| EXECUTIVE SUMMARY | |

EACH VALUATION ASSIGNMENT IS UNIQUE, and often there’s more than one way to answer a question, interpret a fact or approach a problem. How the valuator prepares the client for the BV engagement sets its direction and becomes the foundation of the engagement letter and, ultimately, a responsible and accurate final product.

THE ENGAGEMENT LETTER ENSURES both client and practitioner understand the assignment and can help a CPA/valuator clarify the ownership interest to value, the appropriate professional standards to follow and the fees and payment terms.

THE VALUE OF A COMPANY for gift-tax purposes likely will differ from its value for a sale to a specific purchaser, and an entity’s value for sale on a going-concern basis will differ from its liquidation value—which similarly differs if the valuation is for an orderly liquidation as opposed to a forced one.

THE VALUATOR’S DECISIONS about BV methodology, discounts and premiums and other formulas depend on knowing whether what’s being valued is an entire entity vs. a 49% interest in a limited liability company, for example.

FINDINGS ARE REPORTED IN DIFFERENT WAYS: formal (traditional) written reports, informal (summary) reports, no written report at all or a hybrid of the three. The amount of time to produce each of these varies substantially, so know what the client wants and budget time accordingly.

BV FINDINGS ARE NOT TRANSFERABLE to serve multiple purposes. An engagement letter should specify that a valuation opinion is valid as of a particular date for a particular purpose—and no other. | | TIMOTHY W. YORK, CPA/ABV, is a principal of Dixon Odom PLLC in Birmingham, Alabama; he serves in the valuation services group of the firm. He speaks and writes on valuation issues and serves on AICPA business valuation committees. He also is a member of several valuation organizations. His e-mail address is tyork@dixonodom.com . |

ime is money and the marketplace can be unforgiving of mistakes in today’s professional services environment, so listen well when someone asks you to perform a business valuation (BV). Clients’ reasons for needing valuations vary greatly and may include an emotional component (as in death, divorce, litigation or retirement, for example) that makes them especially anxious about the process. In contrast to compliance-based CPA services, which lend themselves to schedules, checklists and clear-cut decisions, many aspects of BV rely on interpretative rather than definitive answers. Valuators must take care to begin each assignment with a crystal-clear understanding of its context and purpose. This article offers instruction on how to frame a business valuation to minimize the possibility of missteps. GET ON THE GOOD FOOT

CPAs have been developing BV as a practice area for about a decade, and certification, competence and due care are important aspects of their technical proficiency. The fifth article of the “Principles of Professional Conduct” in AICPA Professional Standards (ET section 56), says, “A member should observe the profession’s technical and ethical standards, strive continually to improve competence and the quality of services, and discharge professional responsibility to the best of the member’s ability.” In the case of business valuation services, the Statement on Standards for Consulting Services and ET section 102, “Integrity and Objectivity,” not only requires member integrity and objectivity but warns against conflicts of interest and subordination of judgment to others. Not meeting those standards can be construed as negligence. However, CPA valuators who obtain solid credentials in this practice area (an ABV, for example) know that methodologies, procedures and even valuation standards are not absolute. Each situation has unique aspects, and often there’s more than one way to answer a question, interpret a fact or approach a problem—it is up to an informed valuation professional to make the call. How the valuator prepares for the engagement sets its direction and becomes the foundation of a responsible and accurate final product. The sequence involves gathering information for the project, preparing the engagement letter, performing the valuation and reporting the results.

| Your BV Report Will Be Stronger If You… - Clarify the definition of value for the assignment.

- Choose the most appropriate appraisal method.

- Locate the relevant market data (it’s there).

- Select good guideline companies.

- Make sure the financial analysis is complete, with clearly explained adjustments.

- Support your discount and capitalization rates and premium calculations.

- Avoid typographical errors.

- Are logical and consistent.

Source: Understanding Business Valuation , Gary Trugman, AICPA. | | DEFINE THE ENGAGEMENT

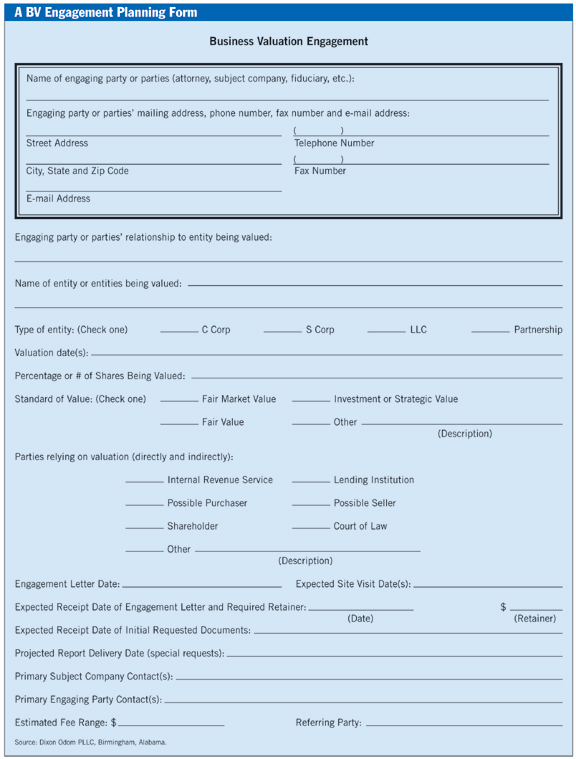

Prior to accepting a BV assignment, you must understand your subject and your purpose. As soon as the person hiring you (who may be the owner of the business to be valued, an acquiring business, an attorney or a bank representative, for example) broaches the subject, you should begin the process of gathering data for preparing an engagement letter. Finding out the relevant facts of the assignment is something valuators refer to as “defining the engagement.” It’s more complex than it sounds, and the crux of doing it well is to assume nothing and spell out as much as possible. Robin E. Taylor, CPA/ABV, a Dixon Odom LLC principal and president of the Financial Consulting Group national BV alliance, says its members often use its Web site to refine ideas about “defining the assignment before the actual work begins.” Obtain as many relevant facts as you can about the entity and the circumstances the valuation is intended to satisfy (whether it’s for a liquidation, M&A, divorce or tax purposes, for instance) and note them. To ensure you and the client agree about what services you will perform, send the client an engagement planning form and ask him or her to complete and return it (see exhibit ). This form covers basic contact information: who actually is engaging you (such as the client or the user of the report), the purpose for the valuation, timing, fees, the subject to be valued and other relevant items. The valuator will incorporate these data into the engagement letter and review and note the assumptions and conditions likely to apply. You will include all of this in your letter and, later, in the valuation report. To avoid problems such as conflict of interest, “it is extremely important to identify your client,” says Linda B. Trugman, CPA/ABV of RCH Trugman Valuation Associates. “For example, in a divorce situation, if the valuator is hired by the wife or the wife’s attorney, the wife is the client even if the husband is the business owner. It will be necessary to discuss the business operations with the husband, but it is unacceptable to discuss the case with him or his attorney.” The CPA valuator always should remember who the client is in all interactions. BUILD A BETTER LETTER

A written engagement letter clarifies the assignment for both client and valuator. It can help you to

Value the correct entity or ownership interest.

Apply the best approaches and methods.

Follow appropriate professional standards.

Apply the correct standard of value for that job.

Ensure the appropriate effective valuation date.

Use productive time efficiently.

Get paid timely—and in full.

Avoid risk to the firm and a challenge to the findings.

Maintain client confidence. Consult the AICPA, state CPA societies and colleagues for a suitable model if you’re in doubt about the language. Gary Trugman’s Understanding Business Valuation (an AICPA publication) covers this topic well. Another good resource is the CPA’s Guide to Effective Engagement Letters, Aspen Publishers, www.aspenpublishers.com . To express a clear understanding on all critical issues, make sure your letter does the following:

Identifies the subject and the purpose of the valuation . Be specific about what you are being asked to value. It could be an entire entity, asset or something less, such as a 49% interest in a limited liability company. Crucial decisions about the appropriate valuation methodology, discounts and premiums and other formulas ultimately used depend on an exact understanding. For example, instead of saying, “We will estimate the value of XYZ Inc.,” say, “We will estimate the fair market value of a 1% limited partner interest in XYZ Inc. as of December 31, 2003.” |

Identifies the standard and premise of value. There are many reasons for valuing an entity, and those circumstances can lead to different outcomes. To clarify, “premise” deals with whether the business is a going concern (most are) or one slated for liquidation, while “standard” relates to why the business is being valued. For instance, a business’s value for sale on a going-concern basis will differ from its value for liquidation purposes. It similarly makes a difference if the valuation is for an orderly liquidation as opposed to a forced one. For example, the value of a company for estate-tax purposes (fair market value) likely will differ from its value for a sale to a specific purchaser (investment or strategic value). In some instances involving litigation, the courts or the law may dictate which standard of value to use. Many valuators say the parties who hire them don’t always understand the nuances of standards of value and the consequences of the choice to an assignment. You can significantly benefit clients by teaching them about standards of value and helping them choose the most appropriate standard for the engagement. Nancy Fannon, CPA/ABV and principal in valuation consulting at Portland, Maine-based Baker Newman & Noyes LLC, says: “Many clients say to the appraiser, ‘I want to know the value of my business,’ without realizing that it can mean many different things depending on the context. Often, appraisers hear this and launch into a fair-market-value analysis. However, if a client is selling a business, what she really may want to know is what the highest multiples being paid in the marketplace are at that time. Another client who is a buyer may want to know what amount she can afford to pay based on whether the entity’s cash flow will support her ability to fund a portion of the purchase price. A fair-market-value approach may not be very helpful to either of these clients.” | | Business Valuation Resources Web sites

For a variety of BV resources, check out www.bvresources.com and www.gofcg.org . Organizations

AICPA

1211 Avenue of the Americas

New York, New York 10036-8775

Jfeldman@aicpa.org ; www.aicpa.org

American Society of Appraisers (ASA)

555 Herndon Parkway, Suite 125

Herndon, Virginia 20170

www.appraisers.org

Appraisal Foundation

1029 Vermont Avenue, NW, Suite 900

Washington, D.C. 20005

www.appraisalfoundation.org

Institute of Business Appraisers (IBA)

P.O. Box 17410

Plantation, Florida 33318

www.instbusapp.org

National Association of Certified Valuation Analysts (NACVA)

1111 E. Brickyard Road, Suite 200

Salt Lake City, Utah 84105

www.nacva.com | |

Informs the client which professional standards apply. Adhere to the professional ethics and conduct guidelines that apply to all CPA engagements and include appropriate information about performance standards in your engagement letter. Many appraisers belong to multiple valuation-related organizations, each having different development and reporting standards. Reconciling them can be complicated and time-consuming. Where a question or conflict arises, check the societies’ literature or help desks (if applicable). Make sure the work follows the model that most stringently protects and serves the client and the public good. Include a specimen “statement of assumptions and limiting conditions” as an attachment to your engagement letter. Here are three examples of such statements:

We have no present or contemplated financial interest in the company referred to in this report. Our fees for this valuation are based on our normal hourly billing rates and are in no way contingent upon the results of our findings. We have no responsibility or obligation to update this report for events or circumstances occurring subsequent to the date of this report.

Our report is based on historical and prospective financial information provided to us by management and other third parties. Had we audited or reviewed the underlying individual company data, matters might have come to our attention which would have resulted in our using amounts that differ from those provided. Accordingly, we take no responsibility for the underlying data presented or relied upon in this report. All of the representations and information supplied by management and agents are assumed to be true, accurate and complete.

The indication of value included in this report assumes the company will maintain its character and integrity through any reorganization or reduction of existing owners’/managers’ participation in the existing activities of the company.

Identifies what the client expects in reporting. Valuators report their findings in different ways: formal (traditional) written reports, informal (summary) reports, no written report at all or a hybrid of the three. The amount of time to produce each varies substantially, so determine the client’s reporting expectations at the beginning of the engagement. Report writing can consume 50% of the total time budgeted for the assignment. Occasionally the purpose of the valuation dictates what type of report is required.

Covers fee issues and billing arrangements. Valuators and clients should have a clear, mutual understanding of fee amounts and payment timing. “Valuation services are premium services that require professionals to have the best qualifications, experience and education. As such, BV commands premium fees. Billings should be addressed at the beginning of the assignment, and the valuator should obtain a commitment from the client,” says Mel H. Abraham, CPA/ABV, of Wood Ranch, California. | Ask for and get a retainer of at least 40% of the expected total fee, applicable to the final invoice. It shows the commitment level of the hiring party and gives an indication of the party’s ability to pay. This helps to avert situations (such as in a divorce or other legal proceedings) where a client subsequently may not be motivated to pay. Link subsequent payments to stages of completion—for example, on completion of the report and at agreed-on interim stages, depending on the complexity of the engagement. Here’s an example of how and how not to express a fee understanding: Don’t say: We will issue billings on a monthly basis and may increase our estimate of the $10,000 fee if unusual circumstances arise. Say something like: We will issue billings as often as weekly and will notify you immediately of issues that will cause our fee to change. We reserve the right to change the original fee estimate as the project progresses and we are able to predict more accurately the total time the project will incur. We request a retainer of 50% of the original estimate ($5,000 based on the original estimate of $10,000), which is due upon the execution and return of this engagement letter. We will apply this retainer to the final invoice, and all invoices must be paid within five working days, or we reserve the right to cease our work on the matter.

PUT PROTECTIONS IN YOUR REPORT

The valuation report, regardless of the type, should | | | PRACTICAL TIPS TO REMEMBER | Keep the following in mind:

Prior to accepting an engagement, know what the valuation will be used for and review the likely assumptions and conditions that apply to it.

To ensure you and the client agree about what services you will perform, send the client an engagement planning form and get him or her to complete and return it.

Obtain as many relevant facts as you can about the entity and the circumstances the valuation is intended to satisfy (whether it’s for a liquidation, M&A, divorce or tax purposes, for instance).

Specify the client’s reporting expectations at the beginning of the engagement.

Teach clients about standards of value and help them choose the most appropriate one. Values for similar entities or assets may differ significantly for entirely appropriate reasons.

A valuation report should include a “statement of assumptions and limiting conditions” to inform the client and the user of the report of what was done as well as what was not done in the engagement. | |

Include the “statement of assumptions and limiting conditions.” The length of such statements varies, but most professional reports have them. Prior to taking the assignment, you will have reviewed the likely assumptions and conditions that apply with the client and attached a specimen statement to the engagement letter. Reiterate them in the report to inform the client and the user of the report of what was done and not done in the engagement.

Identify your client. When you gathered data for the assignment, you learned from the hiring party (an attorney, a subject company or a fiduciary, for example) who would be using the BV report (for instance, the IRS, a possible purchaser or seller, a court of law or a lending institution). Reiterate here the identity of the client and the subject company being valued. Furthermore, describe the final users of the report. In many instances, attorneys prefer to be the conduit for their clients to keep privilege protections in force. (This is not always applicable, but the matter should be addressed in preliminary discussions.)

Limit distribution of the report. The report or findings typically are useful for only limited purposes. Circumstances vary, and values for similar entities or assets may differ significantly for entirely appropriate reasons. Make it absolutely clear the reports or findings are not transferable to serve multiple purposes. The engagement letter will have specified that your valuation opinion is valid as of a particular date for a particular purpose—and no other. Restate this in your report. The CPA/valuator can avoid costly mistakes by adhering to a few relatively simple procedures. Sound planning and preparation can make a valuation engagement proceed smoothly and enhance your success in the BV field. Resources

For information about AICPA courses, practice aids and publications, go to www.cpa2biz.com . For information about the ABV credential, go to the following AICPA Web page: http://www.aicpa.org/members/div/mcs/abv.htm . | National Conferences on Fraud and Advanced Litigation Services

October 2–3, 2003

Fontainebleau Hilton Resort

Miami Beach, Florida | National Business Valuation Conference

November 16–18, 2003

Marriott Desert Ridge Resort & Spa

Phoenix | Succession Planning Conference

December 8–9, 2003

The Royal Pacific Resort

Orlando, Florida | |

{kind=link}