and, often, nonfinancial issues.

- Fiduciary responsibility to act in the client’s best interest (except in certain cases, such as independent audits).

- Professional discernment to disqualify those likely to be a poor fit for a client’s team.

- The related ability to recognize inappropriate planning approaches for a particular client.

- A strong understanding of the unique financial planning issues of business owners.

- Deep, relevant technical skills in such PFP areas as tax and estate planning, budgeting, financial analysis and managing cash flow.

- An existing network of allied professionals.

A CPA can serve as an independent adviser whom clients pay on a fee-for-service basis. This raises a vital question that every CPA firm must ask before offering an additional service: “Will clients pay for it?” In this case, astute clients have long understood that CPAs bring an analytical and objective perspective to the process of working with legal, investment, insurance and other professionals. The CPA’s knowledge, experience and well-honed professional skepticism neutralize sales presentations designed to appeal to client emotions. The CPA’s presence at these meetings also requires the agent or representative to provide solid analytical backing for any recommendations. Often, the CPA’s advice can save clients from wasting money on “financial solutions” that are inappropriate for their needs—a savings that may far exceed the cost of the CPA’s time.

For example, a business owner planning retirement may be bombarded with sales pitches for variable annuities, insurance policies and other investment vehicles. In those situations, the CPA can step in and ask the questions needed to assess the products. The CPA might ask the seller of the annuity, “How exactly does this work? What are the benefits and costs? What is your commission?” (See sidebar, “Questions CPAs Can Ask,” below.) The CPA also can evaluate the credibility of the product and of the person pushing it.

CPAs benefit from asking questions of reputable professionals in the many PFP disciplines. Knowledge gained from regular interactions with these professionals tends to bring new sophistication to a CPA firm. That, in turn, attracts a higher level of new clients.

There is little capital outlay in providing these services—other than for marketing, modifying client engagement letters and providing related legal advice—and an elaborate business plan should not be necessary. Most seasoned CPA practitioners already possess the foundational experience and expertise to start helping clients with wealth management teams, but that doesn’t mean that CPAs mulling such a move don’t have much to learn and consider.

ENHANCED SKILLS REQUIRED

Before CPAs can assist in developing a wealth management team, they need to understand the following:

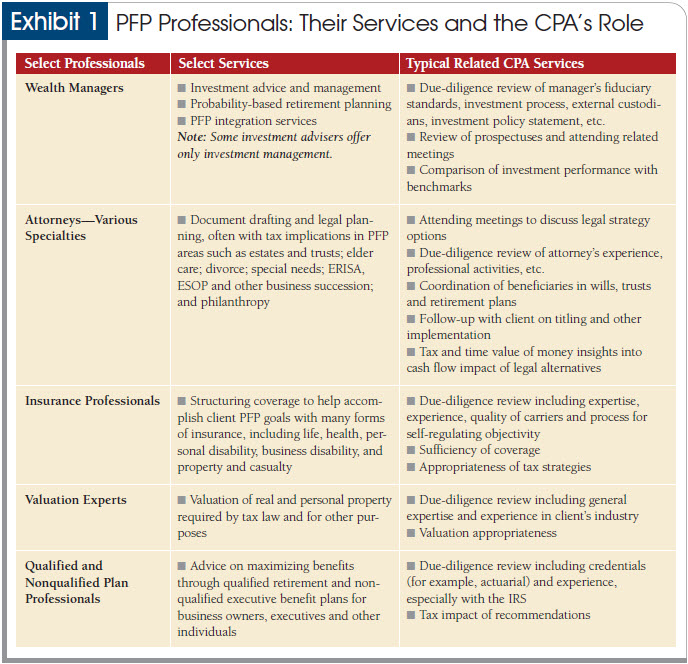

The roles played by wealth management team members. Key to putting together the right team is gaining a general understanding of what each PFP professional does and the kinds of problems that each can solve. Exhibit 1 lists these professionals and the services they provide and also lists related services that CPAs can offer. CPAs can charge for these tasks individually or in combination.

{kind=link}

The understanding of each professional’s role and strengths is essential to knowing which questions to ask when assessing a professional’s qualifications, managing clients’ expectations about what a competent professional in each area should be able to accomplish for them, and properly leveraging the perspectives of multiple specialists. This process often leads to creative solutions to client problems that individual team members might not reach on their own.

Sources of CPE and other educational and regular reference materials. CPAs who want to help clients with wealth management teams need to possess or acquire a solid understanding of investment theory, types of insurance products, risk management and behavioral studies. For example, CPAs not licensed to provide investment recommendations don’t need to be investment experts, but they do need to know enough to help the client assess an investment adviser’s credentials or recommendations. Resources such as the AICPA’s Personal Financial Planning Section and PFS curriculum can help CPAs find CPE courses and other learning materials on these and other crucial subjects. In addition to CPE and reading about PFP topics, CPAs can gain valuable insights through networking with wealth management professionals and connecting with fellow CPAs, possibly through the AICPA’s PFP Section and state CPA societies.

The potential applicability of CPA professional standards and regulations, and how to effectively minimize liability. CPAs need to understand how to manage the liability and other risks associated with helping clients deal with wealth management professionals and issues. These risks, like other CPA practice risks, are manageable with knowledge, good judgment and common sense. CPAs should know which clients are suitable for help with wealth management teams. CPAs also need to possess or gain a relative understanding of the various regulatory and AICPA standards governing the numerous professional and practice areas involved in financial planning. This knowledge will help CPAs avoid offering services that require investment or insurance licensing or that could come under specific CPA professional standards, unless intended. For example, a CPA not intending to fall under the AICPA’s attestation standards needs to know enough about the standards so as not to accidently provide attestation advice that unknowingly would subject him or her to those standards.

In addition, CPAs should ensure that clients are making the final decisions on their finances and are aware that the responsibility for those decisions lies with them. A well-crafted engagement letter or letter modification is an important part of this process. CPAs should speak with an attorney and professional liability insurance provider before beginning any work with wealth management teams.

HOW TO CHARGE FOR SERVICES

CPAs can charge an hourly rate for attending PFP meetings and follow-up monitoring, or an annual retainer with well-defined service specifications. CPAs can earn the rates they want to charge if they learn how to communicate the value of their service to clients. That value is considerable for clients who lack the skills to properly qualify and monitor financial advisers. CPAs need to understand the theories and forces behind client behavior. For example, clients who don’t truly understand the stock market are likely to want to jump into the market when it suddenly rises and bail when it abruptly falls. The result of these emotionally driven decisions is that clients end up buying high and selling low—the opposite of what they should be doing. It is crucial for CPAs and other advisers to comprehend how clients relate to financial issues and how to continually enhance interpersonal communication with clients. In satisfaction ratings, clients often place as much or more weight on their perception of service and relationship quality as they do on the CPA’s knowledge and creative money-saving solutions.

As the investment of their time is the primary cost, CPAs can roll out wealth management team services slowly, starting with attending PFP meetings for a few clients, then adding services and new clients as the word gets out and demand expands.

CPAs also can play an important and profitable role as the tax and accounting resource to wealth management teams. On the accounting side, CPAs can provide personal financial statement, budgeting, cash flow maximization and related services. On the tax side, CPAs can participate in joint planning meetings with the other advisers to ensure that the most effective tax strategies are being used at each planning stage in relation to investment, insurance and other PFP recommendations. Before a financial plan is finalized, it is wise for CPAs to perform an overall tax strategy review to ensure that the plan is “tax-smart” throughout.

CONCLUSION

Clients are seeking the right advisers to help them navigate through the uncertainty in our economy. A CPA who remains on the PFP sidelines may be forcing many clients who lack the proper knowledge to try to find competent advisers on their own at a time when they could benefit from the CPA’s insight, experience and objectivity. For many CPAs, tangential PFP involvement has become an issue of quality client service, client relevance, profitability and competitiveness. Helping clients assemble and monitor wealth management teams is the right option for many practitioners and firms who have not sought PFP specialization but want to enhance services and remain on a traditional fee-for-service basis with clients.

Questions CPAs Can Ask

Following are typical due-diligence questions CPAs can ask investment and insurance professionals vying to become part of a client’s wealth management team.

INVESTMENT PROFESSIONALS

1. Do you practice true asset allocation of stocks and bonds, diversifying across many categories and geographical areas? If so, detail your approach.

2. What is your investment style?

3. How do you incorporate risk in portfolio selection, and do you measure risk and risk-adjusted returns of your portfolio?

4. What is your investment performance record?

5. How are client preferences and needs incorporated in the portfolios you design?

6. Describe your client service procedures.

7. Disclose any potential conflicts of interest.

8. Do you offer clients other financial services, such as retirement planning?

9. Do you use an independent custodian?

10. What is your fee structure?

INSURANCE PROFESSIONALS

1. How do you determine the face amount of insurance necessary in a given client situation?

2. What is the quality of carriers with whom you work?

3. Are you limited to working with certain companies?

4. How long have you been in the business, and what specialization credentials do you have?

5. How do you determine the best type of life insurance policy for a client?

a. Provide some examples of when you recommend different types of policies, such as term, whole, universal or variable.

b. If both term and a more expensive product could be used, can you give me examples of how you present the costs and benefits of each?

6. What is your process for self-regulating objectivity?

a. What is your process for recommending the right product, rather than the one offering the highest commission?

b. Can you give me examples of when you introduced a lower-cost product as a reasonable option when the client could have afforded a more expensive one?

7. Who are your typical clients in terms of income, net worth and profession?

8. Tell me about the types and complexity of the problems you help clients solve, in areas such as estate, retirement and business planning.

9. Can you tell me how you handle difficult insurance underwriting issues and provide examples?

10. Can you provide references from other CPAs, attorneys, bankers and clients?

EXECUTIVE SUMMARY

- CPAs who don’t want to provide investment advice can create a profitable practice area helping clients assemble wealth management teams consisting of investment advisers, insurance brokers, attorneys and other professionals.

- CPAs operating on a fee-for-service basis can offer to assist clients with performing due diligence on potential wealth team members and vetting specific investment and other proposals made to the client.

- CPAs can charge individually or in combination for a number of services, including sitting in on client meetings with advisers, assessing the tax impact of various strategies and providing the objectivity and analytical thinking to counteract product sales pitches that appeal to clients’ emotions.

- It is crucial for CPAs considering the addition of support services for wealth management teams to understand the regulatory and standards structure that governs the various specialties within personal financial planning. CPAs don’t want to accidently give advice that subjects them to regulatory scrutiny or puts them under AICPA standards for a certain specialty.

- Continuing education is essential for CPAs looking to assist with wealth management teams. CPAs need to know enough about investment theory, risk management and human behavior to properly analyze specific advice and know how to counsel clients effectively.

- CPAs must make sure that clients make all the final decisions on financial planning moves and that clients accept responsibility for those decisions. Engagement letters play a key role in protecting the CPA.

- Before advising clients about wealth management teams, CPAs should consult with their attorneys and insurance agents.

Lewis J. Altfest (laltfest@altfest.com) is CEO and chief investment officer, and Walter M. Primoff (wprimoff@altfest.com) is Professional Advisor Group director, both of Altfest Personal Wealth Management in New York City. Altfest also is an associate professor of finance at Pace University.

To comment on this article or to suggest an idea for another article, contact Jeff Drew, senior editor, at jdrew@aicpa.org or 919-402-4056.

AICPA RESOURCES

JofA articles

- “Estate Planning Action Steps,” Oct. 2011, page 24

- “Advising Financially Stressed Clients,” Sept. 2011, page 50

- “PFP Services Guidelines,” July 2011, page 22

- “A Sea Change for Gift and Estate Planning,” July 2011, page 24

Publications

- Estate Planning After the Tax Relief and Job Creation Act of 2010: Tools, Tips, and Tactics (#091056HS, CD-ROM)

- Life Insurance: How to Use It to Your Clients’ Advantage (#091070)

- The Adviser’s Guide to Multistate Income Taxation: Compliance and Planning Opportunities (#PTX1201P)

- The Adviser’s Guide to S Corporations: Tax Compliance and Planning Strategies (#091095)

- The Adviser’s Guide to S Corps, C Corps, Partnerships, LLCs and Sole Proprietorships: Making the Right Choice (#091100)

Conference

Practitioners Symposium and TECH+ Conference in partnership with the Association for Accounting Marketing Summit, June 11–13, Las Vegas

For more information or to make a purchase or register, go to cpa2biz.com or call the Institute at 888-777-7077.

Websites

- Fox Financial Planning Network for CPAs, aicpa.org/pfp/ffpn

- Personal Financial Planning Practice Center, aicpa.org/pfp/practicecenter

- Private Companies Practice Section Practice Growth & Client Service Center, tinyurl.com/6quchst

PFP Member Section and PFS credential

Membership in the Personal Financial Planning (PFP) Section provides access to specialized resources in the area of personal financial planning, including complimentary access to Forefield Advisor. Visit the PFP Center at aicpa.org/PFP. Members with a specialization in personal financial planning may be interested in applying for the Personal Financial Specialist (PFS) credential. Information about the PFS credential is also available at aicpa.org/PFS.

Private Companies Practice Section

The Private Companies Practice Section (PCPS) is a voluntary firm membership section for CPAs that provides member firms with targeted practice management tools and resources, as well as a strong, collective voice within the CPA profession. Visit the PCPS Firm Practice Center at aicpa.org/PCPS.

More from the JofA: