- feature

- TAX

Income Tax Accounting for Trusts and Estates

Planning allocations between entities and beneficiaries is even more critical with higher tax rates on the horizon.

Please note: This item is from our archives and was published in 2010. It is provided for historical reference. The content may be out of date and links may no longer function.

Related

IRS raises standard mileage rates for remainder of 2026

PEEC finalizes revisions to tax services independence guidance

IRS designates certain CRAT arrangements as listed transactions

Estates and nongrantor trusts must file income tax returns just as individuals do, but with some important differences. For one, their income is taxed at either the entity or beneficiary level depending on whether it is allocated to principal or allocated to distributable income, and whether it is distributed to the beneficiaries. And because their exemption amounts, tax brackets and related thresholds haven’t been indexed for inflation or modified for tax relief to the extent those for individuals have, they can be subject to higher tax rates at much lower levels of income. With the new Medicare tax on investment income on the highest tax brackets, estates and trusts pay still more taxes on incomes over $11,200, as opposed to $200,000 or $250,000 for individuals.

In this and other ways, the Patient Protection and Affordable Care and the Health Care and Education Reconciliation acts of 2010 (PL 111-148 and PL 111-152, respectively) affect trusts’ and estates’ income taxes and have introduced discrepancies that tax practitioners can review with their clients who administer trusts and estates. This article reviews some strategies for more tax-efficient allocation of income and principal by trusts and estates.

Income tax accounting for trusts and estates has received relatively little attention from tax professionals as well as lawmakers. This is not surprising because of the comparatively few taxpayers affected. In the 2008 tax year, approximately 3 million Forms 1041, U.S. Income Tax Return for Estates and Trusts, were filed, with an aggregate gross income of $188 billion. Aggregate taxable income and tax liability were $112 billion and $23 billion, respectively (IRS Statistics of Income, Fiduciary Returns–Sources of Income, Deductions, and Tax Liability). Compared with more than 142 million individual income tax returns (forms 1040, 1040A or 1040-EZ) reporting more than $8 trillion in gross income (IRS Statistics of Income, Individual Income Tax Returns, Preliminary Data, 2008), these are small numbers.

In addition, income taxation of estates and trusts does not generate much public interest—unlike the estate and gift tax, which has been subject to much debate within the professional community as well as in government and among the general public. As a consequence, practitioners and their clients may not be aware of several tax issues related to estates and trusts. However, as this article demonstrates, careful planning that takes these issues into account is no less important than for other types of returns and can reap significant tax benefits.

While trusts exist in many forms, this article principally concerns the most commonly encountered type of nongrantor trust. Other trusts that may be of interest to practitioners include those often used in conjunction with a small business, principally electing small business trusts (ESBTs) and qualified subchapter S trusts (QSSTs). An ESBT, defined at IRC § 1361(e)(1) with tax rules at section 641(c), holds the stock of an S corporation, with the shareholders as beneficiaries. A QSST, described in section 1361(d), likewise can hold the stock of an S corporation, with the beneficiary treated as its owner and the trust treated as a grantor trust. For more information on these trusts, see “Creative Ways of Achieving Grantor Trust Status,” The Tax Adviser, Sept. 2009, page 593.

FIDUCIARY ACCOUNTING AND INCOME TAXES

Income of estates and nongrantor trusts is taxed at either the entity or the beneficiary level, depending on the answer to the following two questions:

- Is each income, loss or deduction item part of the trust’s or estate’s distributable income, or is it part of a change in the principal?

- Is the income, loss or deduction item distributed to the beneficiaries, or does the entity retain it?

Fiduciary accounting has been characterized as somewhat similar to governmental accounting because it deals with a fund (the trust principal) and income derived from the fund.

CASE STUDY: THE JSA TRUST

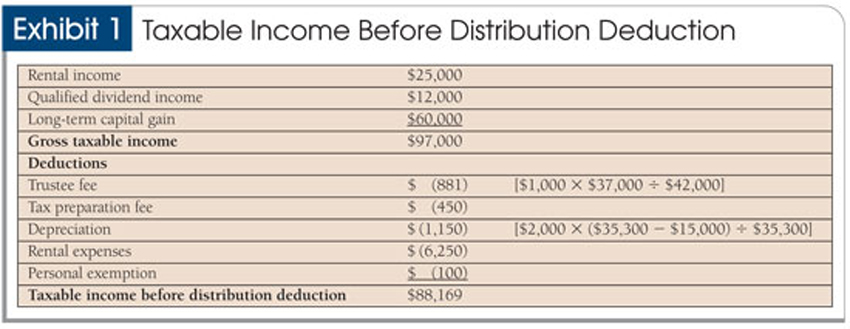

The hypothetical Jon and Susan Anders Family Trust (“JSA Trust”) reports the following income for 2010: rental income of $25,000; qualified dividend income of $12,000; municipal bond interest income of $5,000 (tax-exempt); and long-term capital gains of $60,000. Expenses are a trustee fee of $1,000; depreciation deductions of $2,000; tax return preparation fees of $450; and rental expenses of $6,250. Rental income, dividends and interest are considered trust income and will be included in accounting income (generally, all income as determined under the terms of the governing instrument and state law—IRC § 643(b)). Long-term capital gains, on the other hand, are part of the trust principal and are not included in accounting income. Thus, gross accounting income is $42,000 ($25,000 +$12,000 +$5,000).

The categorization of trustee fee and depreciation expenses depends on specifications in the trust instrument and state law. If the trust instrument is silent, state law prevails. If both are charged to the principal, net accounting income in our example is $35,300 ($42,000 +$450 +$6,250). Tax-exempt income is included in accounting income for purposes of allocating the trustee fee and depreciation deductions in determining taxable income but is excluded from taxable income.

The estate’s or trust’s taxable income is computed using the following formula:

| Gross income | |

| Less | Deductible trust expenses |

| Less | Personal exemption amount |

| Equals | Taxable income before distribution deduction |

| Less | Distribution deduction |

| Equals | Taxable income |

| Times | Applicable tax rates |

| Equals | Tax liability |

Deductible trust expenses include all expenses allocable to taxable trust income. The personal exemption amount has never been updated for inflation and is therefore very low—$600 for estates, $300 for trusts that distribute all income, and $100 for trusts that distribute part or none of the income (IRC § 642(b)). Under section 265, part of the trustee fee must be allocated to tax-exempt income as a proportion of gross accounting income. On the other hand, the $450 tax preparation fee in this example is fully deductible, under the rationale that tax preparation fees arise only if there is taxable income and the tax-exempt income does not generate this particular expense.

According to sections 167(d), 611(b)(3) and 642(e), depreciation and depletion deductions must be allocated between the trust and its beneficiaries based on the proportion of net accounting income minus distributions to net accounting income. If the trustee is required by the trust instrument or state law to allocate depreciation to the trust, the entire deduction (to the extent there is trust income) belongs to the trust. Note that in the case of an estate, the depreciation deduction is apportioned between the estate and beneficiaries regardless of the terms of the will.

Using the numbers from the hypothetical JSA Trust and assuming that the trust distributes $10,000 and $5,000, respectively, to hypothetical beneficiaries Philip and Benedict (total distributions = $15,000), taxable income before the distribution deduction is calculated as shown in Exhibit 1.

{kind=link}

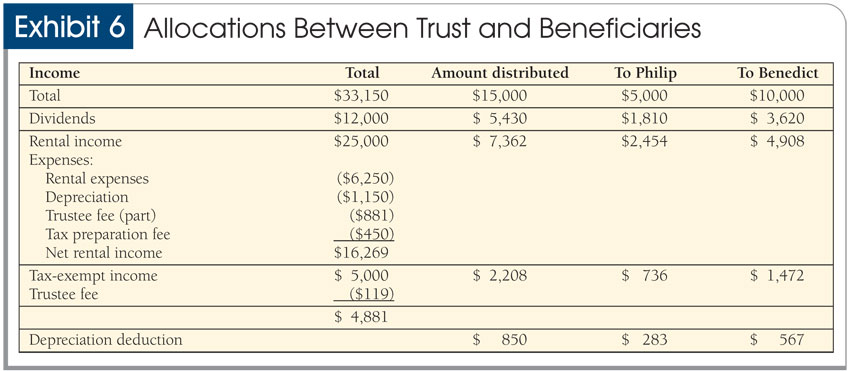

Since 12% of the gross accounting income is tax-exempt (the $5,000 municipal bond interest divided by the $42,000 gross accounting income), only 88% of the $1,000 trustee fee is deductible. The allocation of the depreciation deduction between the beneficiaries and the trust depends on net accounting income. In this case, $15,000 of $35,300 (about 42.5%) of the income is distributed. Thus, about $850 of the depreciation deduction is deductible to the beneficiaries (see Exhibit 6), and $1,150 is deductible at the trust level. Note that, if the trustee fee were deducted from trust income instead of from the trust principal, 43.7%, or $875, of the depreciation expense would be allocated to the beneficiaries and $1,125 to the trust.

{kind=link}

Practice point. Trusts will reach the top marginal tax rate faster than individuals because of the depressed progressive tax schedule (in 2010, the top marginal tax rate for trusts starts at $11,200). Thus, if possible, it is beneficial to allocate as much depreciation as possible to the trust. This can be done by specifying the allocation in the trust instrument.

Distribution deduction. To prevent double taxation on their income, estates and trusts are allowed to deduct the lesser of distributable net income (DNI) or the sum of the trust income required to be distributed and other amounts “properly paid or credited or required to be distributed” to the beneficiaries (IRC § 661(a)). This includes distributions that can be made out of either income or trust principal to the extent they are made from trust income. DNI is calculated based on accounting income less any tax-exempt income net of allocable expenses. Section 661(b) stipulates that the deduction amount consists of each class of item included in DNI (as a proportion of DNI) unless the trust instrument or state law explicitly prescribes a different allocation. Thus, the actual distribution must also be reduced by the proportionate share of net tax-exempt income. The accounting method and period of the estate or trust determine when the deduction may be claimed; the beneficiary’s tax year is not relevant.

DNI and deductible amount. In the case of the JSA Trust, DNI is computed as shown in Exhibit 2.

Note that the $119 of the trustee fee allocated to tax-exempt income is not deductible at the trust or beneficiary level; the $881 deductible part of the trustee fee is allocated between the trust and the beneficiaries as explained below. Because the amount to be distributed ($15,000) is less than DNI, it is used to determine taxable income. First, however, it must be reduced by the proportionate net tax-exempt income of $2,209 (see Exhibit 3).

Instead of a strict pro rata allocation, a trust instrument may stipulate a certain order in which income items are distributed to the beneficiaries. Similarly, state law may indicate in what order income should be distributed.

If the trust instrument of the JSA Trust or state law indicates that taxable income must be distributed before tax-exempt income, the distribution would consist of $15,000 in taxable income, and the entire $4,881 net tax-exempt income would be allocated to the trust. The distribution deduction would be $15,000. On the other hand, if tax-exempt income is distributed first, the distribution would consist of $4,881 net tax-exempt income and $10,119 taxable income. The trust’s income would be $73,169 ($88,169 – $15,000) in the former example or $78,050 ($88,169 – $10,119) in the latter case.

Practice point. Because the tax rates of estates and trusts are likely higher than the tax rates of the individual beneficiaries, it is advisable (if possible) to retain the tax-exempt income and distribute taxable income only.

Taxable income and tax liability. The tax calculation for estates and trusts with regard to long-term capital gains rates is the same as for individuals. Thus, just as for individuals, long-term capital gains and qualified dividends are currently taxed at 15% and, for trusts and estates in the 15% tax bracket (the lowest), zero. For trusts and estates, however, that bracket is available only if ordinary income is not more than $2,300.

Calculating ordinary income. Using the numbers from the JSA Trust (Exhibit 3), total taxable trust income is $75,378. Of this amount, $60,000 is long-term capital gain. The remainder is partially qualified dividend income and partially rental income. Since $15,000 of the $33,150 DNI is distributed to the beneficiaries, the proportion of the remainder retained by the trust to DNI determines the portion of qualified dividend income eligible for the preferential tax rates as shown in Exhibit 4.

Thus, ordinary income is $8,808, as shown in Exhibit 5.

Because $8,808 exceeds $2,300, the zero tax rate is not available. The tax on the capital gains and dividends is $9,986 (15% x ($60,000 + $6,570)). The tax on ordinary income is $2,106 ([33% x ($8,808 – $8,200)] + $1,905.50) for a total tax of $12,092 (see tax tables at bottom of page). If the trust were required by its governing instrument to distribute all its income currently, the trust’s taxable income would be $59,700 ($60,000 capital gains less exemption amount of $300). None of the income would be considered ordinary, and the zero rate would be available for the first $2,300 of the capital gains. Tax would be 15% x $57,400 = $8,610.

The low tax rates for long-term capital gains and qualified dividends are scheduled to sunset by the end of 2010. If no new law is enacted, capital gains will be taxed at 20% and dividends at the applicable marginal tax rate (the top two brackets of which are also scheduled to increase back to their pre–Economic Growth and Tax Relief Reconciliation Act levels of 36% and 39.6%, respectively).

Practice point. It may be advisable to recognize income in 2010 before the higher rates go into effect. Also, if the higher rates take effect, the difference between trust tax brackets and individual tax brackets becomes even more important. “Pushing” the income to the beneficiaries by distributing all or most of DNI makes even more sense, since income at the beneficiary level is more likely to be taxed at a lower rate.

DIFFERENT INCOME TYPES AT THE BENEFICIARY LEVEL

The character of the trust income at the beneficiary level is determined based on the actual distribution amount and DNI unless the trust instrument or state law specifies otherwise. Direct expenses must be allocated to the respective incomes (for example, rental expenses must be deducted from rental income). Indirect expenses, such as trustee fees, must be allocated between taxable and tax-free income. However, the tax law does not specify how indirect expenses must be attributed to different taxable income items, which allows for some flexibility.

Beneficiary allocations. The beneficiaries of the JSA Trust receive $5,000 and $10,000, respectively. Unless specified differently in the trust instrument or by state law, the two amounts are composed as shown in Exhibit 6.

Note that because dividends are taxed at a lower rate, all expenses that are not allocated to the municipal bond interest are allocated to rental income. Further note that the income items are in proportion of DNI, while the depreciation deduction is allocated between the trust and the beneficiaries based on net accounting income.

Practice point. When (or if) the lower tax rate for qualified dividends sunsets, the allocation of expenses to nondividends is no longer necessary. However, depending on the beneficiary’s individual tax situation, it may still be important to allocate the indirect expenses to one particular income item.

NEW LAWS AFFECTING ESTATES AND TRUSTS

The recently enacted health care legislation affects not only individuals and businesses but also the income of trusts and estates. Under the new IRC § 1411, trusts and estates will be subject in 2013 and subsequent tax years to a 3.8% “unearned income Medicare contribution” tax on the lower of their undistributed net investment income or the amount by which their adjusted gross income (AGI) exceeds the amount where the highest tax bracket begins. This is a much lower threshold ($11,200 in 2010) than for individuals, who are subject to this tax only if their modified AGI exceeds $250,000 for married taxpayers filing jointly and surviving spouses and $200,000 for all others.

If the JSA Trust has the same income and makes the same distribution in 2013, it would be subject to the unearned income Medicare contribution tax on $64,178 ($75,378 less $11,200 (or top income tax bracket threshold in 2013 if different)); AGI is $75,378; investment income net of expenses and deductions is also $75,378. Additional tax would be $2,439.

Practice point. Since the threshold for individuals is much higher than for estates and trusts (and since most, if not all, trust income will be considered investment income), taxpayers may want to distribute more (or all) of the trust income to limit the amount subject to the 3.8% extra tax.

Note that certain trusts will not be subject to this additional tax. For example, section 1411(e) states that the unearned income Medicare contribution tax does not apply to trusts in which the only unexpired interests are for charitable purposes. Trusts that are tax-exempt under section 501 and charitable remainder trusts (as defined in section 664) are also excluded (Joint Committee on Taxation Report).

Furthermore, simple trusts and grantor trusts are also likely to be exempt. A simple trust must distribute all current income; thus all income taxes apply at the beneficiary level, and it does not have any undistributed net investment income. A grantor trust is not considered a taxable entity because the grantor (or possibly some other person such as the beneficiary) is presumed to be the owner of the trust. The trust income is therefore taxed at the grantor level.

2010 Tax Rates for Trusts and Estates

| If taxable income is: | The tax is: |

| Not over $2,300 | 15% of taxable income |

| Over $2,300 but not over $5,350 | $345.00 plus 25% of the amount over $2,300 |

| Over $5,350 but not over $8,200 | $1,107.50 plus 28% of the amount over $5,350 |

| Over $8,200 but not over $11,200 | $1,905.50 plus 33% of the amount over $8,200 |

| Over $11,200 | $2,895.50 plus 35% of the amount over $11,200 |

EXECUTIVE SUMMARY

Income taxation of estates and trusts may not receive the same attention as individual income taxes or estate taxes. This article describes some of the general income tax rules of these entities, such as the different rules for allocation of income and deduction items between principal and distributable income, between tax- exempt and taxable income, and between trusts/estates and beneficiaries.

These allocations are prescribed either by the trust instrument, state law or the Internal Revenue Code. In some cases, taxpayers have flexibility. Generally, it is advisable to “push” the taxable income and the income taxed at higher rates to the beneficiary, because the tax rate schedule for trusts and estates is depressed, with the highest bracket currently starting at $11,200.

Pushing income to beneficiaries may become still more important if lower tax rates under the Economic Growth and Tax Relief Reconciliation Act are allowed to sunset as scheduled at the end of 2010.

Also, since income from estates and trusts is mostly investment income, the new 3.8% unearned income Medicare contribution tax will apply to most, if not all, of the trust’s income falling in the highest tax bracket. Individuals are not subject to this tax until their modified AGI reaches $250,000 (married filing jointly and surviving spouses) or $200,000. Thus, distributing trust income to beneficiaries can lower the amount subject to this extra tax.

Sonja Pippin (sonjap@unr.edu) is an assistant professor in the Department of Accounting and Information Systems at the University of Nevada–Reno.

To comment on this article or to suggest an idea for another article, contact Paul Bonner, senior editor, at pbonner@aicpa.org or 919-402-4434.

AICPA RESOURCES

Publications on demand

- Can You Trust Your Trust: What the Practitioner Needs to Know (#017271PDF)

- The Adviser’s Guide to the Revised Trust Accounting Rules (#061073PDF)

- Fiduciary/Trust Accounting: A Comprehensive Practice Guide (#091029PDF)

CPE self-study

Form 1041: Income Taxation of Estates and Trusts (#736946SNF)

For more information or to make a purchase, go to cpa2biz.com or call the Institute at 888-777-7077.

The Tax Adviser and Tax Section

The Tax Adviser is available at a reduced subscription price to members of the Tax Section, which provides tools, technologies and peer interaction to CPAs with tax practices. More than 23,000 CPAs are Tax Section members. The Section keeps members up to date on tax legislative and regulatory developments. Visit the Tax Center at aicpa.org/tax. The current issue of The Tax Adviser is available at aicpa.org/pubs/taxadv.

PFP Member Section and PFS credential

Membership in the Personal Financial Planning (PFP) Section provides access to specialized resources in the area of personal financial planning, including complimentary access to Forefield Advisor. Visit the PFP Center at aicpa.org/PFP. Members with a specialization in personal financial planning may be interested in applying for the Personal Financial Specialist (PFS) credential. Information about the PFS credential is available at aicpa.org/PFS.

More from the JofA: