- feature

- REGULATION

Financial Regulatory Reform: What You Need to Know

Please note: This item is from our archives and was published in 2010. It is provided for historical reference. The content may be out of date and links may no longer function.

Related

PCAOB seeks feedback on its 5-year strategic plan

Are finance leaders moving too fast on agentic AI?

AICPA updates audit standards related to external confirmations

The Dodd-Frank Wall Street Reform and Consumer Protection Act, which became law in July, will create new regulations for companies that extend credit to consumers, exempt small public companies from Sarbanes-Oxley section 404(b), make auditors of broker-dealers subject to PCAOB regulation and change registration requirements for investment advisers. The profession successfully advocated for CPAs to be carved out of the new Consumer Financial Protection Bureau for usual and customary activities.

Some highlights of the legislation that may be of particular interest to CPAs are summarized below (see Exhibit 1 for additional details).

{kind=link}

FINANCIAL STABILITY OVERSIGHT COUNCIL

The legislation creates a new systemic risk regulator called the Financial Stability Oversight Council. The council, chaired by the Treasury secretary and whose members will be heads of regulatory agencies, including the chairmen of the Federal Reserve, FDIC and SEC among others, will identify any company, product or activity that could threaten the financial system.

The Federal Reserve will supervise the companies identified by the council, and the FDIC would carry out instructions by the council to close large entities under a new orderly liquidation authority. The council, through the Federal Reserve, will also have the power to break up large firms, require increased reserves, or veto rules created by another new regulator—the Bureau of Consumer Financial Protection—with a two-thirds vote.

BUREAU OF CONSUMER FINANCIAL PROTECTION

The Bureau of Consumer Financial Protection consolidates most federal regulation of financial services offered to consumers and replaces the Office of Thrift Supervision’s seat on the FDIC board. Almost all credit providers, including mortgage lenders, providers of payday loans, other nonbank financial companies, and banks and credit unions with assets over $10 billion will be subject to new regulations.

CPAs providing “customary and usual” accounting activities, including the provision of “accounting, tax, advisory, or other services that are subject to the regulatory authority of a [s]tate board of accountancy” are carved out from the bureau’s authority. In addition, other services “incidental” to such usual and customary accounting activities, to the extent that they are not offered or provided separate and apart from such customary and usual accounting activities or to consumers who are not receiving such customary and usual accounting activities, are also carved out. Refund anticipation loan providers are not exempt.

SOX 404(b) EXEMPTION

The act amends the Sarbanes-Oxley Act (SOX) to make permanent the exemption from its section 404(b) requirement for nonaccelerated filers (those with less than $75 million in market cap) that has temporarily been in effect by order of the SEC. The act also requires the SEC to complete a study within nine months of the act’s enactment on how to reduce the burden of 404(b) compliance for companies with market caps between $75 million and $250 million. The study will consider whether any such methods of reducing the burden, or a complete exemption, would encourage companies to list on exchanges.

PCAOB’S NEW POWERS

The act closed an ambiguity in SOX. Under SOX, auditors of broker-dealers were required to register with the board, but the board did not find SOX gave it authority to regulate auditors of privately-held broker-dealers. “The Dodd-Frank Act provides the PCAOB with standard-setting, inspection and disciplinary authority regarding broker-dealer audits,” said the PCAOB in a statement.

However, the act allows the PCAOB, in its inspection rule, to differentiate among broker-dealer classes and exempt introducing brokers such as those who do not engage in clearing, carrying or custody of client assets. The act reconciles registration with inspection so that any auditors not covered by the inspection rule would also no longer be required to register with the PCAOB.

The act also allows the PCAOB, under certain circumstances, to share information with foreign auditor oversight authorities, which should help the board gain access to foreign regulators’ inspection information as well.

The PCAOB said more information about its plans to implement this authority and guidance for auditors of brokers and dealers will be forthcoming.

ACCOUNTING STANDARDS

The act gives the Financial Stability Oversight Council the duty to monitor domestic and international financial regulatory proposals and developments, including insurance and accounting issues, and to advise Congress and make recommendations in such areas that will enhance the integrity, efficiency, competitiveness and stability of the U.S. financial markets.

In a compromise reached in response to concerns raised by the AICPA and others over more onerous language proposed in earlier stages of the legislation, the final act allows the council to “submit comments” to the SEC and any standard-setting body with respect to an existing or proposed accounting principle, standard or procedure.

The act also provides a permanent funding mechanism for GASB by authorizing the SEC to require a national securities association to levy an “accounting support fee,” the proceeds from which would be remitted to the Financial Accounting Foundation.

REGISTERED INVESTMENT ADVISERS

Currently, the Investment Advisers Act of 1940 requires investment advisers with over $30 million in assets under management to register with the SEC.

Advisers with assets under management between $25 million and $30 million may elect to register with the SEC. Under the Dodd-Frank act, this threshold will be raised to $100 million, thus shifting more than 4,000 of approximately 11,500 SEC-registered investment advisers to state securities regulatory oversight, said AICPA Senior Manager Teighlor March.

However, the act provides certain exceptions to this requirement. For example, if an adviser would have to register in 15 or more states as a result, the act provides an option to register instead with the SEC.

AIDING AND ABETTING SECURITIES FRAUD

Because it lowers the legal standard from “knowing” to “knowing or reckless,” the act may make it easier for the SEC to prosecute aiders and abettors of those who commit securities fraud under the Securities Act of 1933, the Securities Exchange Act of 1934, and the Investment Advisers Act of 1940.

The AICPA and state CPA societies successfully lobbied to exclude more onerous amendments to the bill that would have opened the door for trial attorneys to file private rights of action.

A study is required within one year of enactment regarding private rights of action for aiding and abetting claims to be performed by the Government Accountability Office. The outcome of this study could potentially broaden the ability of private plaintiffs to bring aiding and abetting claims in civil courts, which would be a setback to the CPA profession.

ADVISERS TO PRIVATE FUNDS

Significantly, the act eliminates the private adviser exemption under the Investment Advisers Act of 1940, which will consequently result in more advisers’ having to register with the SEC. Advisers to venture capital funds remain exempt from registration, as well as advisers to private funds if such an adviser acts solely as an adviser to private funds and has U.S. assets under management below $150 million. It also amends the Investment Advisers Act to specifically exclude “family offices” from registration as an investment adviser.

EXECUTIVE COMPENSATION, CORPORATE GOVERNANCE

The act requires a nonbinding shareholder vote on executive pay. Compensation based on financial statements that are restated must be returned for the three years preceding the restatement in an amount equal to the excess of what would have been paid under the restated results. Listing exchanges will enforce the compensation policies.

“Management focus on accounting accuracy may be enhanced, but in the end compensation committees may still set compensation at the board’s discretion,” said AICPA Technical Manager Sharon Strother. “Companies may need to review existing compensation contracts.”

The act also requires directors on compensation committees to be independent of the company and its management, and requires new disclosures regarding compensation.

The act requires the SEC, within 180 days after enactment, to issue rules requiring companies to disclose in the proxy statement why they have separated, or combined, the positions of chairman and CEO.

OFFICE OF THRIFT SUPERVISION

The Office of Thrift Supervision (OTS), which is currently the regulator for savings-and-loan (S&L) financial institutions, will be rolled into the Office of the Comptroller of the Currency (OCC), which also regulates federally chartered banks.

Although the act makes clear that the OTS will no longer exist after its responsibilities are transferred to the OCC, it also allows existing thrift chartered institutions to continue to operate under OCC regulation and the OCC can grant new charters for federal savings banks.

Matthew G. Lamoreaux (mlamoreaux@aicpa.org) is a JofA senior editor. The author wishes to thank the following AICPA staff who made substantial contributions to the preparation and review of this article: Diana Deem, Matthew Iandoli, Peter Kravitz, Cynthia Lund, Teighlor March, Mark Peterson and Sharon Strother.

To comment on this article or to suggest an idea for another article, contact Matthew G. Lamoreaux, senior editor, at mlamoreaux@aicpa.org or 919-402-4435.

For additional information on the Dodd-Frank Act, see the following online resources:

- The AICPA’s Financial Regulatory Reform advocacy page

- “The Dodd-Frank Wall Street Reform and Consumer Protection Act: Financial Regulatory Reform Legislation” (AICPA PFP Section web seminar)

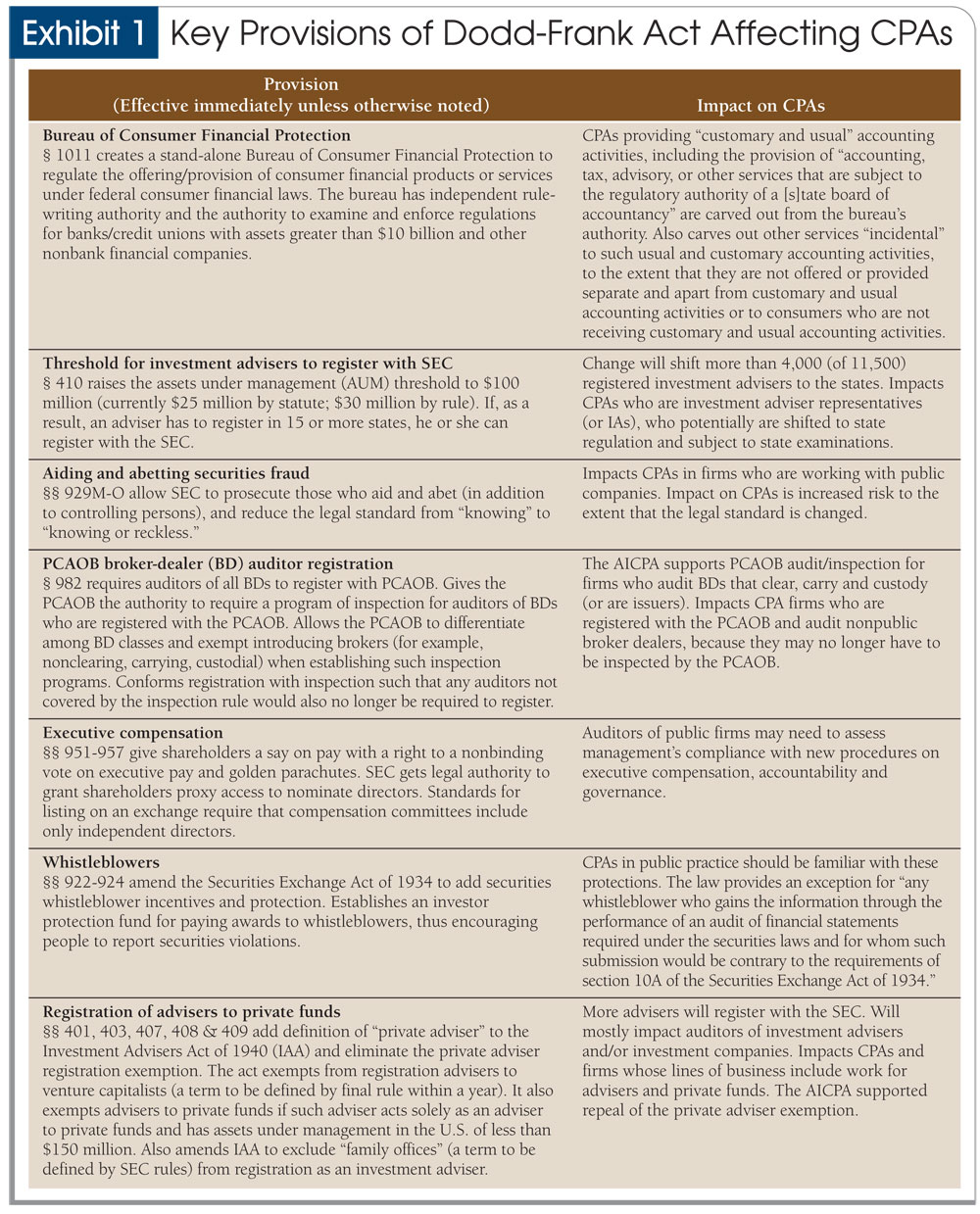

Exhibit 1: Key Provisions of Dodd-Frank Act Affecting CPAs

| Provision (Effective immediately unless otherwise noted) | Impact on CPAs |

| Bureau of Consumer Financial Protection § 1011 creates a stand-alone Bureau of Consumer Financial Protection to regulate the offering/provision of consumer financial products or services under federal consumer financial laws. The bureau has independent rule-writing authority and the authority to examine and enforce regulations for banks/credit unions with assets greater than $10 billion and other nonbank financial companies. | CPAs providing “customary and usual” accounting activities, including the provision of “accounting, tax, advisory, or other services that are subject to the regulatory authority of a [s]tate board of accountancy” are carved out from the bureau’s authority. Also carves out other services “incidental” to such usual and customary accounting activities, to the extent that they are not offered or provided separate and apart from customary and usual accounting activities or to consumers who are not receiving customary and usual accounting activities. |

| Threshold for investment advisers to register with SEC § 410 raises the assets under management (AUM) threshold to $100 million (currently $25 million by statute; $30 million by rule). If, as a result, an adviser has to register in 15 or more states, he or she can register with the SEC. | Change will shift more than 4,000 (of 11,500) registered investment advisers to the states. Impacts CPAs who are investment adviser representatives (or IAs), who potentially are shifted to state regulation and subject to state examinations. |

| Aiding and abetting securities fraud §§ 929M-O allow SEC to prosecute those who aid and abet (in addition to controlling persons), and reduce the legal standard from “knowing” to “knowing or reckless.” | Impacts CPAs in firms who are working with public companies. Impact on CPAs is increased risk to the extent that the legal standard is changed. |

| PCAOB broker-dealer (BD) auditor registration § 982 requires auditors of all BDs to register with PCAOB. Gives the PCAOB the authority to require a program of inspection for auditors of BDs who are registered with the PCAOB. Allows the PCAOB to differentiate among BD classes and exempt introducing brokers (for example, nonclearing, carrying, custodial) when establishing such inspection programs. Conforms registration with inspection such that any auditors not covered by the inspection rule would also no longer be required to register. | The AICPA supports PCAOB audit/inspection for firms who audit BDs that clear, carry and custody (or are issuers). Impacts CPA firms who are registered with the PCAOB and audit nonpublic broker dealers, because they may no longer have to be inspected by the PCAOB. |

| Executive compensation §§ 951-957 give shareholders a say on pay with a right to a nonbinding vote on executive pay and golden parachutes. SEC gets legal authority to grant shareholders proxy access to nominate directors. Standards for listing on an exchange require that compensation committees include only independent directors. | Auditors of public firms may need to assess management’s compliance with new procedures on executive compensation, accountability and governance. |

| Whistleblowers §§ 922-924 amend the Securities Exchange Act of 1934 to add securities whistleblower incentives and protection. Establishes an investor protection fund for paying awards to whistleblowers, thus encouraging people to report securities violations. | CPAs in public practice should be familiar with these protections. The law provides an exception for “any whistleblower who gains the information through the performance of an audit of financial statements required under the securities laws and for whom such submission would be contrary to the requirements of section 10A of the Securities Exchange Act of 1934.” |

| Registration of advisers to private funds §§ 401, 403, 407, 408 & 409 add definition of “private adviser” to the Investment Advisers Act of 1940 (IAA) and eliminate the private adviser registration exemption. The act exempts from registration advisers to venture capitalists (a term to be defined by final rule within a year). It also exempts advisers to private funds if such adviser acts solely as an adviser to private funds and has assets under management in the U.S. of less than $150 million. Also amends IAA to exclude “family offices” (a term to be defined by SEC rules) from registration as an investment adviser. | More advisers will register with the SEC. Will mostly impact auditors of investment advisers and/or investment companies. Impacts CPAs and firms whose lines of business include work for advisers and private funds. The AICPA supported repeal of the private adviser exemption. |

AICPA RESOURCES

Website

AICPA Advocacy Web page on Financial Regulatory Reform

Book

Financial Reporting Fraud: A Practical Guide to Detection and Internal Control, second edition (#029890)

For more information or to make a purchase, go to cpa2biz.com or call the Institute at 888-777-7077.

OTHER RESOURCES

Dodd-Frank Wall Street Reform and Consumer Protection Act

More from the JofA: